In This Article

Announcements

We have two brief announcements this quarter; having poured a tremendous amount of work into both of them, we hope you take the time to read them.

Building our future Legacy starts with a Strong Foundation.

When we opened our doors, a primary goal was to foster change. We believe we accomplish this by challenging investors to think different, offering an alternative viewpoint to the traditional narrative marketed or “sold” by most in the industry.

Though, bringing about change within the industry isn’t where we wanted to stop, it’s not the best we can do; we don’t believe it should stop there. Today, our announcement goes deeper; it’s focus it to bring about real change, social change. It is the foundation of what we hope will become our future legacy.

Other Side Asset Management is proud to introduce our new Philanthropy Partnership

This partnership leverages the power of the collective as we tie a simple introduction directly to philanthropic giving, and we’re doing so in what could be a tremendously impactful way. All it takes is an introduction…

We’re asking for is a seat at the table…

Simply said, should you introduce us to a friend, attorney, neighbor, co-worker, physician, chiropractor, business owner, head of a non-profit; should you let us talk/present to a group, a business association or trade group (small or large), and any “advisory business” be generated from that introduction, Other Side Asset Management will donate 40%* of “advisory business revenue” (*less custodial & performance reporting fees) – to the qualifying charity/non-profit/501(c)(3) of your choice.

There is no out of pocket expense to hear our story.

Most investors are already paying fees to their current advisor. In most scenarios (clearly not all), we (Other Side Asset Management) can reduce the collective fees many are paying, while at the same time, we are willing to donate a generous portion of “advisory business” revenue to help drive social change.

We want to give back, we want to foster change, we want to help society as a whole – our hope is others will follow our lead, please consider allowing us to tell our story, together, we can change lives.

We ask that you visit our Philanthropy Partnership page on our website for full details…

Change for the better

For better or worse (we believe for the better), this will be the last quarterly resembling what many of you have become accustomed to. What began as a way to document our thoughts while educating and enlightening our clients and readers, in its current form, our quarterly simply contains more information than most care to digest in a sitting.

As we’ve discussed in the past, Other Side Asset Management is built around our clients. Those who invest with us often think different, an attribute and quality we preach, support and greatly respect. While most of you do think different, there are common threads amongst the group. If we hear similar feedback from a handful, it’s likely that it’s affecting more than just the few.

After quite a bit of work, we’ve finally launched our website www.othersideam.com. We believe it to be clean and modern; a representation of who we are, how we think and what makes us different. Aside from telling our story, with the help of a little technology, our website now allows us to streamline how we communicate with you, hopefully enhancing our client experience.

In an effort to reduce the size of our quarterly, yet continue to deliver pertinent content in a timelier manner, we have decided to create a blog. Our initial plan is to release one note per month with no set schedule. This will also allow us to focus our quarterly efforts more on the portfolio than macro environment while providing brief and easily digestible information throughout the quarter.

Our website also provides us with a central location to archive our notes for easy reference, while it also will include additional enhancements allowing users who want to read the note in its entirety to do so or provide quick links for others to navigate specific sections that might be of greater interest.

Our commitment is to continually provide you with the information we would want if our roles were reversed in a clean, easy to use format. These adjustments will hopefully allow us to achieve these goals; quality content, smaller doses spread out over time.

We believe these changes will positively impact the majority of who read our notes.

Martin Zweig

Before all the glitz, glamour, sensationalism and sadly, monetization of current financial media empires, PBS (Public Broadcast Service) aired the mundane, relatively boring, yet extremely informative weekly broadcast of, “Wall Street Week”. For nearly 35 years, host Louis Rukeyser, would show up in living rooms around the country on Friday night summarizing major events that took place on Wall Street throughout the week, while also discussing notable events on horizon. This was THE financial news of the time.

Rukeyser would often host well-known, industry ‘insiders’ as guests. Martin Zweig, was a regular. One of Wall Street’s most brilliant minds, Zweig didn’t re-invent the wheel; in fact, it’s been said that many of Zweig’s methods came from famed Wall Street trader, Jesse Livermore. We’ve frequently mentioned Livermore, quoting excerpts from, “Reminiscences of a Stock Operator – With New Commentary and Insights on the Life and Times of Jesse Livermore”, by Edwin Lefevre (forward written by Paul Tudor Jones).

Zweig’s notoriety rose when he accurately predicted the stock market crash of 1987, or ‘Black Monday’ as most know it; he did so the weekend prior on, Rukeyser’s Wall Street week.

Zweig, founded Zweig-DiMenna Associates in 1984 with then protégé Joe DiMenna. Decades later, DiMenna has been touted by ‘industry insiders’ as “one of the best stock pickers no one has ever heard of”. With one of the best stock pickers by his side, Zweig still utilized many basic principals that may sound familiar to our investors and readers. While paraphrasing, Zweig wanted to be fully invested in markets when indicators were ‘positive’ and to sell stocks as indicators became ‘negative’; risk management and loss mitigation were crucial to Zweig’s strategies.

