In This Article

Working with outdated maps

Many of our readers know that after spending most of our lives in New Jersey, my wife and I eventually moved down to Raleigh, North Carolina in 2012. What many don’t know is how we actually got here.

A lifelong friend of mine, more like a brother than a friend, spent much of his adult life traveling alongside the foreign state department. Years ago, we asked both he and his wife a simple question:

“If you could live anywhere in the world, where would it be?”

Without hesitation, in complete unison, they answered: “Fuquay-Varina… Holly Springs, North Carolina.”

Needless to say, we were surprised.

In 2009, as I was preparing to leave the institutional side of the financial industry and move back into private wealth management, my wife and I decided to take a trip down to Raleigh to look at homes.

After countless nights scrolling Realtor.com, I assembled a list of more than 40 properties I was convinced she’d love.

There was just one problem … we could barely find any of them.

For four straight days, we drove around in circles staring at a Garmin GPS that seemed completely unaware half the neighborhoods even existed. Developments were too new. Roads weren’t updated. Entire communities simply weren’t on the map yet.

By the end of the trip, my wife hated the area.

When we came back in 2012, we worked with a local realtor instead of relying on outdated technology. Within four days we found a neighborhood we loved, built our house, moved to North Carolina … and never looked back.

Today, when people ask my wife if she likes living here, her answer is almost always the same:

“I love it. I just wish we had done it sooner.”

What changed? Simple … the maps changed.

Back in 2009, most of us still relied on standalone GPS systems like Garmin. Updates came every few months through CDs you manually installed … assuming you even bought them in the first place. Meanwhile, Raleigh was growing faster than the system could adapt.

Today, our maps update in real time as conditions change around us.

Ironically, markets have undergone a very similar transformation … yet many investors and financial “experts” still navigate modern markets with the equivalent of a 2009 Garmin.

For years now, we’ve argued that markets have fundamentally changed. Passive flows, ETFs, volatility targeting, gamma exposure, and machine-driven trading increasingly dominate price action. Yet every time markets rally, the old guard screams the same warnings:

“Valuations!”

“Bubble!”

“1999 all over again!”

Now, to be clear, valuations still matter … eventually.

But valuation alone has become an increasingly poor timing mechanism in markets driven by flows, liquidity, and rate-of-change dynamics.

Humbly, I understand the old framework better than most … because I used to live inside it … I also fought ‘change’ for far too long.

Today’s markets are no longer reacting solely to static valuation models or textbook fundamentals. Increasingly, they respond to momentum, liquidity, positioning, and shifting rate-of-change beneath the surface.

Or said differently … the maps are updating exponentially faster than market ‘experts’ understand. And that brings us to today’s note.

Because while much of Wall Street remains obsessed with valuations, bubbles, and imminent collapse … the market itself has been trading a very different message altogether.

What Markets Actually Traded

While financial television, social media, and Wall Street strategists remain focused on recession fears, tariffs, valuations, bubbles, and “imminent doom” … markets themselves have traded something entirely different.

They’ve been trading reflation.

Back in March, the dominant narrative centered around economic deterioration. Growth was slowing, inflation had re-accelerated meaningfully, and many investors became convinced the economy was rolling toward Stagflation.

But then the signals started changing.

As we discussed in “The Move Everyone Misread,” growth quietly began reaccelerating faster than consensus expected, with favorable base effects creating a firmer near-term growth backdrop than many anticipated.

By late April and early May, the setup had shifted materially.

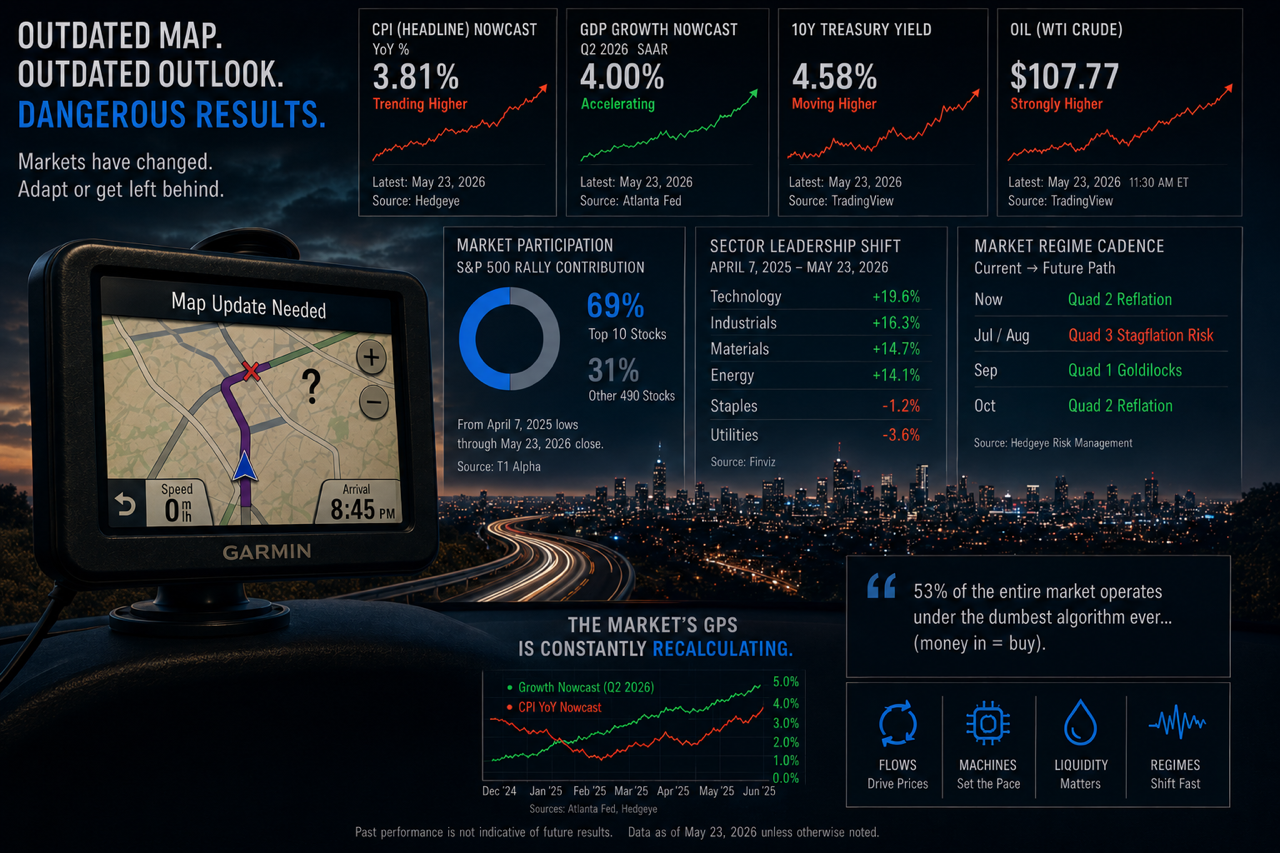

Inflation nowcasts were projecting CPI accelerating toward +3.62% YoY, with expectations pushing closer toward +4.0% as energy pressures intensified. At the same time, growth continued to accelerate with Hedgeye risk management’s framework shifting toward a near-term Quad 2 reflationary backdrop.

In plain English?

Growth stopped deteriorating fast enough … while inflation stopped decelerating altogether. Markets responded accordingly:

- equities ripped higher,

- cyclicals regained leadership,

- higher beta areas outperformed,

- commodities strengthened,

- Treasury yields pushed materially higher,

- and systematic flows accelerated the move.

But beneath the surface, things were not nearly as clean as the headline indices suggested.