Zweig-DiMenna treated ‘stock picking’ and ‘macro risk controls’ as two separate issues – two completely different full time jobs. In studying Zweig, according to long-time Zweig partner Michael Shaus in a recent interview with financial newsletter icon Jim Grant; Zweig would determine how much risk was in the markets at any singular point in time; ‘risk control’ was determining how much money they should have invested in and out of stocks based upon how much risk there was in the markets at any given point. This strategy differs from those merely attempting to generate alpha by just owning stocks.

By examining monetary policy (the fed, interest rate policy, etc), the “tape” (how stocks are currently trading) and sentiment (a measure of investor emotion, which you all have heard us talk about before) – Zweig would determine where he believed the risk to be, and he was extremely good at it.

While you can learn more about Zweig’s thought process by reading his book, “Winning on Wall Street”, I want to leave you with two excerpts, which couldn’t be more poignant given current market conditions… you can find the below excerpts in the introduction section pages xix and xxi.

If I were a genius –and there aren’t any in this business – I would have sold everything before the break, bought even more puts, held them all right up to the bottom day and made zillions. But that’s not reality.Reality is cutting risk to the bone when the indicators weaken, hoping you can make a few bucks when conditions are good, and praying that you’ll survive crashes, plagues, and earthquakes long enough so that someday you’ll see the pleasant light of another bull market and have some money left to play it…

He continues…

Patience is one of the most valuable attributes in investing. I liken it to a great baseball hitter such as Wade Boggs nowadays or Ted Williams in my youth. The key to their success is to wait for the fat pitch to hit and not swing from the heels at just anything. The idea is to work the pitcher into a hole and get the count to 2-and-0 or to 3-and-1. That forces the pitcher to throw strikes…often fastballs. In other words, if the hitter is patient, he tries to work the odds into his favor. Then, and only then, does he take a real rip at the ball.

It’s about the same in the Stock Market. I try to “work the count” in my favor by waiting for the indicators to get very one-sided before “swinging from the heels” with an aggressive strategy. If I don’t find the indicators producing very good odds in one direction or the other, I’m content to play defensively and just bide my time.

Note: Per Zweig, “there are no geniuses in this business”, and yet, most who are successful have similar traits. What are those traits? While it’s not written, humility, the best don’t consider themselves to be the best; followed by “cutting risk to the bone” and “patience”, and “being content to play defensively” (when indicators aren’t producing very good odds).

Things have obviously changed since Martin Zweig and Joe DiMenna founded their firm in 1984. While hindsight is 20/20, it was immediately following the crash of 1987 where then Fed chairman, Alan Greenspan immediately directly tied the Fed to Asset prices.

Over the last 30 years, the Fed, via both interest rate and monetary policy has become a much greater influence on “the tape”. Some (myself included) would argue they have BECOME “the tape” (more on this later). Though, even with the Fed becoming a more pronounced market influence, Zweig’s investing principals are timeless; he looked at indicators like ‘sentiment’ (investor emotion) before computer programs and software made it more easily to track. I say this understanding that he was a big believer in certain cliché’s that currently exist today, such as “don’t fight the Fed” and the “trend is your friend”.

Why do I tell you the story of Martin Zweig now?

We have written for quite some time about sentiment, contrarian indicators and more specifically the Fed. We have likened our current investing environment to driving a car – suggesting now might not be the right time to be full throttle on the gas peddle as many indicators point to what is likely a hair pin turn ahead.

While I never had the privilege of meeting or working for Martin Zweig, if he were alive today, my hunch is he’d be closer to full throttle right now than most currently are (including us). With an accommodative Fed, strong tape and reasonably good sentiment (many hedge funds still sitting on the sidelines), the environment seems ripe for him to press his luck.

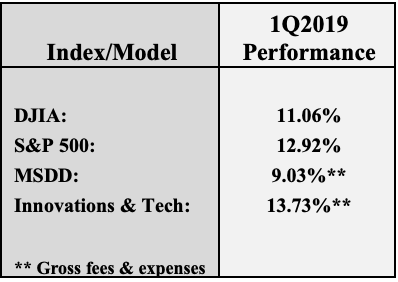

Our ‘perceived’ Achilles heel for the quarter, if anything, would have been our ‘macro risk controls’ i.e. how much we should have invested. Picking ‘winning’ stocks hasn’t been our challenge; on a cash adjusted basis our models are outperforming traditional benchmarks.

Most individuals will look at the performance of our primary model (MSDD), the S&P and then first full quarter of the Innovation and Technology portfolio and say, “I want that one – I want the Innovations portfolio”, until you don’t… Until the downside wakes you up to the reality that most don’t have the ability to stomach the downside volatility that portfolio and markets have yet to see… The Tech bubble of 2001 wasn’t all that long ago – and now you’re 18 years closer to retirement than you were back then. Do you really want to be staring down retirement in the middle of another Tech bubble or Mortgage-meltdown scenario?

Having said that, let’s look at some numbers. If you’ve read our announcements, you’ll note we are in the process of change, we are working on a more centralized location for performance numbers… please bear with us.

Having said that, let’s look at some numbers. If you’ve read our announcements, you’ll note we are in the process of change, we are working on a more centralized location for performance numbers… please bear with us.

While Martin Zweig believed in ‘not fighting the Fed’ and ‘the trend is your friend’, I’d like to note two things we believe to be important…

- In the first excerpt, he talks about praying to survive crashes – we don’t pray – we rely on a strict discipline and capital preservation strategies.