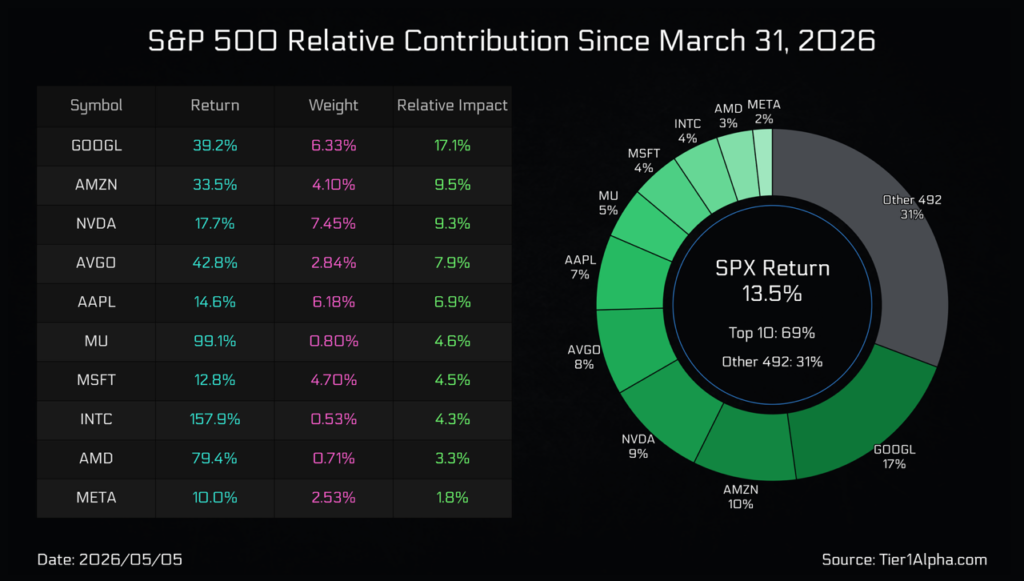

As the chart above from @t1alpha shows, while the S&P 500 rallied roughly +13.5% off the lows, nearly 70% of the move came from just 10 stocks, led primarily by AI, semiconductor, and mega-cap technology names. Meanwhile, the other 492 stocks combined contributed barely 31% of the advance.

In other words, the market was indeed moving higher … but participation underneath the surface remained surprisingly narrow.

We saw similar dynamics during portions of last April’s rally as well, which is one of the reasons we’ve continued adjusting our S&P modeling process to better capture concentration, passive flows, and machine-driven liquidity beneath the surface.

Cap-weighted indices can increasingly distort what’s actually happening underneath the hood.

- The bulls point to undeniable strength in price action.

- The bears point to narrow breadth, stretched valuations, and bubble-like concentration.

Truthfully?

Both observations can simultaneously be true.

Markets have absolutely been trading a reflationary Quad 2 setup … but through an increasingly concentrated, flow-driven structure dominated by mega-cap leadership, passive inflows, and systematic positioning.

And increasingly, modern markets pull those signals forward far faster than most investors realize.

Why experts sound terrified

Despite markets correctly identifying the reflationary Quad 2 setup into May and June, many investors and Wall Street strategists still sound terrified.

To be fair, their concerns aren’t irrational. On the surface, there’s plenty to point to:

- elevated valuations,

- narrow breadth,

- concentration in mega-cap technology,

- rising Treasury yields,

- and increasingly speculative behavior surrounding AI.

Comparisons to:

- 1999,

- the Dot-Com bubble,

- the Nifty Fifty,

- and prior speculative manias dominate the conversation.

Some of those concerns may eventually prove correct. But there’s a major difference between identifying long-term risk and successfully navigating the path markets take in the meantime.

That distinction matters because markets increasingly behave more like liquidity systems than traditional valuation-driven models dominated by:

- passive flows,

- ETF allocations,

- volatility targeting,

- and machine-driven positioning.

I understand the old framework well because I spent years operating inside it institutionally.

Traditional valuation analysis absolutely mattered in environments where:

- active management dominated,

- passive flows were limited,

- information moved slower,

But today? The machine often matters more than the spreadsheet.

Markets can remain stretched and momentum-driven far longer than traditional valuation models would suggest possible.

Yet the fear narrative persists as many investors continue forcing modern market behavior into frameworks that struggle to explain:

- momentum persistence,

- concentration dynamics,

- passive buying pressure.

To be fair, the bears aren’t entirely wrong. The narrow breadth, concentration, and valuation concerns are all very real … but this is more of a symptom of current market structure … which feeds the loop. Modern markets don’t collapse simply because valuation experts believe they “should.”

Markets typically break when policy shifts, liquidity changes, flows reverse, positioning unwinds, and/or growth and inflation materially shift.

Which brings us to where the current setup may become slightly more challenging…

Because while markets have spent the last several months correctly pricing reflationary Quad 2 dynamics, they may soon begin looking ahead toward a very different monthly quad cadence altogether.

The monthly quad cadence

Markets constantly discount where the puck is going, not where it currently sits, often pulling forward the next macro regime well before the underlying data fully reflects the shift.

Which brings us to the current monthly quad cadence.