- He also believed in knowing “When to part company with the crowd”.

- While the Fed tied interest rates to asset prices in 1987, it’s only been recently that Global Central Banks have been unable to resuscitate the economy with near zero interest rates and stimulus packages after such a prolonged period of time. We are in completely unchartered waters with interest rate and monetary policy as well as both volume of and debt quality.

We are still cautiously optimistic regarding the “Melt-up”, we have been adding positions to the portfolio; these are companies we believe are a “value” relative to their revenue growth, which should accelerate in a prolonged low interest rate environment.

However, it’s important to note, when the entity that holds the fate of the global markets in its hands has no clue (literally), I hesitate to bet the ranch!

“Many participants observed that if uncertainty abated, the Committee would need to reassess the characterization of monetary policy as “patient” and might then use different statement language” FOMC minutes February 20, 2019

Or better yet, this admission:

“Many participants suggested that it was not yet clear what adjustments to the target range for the federal funds rate may be appropriate later this year.”

You seriously can’t make this sh*t up!

While we don’t know exactly what Martin Zweig would be doing at this exact moment in time, we believe he would be pretty aggressive at this moment in time. Our participation has steadily grown as markets as “the tape” has gained strength; we will continue to do so until there is a more clear opinion from FOMC officials or we see credit begin to tighten. We have firmed some of our capital preservation strategies and initiated some ‘partial positions’ as a means to gain participation without firing all of our bullets at one time. We still have more cash to deploy and will do so accordingly.

So from one investing legend to another, we turn from the story of Martin Zweig to Warren Buffet’s thoughts via his most recent letter to shareholders… As usual, there are quite a few nuggets of gold to harvest from his words…

Buffett Annual Letter

Warren Buffett released his annual letter (scorecard) to Berkshire Hathaway shareholders on February 23, 2019. Within hours its read front to back, back to front and analyzed. Every investor will pull from this report what he or she feels most poignant; below we share ours.

“Berkshire will forever remain a financial fortress. In managing, I will make expensive mistakes of commission and will also miss many opportunities, some of which should have been obvious to me. At times, our stock will tumble as investors flee from equities. But I will never risk getting caught short of cash.” ~ Warren Buffett; February 23, 2019 – Annual letter to Shareholders.

As mentioned above, on a cash adjusted basis, our models outperformed traditional benchmarks in Q1. We know, we don’t live in a cash adjusted world; this fact is not lost on us. What we also understand is the most recent “V” shaped recovery we are currently witnesses of is by no means normal, either, especially with such an indecisive FOMC.

Our primary model is designed to mitigate catastrophic loss in times of crises. As discussed in our previous note, from December 1st through the December 24th market lows our portfolio was down roughly 9.5% vs. the S&P’s negative 16.7%.

Following what was arguably the worst December on record for equity market performance since 1929, given the current debt/credit environment we’re comfortable in not risking getting caught short of cash.

Back to Mr. Buffett as he made some astonishing admissions in his writings:

“In the years ahead, we hope to move much of our excess liquidity into businesses that Berkshire will permanently own. The immediate prospects for that, however, are not good: Prices are sky-high for businesses possessing decent long-term prospects.

That disappointing reality means that 2019 will likely see us again expanding our holdings of marketable equities. We continue, nevertheless, to hope for an elephant-sized acquisition.”

One of the greatest value investors of all time can’t seem to find an acquisition because everything they look at is over-valued – again:

“Prices are SKY-HIGH for businesses possessing decent long-term prospects”.

Yet, it is extremely important for people to read this next excerpt.

“My expectation of more stock purchases is not a market call. Charlie and I have no idea as to how stocks will behave next week or next year. Predictions of that sort have never been a part of our activities. Our thinking, rather, is focused on calculating whether a portion of an attractive business is worth more than its market price.”

Buffett recognizes there is often a disconnect between the market price of an equity vs. it’s overall “value” – he’s seen his stock fall by nearly 50% twice in the last 20 years and yet, this fluctuation is ‘noise’ to Buffet; but it’s important to note he can afford it to be, he’s an 88-year old billionaire who lives in a more modest home than most of you reading this note.

Whether you are retiring or just getting started, how comfortable will you be watching your equity values drop by 50 – 90 percent respectively? What happens to your retirement income if you’re actively withdrawing money from your investment accounts? Most believe they have the stomach to handle a situation like this? History and numerous studies suggest not…

We’re paraphrasing words from our 3Q2018 quarterly, however, in the last 20 years, the best of the best have fallen HARD, some more than once. Microsoft, McDonalds, Home Depot and Disney have all fallen by roughly 70% or more – Apple, Intel and Starbucks have fallen by more than 80% – Amazon and Citibank have fallen more than 90%. Decades later some have yet to fully recover.

While we’ve taken a cautious approach coming out of one of the worst December in history, responsible investing requires a little prudence and as Martin Zweig suggests, patience.

In our fourth grove, Berkshire held $112 billion at yearend in U.S. Treasury bills and other cash equivalents, and another $20 billion in miscellaneous fixed-income instruments. We consider a portion of that stash to be untouchable, having pledged to always hold at least $20 billion in cash equivalents to guard against external calamities. We have also promised to avoid any activities that could threaten our maintaining that buffer.

When one of the best value investors of all time can’t find an acquisition due to sky-high valuations and holds over $120-billion dollars in cash or cash equivalents at the end of 4Q2018 and in the same vein, “I, too, will never risk getting caught short of cash” – In an effort to guard against “external calamities”. Our capital preservation strategies are our insurance policy that takes care of the “What if” questions while also protecting against requiring a “Hope and pray” strategy.

More Join Our Island

“All too often we dismiss the small things or nuances as not mattering burying them in the “fine print”. Then we act surprised when something “unforeseen” happens, only after which, we come to the realization that those small things – mattered.” ~ Other Side Asset Management, Special Report January 2018

In early March, both Dallas Federal Reserve President Robert Kaplan and the Bank of International Settlements (also known as the BIS) recently made some astonishing admissions, buried in the “fine print” of independently written reports and ignored by just about everyone.

The Dallas Federal Reserve President (Robert Kaplan) needs no introduction his position is about as self-explanatory as it gets, but many may not know who or what the Bank of International Settlements is, so for those unfamiliar, The Bank of International Settlements (BIS), is often referred to as the Central Bank of the World’s Central Banks.

While the Bank of international Settlements doesn’t often make headlines, though, as the Central Bank to the World’s Central Banks, it’s safe to say they are a relatively important entity… and while the Dallas Fed is currently a non-voting ‘Alternate Member’ of the FOMC, they do become a voting member in 2020, again, a fairly influential voice.

On March 5th, 2019, Dallas Fed president Kaplan, published a paper echoed many of the concerns we have emphasize for years now. His focus was the “implications of rising levels of BBB and less-than-investment grade debt” (this is not new news at this time).

From Dallas Fed President, Robert Kaplan’s March 5, 2019 report:

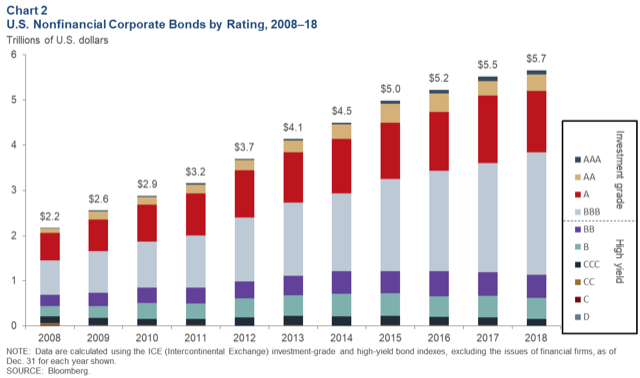

Many of you understand why the above chart scares the heck out of me. Last year we wrote about in detail, a structural flaw in our financial system and why the BBB market is applying significant pressure to that ‘point load’ (or structural flaw).

It’s extremely important to understand a BBB bond rating is THE line in the sand that determines what companies can or can’t own based upon corporate structure and governing bylaws (Spoiler Alert: the majority can NOT own junk/high yield debt). BBB = Investment Grade (IG) anything below is junk or high-yield.

From Kaplan:

“In a downturn, some proportion of BBB bonds may be at risk of being downgraded to less than investment grade. These downgrades, if they happen in sufficient size, could create dislocations for investors who tend to have specific allocations or restrictions based on credit-rating categories. These dislocations could further negatively impact credit spreads and market access for more highly indebted companies.”

While the above is extremely pertinent and should sound familiar, it’s the next admission that speaks to the real news:

One further issue is whether there is sufficient liquidity in the various corporate debt markets. Ample liquidity is particularly important in the event of market stress or dislocation.

As important as this above statement is, I’m going to turn to the BIS for a minute, for while reading these reports independently is enlightening, reading them in conjunction with each other is even more so impactful. The BIS released their quarterly review on March 5, 2019. (If you think my quarterlies are long, their report was 152 riveting pages). In an education by headline world, reports like these are often overlooked and under-read.

The BIS explains in plain English the ramification of Kaplan’s ‘possible liquidity concerns’; dedicating an entire section to investment mandates beautifully connecting the dots between their words and Kaplan’s:

From page 12 of the BIS report:

“Investment mandates and fire sales: the case of mutual funds and BBB bonds”

“Rating-based investment mandates require portfolio managers to hold assets above a minimum credit quality. Such mandates often apply to corporate bond mutual funds, and allow investors to easily choose the desired risk exposure, often focusing on the investment grade segment.”

Sound familiar? Keep reading, there’s more…

Since the GFC (Great Financial Crisis of 2008), investment grade corporate bond mutual funds have steadily increased the share of BBB bonds in their portfolios. In 2018, this share stood at about 45% in both the United States and Europe, up from roughly 20% in 2010.

As interest rates remained unusually low post-GFC, portfolio managers were enticed by the significant yield offered by BBB-rated bonds, which was substantially higher than for better-rated bonds.

All they are saying here is Investment managers loaded up on BBB debt to reach for yield. They are delicately blaming the consumer… ‘Customers wanted yield, damn it, we’ll give them yield’.