As it stands today, markets have largely been trading a Hedgeye Quad 2 environment defined by:

- accelerating inflation,

- coupled with accelerating growth

However, the projected monthly framework should temporarily raise those bunny ear antennas as markets begin looking ahead toward anticipated Quad 3 dynamics during the summer months.

| Period | Expected Quad | Likely Market Character |

| May / June | Quad 2 | Reflation, strong tape |

| July / August | Quad 3 | Choppier markets, higher volatility |

| September / October | Quad 1 → Quad 2 | More constructive backdrop |

Again, markets don’t simply trade each calendar month in a vacuum … they are constantly pulling forward the most prevailing regime discounting these transitions as they digest ALL of the global data, price, volume, volatility … in real time.

Which means markets may begin pricing July and August’s anticipated stagflationary dynamics well before the calendar flips, even while portions of June still appear reflationary.

Just because Quad 3 environments tend to create:

- slowing growth,

- narrower leadership,

- higher volatility

That doesn’t automatically imply:

- recession,

- market collapse,

- or some catastrophic bear market.

But it does often create more selective and less forgiving market environments.

Underneath the surface, portions of that transition may already be emerging, with sectors such as Financials and Industrials recently losing both momentum and trend support.

Though, if markets do begin pulling forward September’s anticipated Goldilocks (Quad 1) transition and October’s projected return toward Reflation (Quad 2) early enough, the possible choppy summer environment is likely to eventually give way to another constructive setup into the back half of the year.

Should the current monthly quad cadence plays out as expected, the next several months may look very different from the recent reflationary move off the March/April lows.

However, that does not necessarily imply recession or some catastrophic market collapse.

Though it does suggest markets may become increasingly more difficult beneath the surface as participants begin pricing Quad 3 dynamics.

Many investors still think in binary terms:

- bullish or bearish,

- recession or expansion.

The bears continue waiting for valuations to matter immediately … while the bulls continue assuming every dip should behave like the last several years.

We’ll simply continue to follow the signals should markets transition into a more volatile and selective phase.

Between now and then, prudence likely matters more than prediction … because the biggest risk often isn’t being completely wrong … it’s remaining positioned for the previous regime while markets quietly begin repricing the next one.

Final Thoughts

When my wife and I first came to Raleigh in 2009, we thought the problem was the area … it wasn’t.

The problem was the map we were using.

The GPS wasn’t technically “wrong” … it was outdated. Raleigh was changing faster than the system could update itself.

And that’s exactly where many investors find themselves today … attempting to navigate markets dominated by:

- passive flows,

- systematic positioning,

- machine-driven liquidity,

- and rapidly shifting rate-of-change dynamics…

… using archaic tools under extremely different conditions.

That doesn’t mean valuations or concentration risk no longer matter … but obnoxious valuations shouldn’t surprise anyone when 53% of the entire market operates under the dumbest algorithm ever … (money in = buy) … at what price?! Doesn’t matter … at what valuation?! Doesn’t matter.

That’s why process and flexibility matter as we potentially transition toward a more volatile, difficult summer backdrop. … and why we continue focusing heavily on signals, rate-of-change, market structure, and evolving liquidity dynamics … rather than … static narratives, political noise, or emotionally driven headlines.

Truthfully, none of us know exactly how the coming months will unfold … but what we do know is this:

The market’s GPS is constantly recalculating … and investors still relying on outdated maps may eventually find themselves very lost.

Markets will eventually face volatility, pullbacks, and deeper corrections. They always do. The real question is whether your process is adaptive enough to recognize when the map is changing in real time.

If you’d like help stress-testing your retirement, investment, or overall financial plan against an increasingly fast-moving market environment, we’d be happy to oblige.

At Other Side Asset Management, we begin every relationship with a complimentary comprehensive retirement income plan designed to evaluate:

- income needs,

- investment positioning,

- tax considerations,

- Social Security strategies,

- insurance and long-term care exposure,

- estate planning considerations,

- and the overall durability of your financial picture.

No pressure. No obligation. Just a disciplined process designed to help families navigate an increasingly complex financial landscape with greater clarity and confidence.

And perhaps most importantly … with an updated map!

Schedule your free consultation today.

As always … Good investing!!

Mitchel C. Krause

Managing Principal & CCO

4141 Banks Stone Dr.

Raleigh, NC. 27603

phone: 919-249-9650

toll free: 844-300-7344

mitchel.krause@othersideam.com

Please click here for all disclosures.