For those who don’t read footnotes, this is why we urge you to do so. This is one of the most important statements in the entire 152-page report, and yet it’s literally buried beneath “Graph B” the 4 charts on page 12:

While attractive to investors that seek a targeted risk exposure, rating-based investment mandates can lead to fire sales. If, on the heels of economic weakness, enough issuers were abruptly downgraded from BBB to junk status, mutual funds and, more broadly, other market participants with investment grade mandates could be forced to offload large amounts of bonds quickly.

Circling back to Kaplan and the importance of his words coupled with the BIS’s – the junk bond market is literally a fraction of the size of the Investment grade market. Per the BIS, if enough issuers were downgraded, the junk market wouldn’t have the size (or liquidity – Kaplan’s concern) to absorb those freshly downgraded bonds. Creating fire sales or a complete bond market freeze ((my words) which neither mentioned – but we have numerous times in the past).

It was our most stark and focused warning on this specific topic, writing about it well over a year ago. In January 2018, we argued… “What happens when a structured system, experiences a breakdown?” We explored ‘When liquidity dries up’. When a single downgrade could be 15% of the entire junk market (AT&T) what happens if 5 highly leveraged companies were downgraded, totaling over 45% of the entire Junk market?

We detailed the structural flaw in the system most continue to overlook.

In understanding the largest bond buyers in the financial markets (less central banks) are primarily tied to owning IG bonds and the Triple-B market now represents nearly 50% of all IG paper with the lowest tranche representing 40% of that segment, should a percentage greater than what many expect be downgraded ‘one single notch’ to BB, it is very likely high-yield markets won’t be able to absorb such volume; large price distortions (think Toys R Us bonds) could become more the rule vs. the exception.

We stressed:

“It all keeps coming back to “structure”; the volume of debt stressing the point load of the Triple-B/junk line is massive, downgrade(s) trigger sales of bonds and dislocation in markets as the volume of bonds being sold dwarfs the size of the natural buyers able to purchase”

We pleaded… in over 20 pages (reiterating the importance, because it bears repeating)

“I want to make it clear… what keeps me up at night is more of a structural problem within our financial system then anything.”

A mountain of BBB debt has grown exponentially in front of all of our faces and we’re the only ones asking why that tranche? How can such a large percentage fall into that particular tranche? The BIS just told you why…

Rating-based investment mandates require portfolio managers to hold assets above a minimum credit quality.

And they hid the dangers in the fine print:

Rating-based investment mandates can lead to fire sales. If, on the heels of economic weakness, enough issuers were abruptly downgraded from BBB to junk status, mutual funds and, more broadly, other market participants with investment grade mandates could be forced to offload large amounts of bonds quickly.

The majority of investable money mandates Investment Grade purchases. It would be much easier and shorter to type, “mutual funds and, more broadly, other market participants with investment grade mandates” but then you don’t fully understand the impact of “other market participants with IG mandates” – which includePension funds, Mutual Funds, Age-based mutual fund portfolios, Bond ETF’s, private wealth managers, Financial Institutions, Insurance companies, corporations, and the list goes on… In general, the great majority of these companies have ratings-based investment mandates preventing them from both buying junk bonds, as well as holding junk bonds if a downgrade occurs; which equals forced selling (fire-sales and liquidity freezes).

So there it is, if you don’t want to believe me, if you don’t value the words of a small investment shop out of Raleigh NC? If you don’t think REAL risk exists in credit markets, maybe the words of the Dallas Fed and the BIS (the Central Bank of the World’s Central Banks) will provide more credibility?

If you still trust the ratings agencies after their AAA-rated Collateralized Mortgage Obligations nearly destroyed the economy in 2008, I don’t know what to tell you?

Without a BBB rating from credit agencies, many deals over the last decade wouldn’t have gotten done, period, FULL STOP. Think of the volume of money Wall Street investment bankers would have lost if they couldn’t raise the necessary capital to get these deals done! How much revenue do you think investment bankers made on the AT&T acquisition of Time Warner? A single deal valued over $108.7-billion (mostly debt)?

While I believe in the melt-up thesis, there is a storm brewing of significant proportion and this is why the Fed immediately reversed course, it sure as heck wasn’t their DATA.

The Fed’s Reversal

Dallas Fed President Kaplan concluded his note touching on interest rate sensitivity:

“I am also sensitive to these corporate debt developments in light of the historically high level of U.S. government debt and the forward estimates for the path of government debt to GDP. An elevated level of corporate debt, along with the high level of U.S. government debt, is likely to mean that the U.S. economy is much more interest rate sensitive than it has been historically.”

In a nutshell, one shouldeasily conclude from reading his note…

We can’t raise rates anymore because every existing entity from corporations to governments have taken on way too much debt since we cut borrowing rates to virtually zero for such and extended time frame…

Let’s rewind.

The FOMC had been screaming ‘hawkish’ rhetoric from the onset of Fed Chair Powell’s appointment. (i.e. strong economy in need of rate increases).

Though, when faced with one of the most damning Decembers on record for financial markets, the Fed went from super ‘hawkish’ to immediately ‘dovish’ – literally overnight. In what amounts to, “in the blink of an eye”, discussions of rate increases were replaced with being ready to “use all monetary tools in the Fed’s toolbox”.

Oddly enough, the FOMC preaches “data dependency”, and yet, none of the data they cite as economic barometers have changed. Outside of a nominal reduction of 10-20 basis points to their GDP numbers, there has been no real change of significance to core PCE, inflation or GDP.

So here we are today, markets have rallied and a “V” shape recovery has ensued! We now sit at levels in financial markets no more than a few percentage points below where we were prior to the November/December sell-off of 2018. Then, the Fed was hawkish and tightening, today they are dovish and accommodative while staring at virtually the same data?

Do you still question what data the fed is dependent on?

Yet, there is a much bigger question that remains unanswered (one which no one knows the real answer to):

Do equity prices continue to rise with the return of an extremely dovish Fed, driving interest rates lower as ‘easy’ money (credit) returns OR do investors finally demand higher interest rates for the risk they are taking in credit markets?

A very real case can be made for both, higher interest rates being demanded for by investors due to a slowing global economy, sending both bond and equity markets into negative territory.

Coordinated central bank intervention has been extensively detailed in Nomi Prins book “COLLU$ION – How Central Bankers Rigged the World” and based upon this work, has been very influential and powerful.

In April 2016, at his office in Brasilia, Joao Barroso, senior advisor at Brazil’s central bank (BCB), considered the effect of capital inflows on Brazil as connected to the Fed’s artisanal money policies. According to his original analysis, over 54 percent of capital inflows from the United States to Brazil were caused directly by QE. Most of that capital flowed into Brazil’s bond market, because rates there were so much higher than in the rest of Latin America.

Barroso also estimated that up to 65 percent of total US portfolio flows to major Latin American countries were directly caused by the Fed’s QE, isolating out all other factors. Collu$ion; Nomi Prins, page 80

Quite a bit of research has come out of the BCB highlighted by Ms. Prins showing direct correlation of global central bank intervention to moves in global equity markets.

Marty Zweig was a “don’t fight the Fed” guy, he was a strong believer in “the trend is your friend” and from the look of things; we’re once again staring at accommodative behavior by global central banks, but he also believed in knowing “when to part company with the crowd”.

My personal bias is one of a global equity market “melt-up” (a phrase coined by Stansberry Research analyst Steve Sjuggerud), it’s a reason I believe if Mr. Zweig was alive today, he would be more open throttle than most would think to be, however the RISK in markets hasn’t disappeared. The end result will be worse than most will be prepared for. We will tackle how we are preparing for this in our conclusion…

Let’s Talk Valuation

I want to circle back to Warren Buffet for a second, for I think it’s important to comment on “valuation”. How many times have we heard, “Equity prices HAVE to fall because markets are simply way over-valued”?

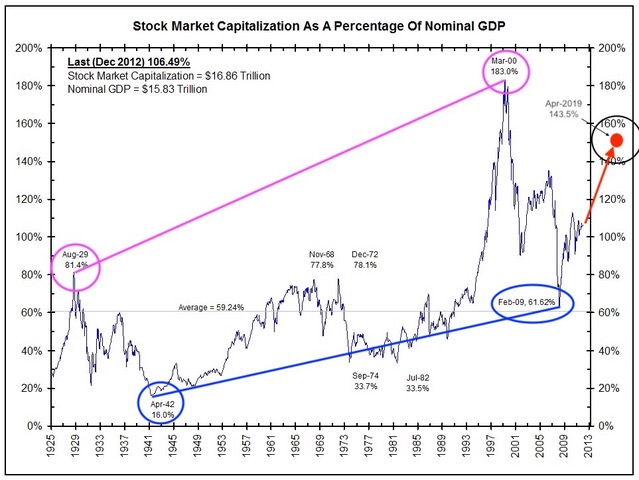

Total stock market capitalization as a percentage of nominal GDP is a financial metric often referred to as “The Buffet Indicator”. Mr. Buffet has stated this metric is, “probably the best single measure of where “valuations” stand at any given moment.”

We’ll agree that in retrospect, valuation has always proven to be important, though, the question we feel important to explore is does this metric speak to an imminent move in equity prices in either direction? How reliable is it in the moment? In taking a look at the “Buffet Indicator” from a historical standpoint, we can understand this thought process more clearly.

As you can see from the above image, the stock market capitalization as a percentage of GDP peaked at 81.4% in August of 1929 just prior to the financial market crash leading us into the Great Depression. Now compare this with the absolute peak of this metric preceding the technology bubble of March 2000 of 183.00% (follow the purple line) – “Valuation” prior to the technology bubble of 2001 was more than double that of the 1929 crash.

Similarly you can compare lows. The metric bottomed out in April of 1942 with a reading of 16% where at the bottom of the Great Recession in February of 2009 read 61.62% (a valuation 3 times that in 1942) (Blue line).

If measures of “overvalued” vs. “undervalued” can be drastically eclipsed during times of both euphoria and pessimism, while this may be a great barometer of “current valuation”, relative to history, it’s an extremely inefficient indicator for any imminent stock market move in any one direction.

Equity markets can absolutely be “over-valued” by historical measures – but there is no specific rule suggesting valuations can’t stretch from say, overvalued to grossly overvalued or to obnoxiously overvalued, before being humbled back to more normalized levels. There is no alarm that rings at the top saying – “That’s it folks – it’s over! Time to go home.”

In understanding markets could move exponentially higher from already, generally accepted “overvalued” historical measures, attempting to quantify how “high” valuations can go is often futile (in the short-term),

We’ve previously referenced, “This Time is Different: Eight Centuries of Financial Folly” by Carmen Reinhart and Kenneth Rogoff. In a word, they conclude “confidence” was the determining factor as to what brought about catastrophic loss in past bubbles dating back centuries.

If you really think about this, you may come to an awakening; the realization that “confidence” is a feeling or emotion. Hopefully you have begun to understand why we place so much study and effort on the subject of investor sentiment. In understanding emotions are by no means rational, you may then also understand why we believe so strongly in capital preservation strategies, for at times, the best analysis in the world can’t protect you from violent emotional market swings. Winners can ‘run’ much longer than they ‘should’, just as losers can fall much further. Markets are as much emotional as analytical, as it’s the emotional investor that drives the buying and selling…

Institutional investors making decisions for you every day are as human as you and I. They have emotions, too, especially when their jobs and family’s future rely on that job providing an income stream. That’s as emotional as it gets and don’t think it doesn’t affect their mindset.

Discipline to our capital preservation strategies reduced risk in our portfolio in December, solidly positioning us in cash; living to fight another day. Yes, we’re a handful of percentage points behind the S&P. I can’t guarantee we’ll make it up (there are no guarantees in this business), however, I’m very confident in our abilities over a full investment cycle.

Investing isn’t a sprint, as Martin Zweig suggests, patience is one of the most valuable attributes in investing. We, here at Other Side Asset Management, spend quite a bit of time asking the questions most don’t, and put more effort into finding solutions as to how to mitigate potential and very probably outcomes, such as…

- What would have happened if markets blew through December 24th lows by another 20% to the downside?

- What will happen to your portfolio if/when markets initially go down 20% and then another 20% and then another 20%?

- What happens if/when there is no immediate “V” shaped recovery, as it took markets nearly 25 years to break even from the crash of 1929?

- What happens when confidence erodes in the Fed’s ability to fix the problems, they themselves created?

It’s clear our current indexed world doesn’t pay attention to valuation… Passive investing is a one way bet the market will move higher over the course of time… When buying an ETF, your money doesn’t discriminate if a company trades at 8 times earnings or has no earnings at all; the ETF robotically follows its directive (be the index). Weightings are often determined by nominal equity price; admittedly, it’s a strategy that has recently outperformed the masses (and may likely continue to do so) as Central Banks are posturing to re-commit to additional coordinated, easy global monetary policy (Collusion – per Nomi Prins).

When confidence in the system wanes, many will wish they had a capital preservation strategy in place (you can use them with ETFs); but we’ve talked about this before, in great length as well. However, its importance, in our opinion, cannot be stressed enough.

Summary

On one hand, as we type, central banks around the globe are being urged to become more accommodative with their monetary policy in the name of “global economic slowdown” (the Fed); price action is currently strong in equities and sentiment is in the bull’s favor. This is an environment, I would think if around, the late Martin Zweig, would find ripe for taking?

On the other hand, virtually all debt is at record high levels; zombie companies continue to be propped up by artificially suppressed interest rates while credit quality and the BBB market continues to balloon. Valuations are “sky-high”, per Warren Buffet, so much so, they passed on making a large acquisition again last year and plan to allocate more towards market equities.

After nearly 10 years of Zero Interest Rate Policy (ZIRP), and only a short way into their hawkish policy of increasing interest rates (topping out at a mere 250-basis points) the FOMC has now put the breaks on all tightening. Per the Fed’s most recent meeting, they will be placing a hard stop on all future balance sheet roll-offs as of September 2019, leaving them with a severely bloated balance sheet of nearly $4-trillion dollars. Additionally, markets are now of the opinion there is a 50% chance of a rate cut come year-end 2019. Yes, seriously…

As we outlined, Dallas Fed president Kaplan voiced concerns in regards to what we have been saying for years now; While stated more delicately (call it politically), we can’t raise interest rates, because corporations and governments have taken on too much debt – (he didn’t go as far as to say the reason they’ve taken on too much debt is due to abnormally low rates for too long a period of time, but… do you really need him to?)

This quarter (1Q2019), both Kaplan and the Bank of International Settlements (the BIS) the Central Bank of Central Banks have finally acknowledged the issues behind the structural flaws in our bond markets as it relates to the BBB market and liquidity concerns we’ve been outlining for quite sometime, and yet, they’ve only scratched the surface.

While we’ve detailed the excessive leverage in credit markets and explosion of the BBB bond market at length, according to the “Dean of high-yield” Marty Fridson, there has also been a massive increase of CCC bonds (over 43.6%) – this also speaks to the extremely low quality of debt these days.

And still, 2018 brought us some of the strongest GDP growth in years (thank you, one off tax cuts) – while at the same time, Bianco research detailed the rise of more zombie companies (defined as those who can’t service their interest expense through operating income) suggesting a number greater than 15%, more than twice the level seen pre 2008 mortgage crises.

The Conundrum…

If we thought the current investing environment was akin to picking up nickels in front of a steamroller, we would be sharing a different opinion than our current point of view. Those who study the characteristics of late stage bull markets would argue the returns we are likely to see in the near term (especially given the Feds more dovish tone and sheet volume of global central bank intervention) could be historic.

Marty Zweig would likely tell us, that fighting the Fed has never been a good idea, nor is fighting the trend. As the cliché goes, “the trend is your friend”… which would lead some to think we should be “all-in”, right? We still say, not so fast…

The saying, “the trend is your friend…” has a conclusion, again, that damn fine print… When stated in its entirety the saying becomes, “the trend is your friend, until the end…” While the cards are aligning more and more for the late stage bull market rally we’ve been discussion, it doesn’t mean we can be irresponsible in preparation for the storm. We’ve said it before; you don’t buy hurricane insurance while staring down a CAT 5 hurricane. We can’t predict when the storm is going to reach us, but we can prepare for it. We can begin to distance ourselves from the crowd.

It’s important to remember, we’re investing, not gambling. Taking the time to assess an uncertain situation, especially during times of extremes, doesn’t necessarily mean you’re going to be left behind. It means you’re being smart.

“It’s better to walk alone, than with a crowd going in the wrong direction.” ~Diane Grant

We are performing very well on a risk-adjusted basis and while we’re talking clichés, let’s not forget this one…

Bulls make money, Bears make money, but pigs… pigs get slaughtered…

If it’s not yet clear to anyone with their eyes open, the Fed is hostage to its own bad policy and we don’t believe it’s a good position for them or any of us to be in.

Investment newsletter veteran, Jim Grant coined an analogy and I have found none better to describe the FOMC’s “dual mandate” of inflation/price stability and full employment to that of Arsonist and Fireman. Artificially suppressed interest rates fuels the asset bubble, increasing rates lights the fuse, bubble explodes, fire ensues… Then its up to them to put that fire out (reduce rates to spur the economy), rinse, repeat…

Only no one knows how long the current fuse is? Nor how big, hot or for how long the next blaze will burn? Or will the firemen even be able to put out the fire?

The bigger this (MOAB) gets, they more black powder, fuel and wood, piles up, the more people it will harm, especially for those who are unprepared. It will then become clear that betting on passive investment strategies which solely rely on an endless money supply inflating asset prices (or those active managers acting as closet indexers) was likely a bad idea?! We do not believe this will not end well for many…

In the meantime, my belief is the markets will continue to move higher based upon the Fed becoming the market. Global central bank intervention has poured over $22-trillion into financial markets over the last decade. As markets move higher and money mangers/hedge funds underperform, they will begin to push more money into equities. With negative yields on nearly $11-trillion of assets around the globe, as that money matures, it too will search for more yield. Money flow will inflate ASSET PRICES – which is a form of inflation. It doesn’t show up in your CPI or PPI numbers, because it’s marketed to you as, “The Wealth Affect”, but rest assured, it’s inflation. Call it a melt-up, call it the snowball affect, it is likely to accelerate with increased volatility.

The question is how much longer and how far can these markets move to the upside before the next credit default cycle hits. What percentage of “zombie companies” will easy credit support before investors wake up to the reality that if a company can’t make the interest payments on their debt at ridiculously low interest rates, how will they do so as borrowing costs rise? How much credit will banks lend to these zombie companies before they say, no more?

No one has the answers to these questions, but when banks pull back their lending, that’s when the music really stops. When companies can’t make payments on their debt as banks are literally handing these companies money at virtually zero borrowing cost we’ll not only see the companies who were extended the credit go bad, but we’ll also see the banks who were handing out this assistance.

In the meantime, we’re positioning ourselves for the impending “melt-up”. The names, which are likely to outperform in times like these, are those companies, which can steadily increase internal revenue growth fueled by cheap money. As we become more tech centric a society, we believe Internet security will be an enormous benefactor. We can’t ignore the explosion of “gaming”, not only here at home, but abroad. Additionally, improvement and technology within the medical device field is becoming more real by the day (personal biases aside). These companies are likely to see obnoxious amounts of capital pushed their way, while the “boring” consumer staples are likely to suffer… Until the rotation begins and they don’t…

Disclosure

** We continue to work on getting our flagship model’s numbers audited from a performance standpoint. In opening our new firm (OSAM), performance will only be able to be officially audited as far back as the complete sets of statements we receive from clients. This may remove data points from our official numbers upon audit completion affecting 2016’s reportable performance number. Numbers reported are gross fees and commissions as we have a sliding fee scale based upon assets.

Disclosure: The commentary, analysis, references to, and performance information contained herein, except where explicitly noted, reflects that of Other Side Asset Management, LLC, a registered investment adviser. Opinions expressed are as of the current date and subject to change without notice. Other Side Asset Management, LLC shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions contained herein or their use, which do not constitute investment advice, are provided as of the date written, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. This commentary is for informational purposes only and has not been tailored to suit any individual. References to specific securities or investment options should not be considered an offer to purchase or sell that specific investment. Other Side Asset Management, LLC does not guarantee the results of its advice or recommendations, or that the objectives of a strategy will be achieved. Performance shown herein should in no way be considered indicative of, or a guarantee of the actual or future performance of, or viewed as a substitute for any portfolio invested in a similar strategy. Performance data shown represents past performance, which does not guarantee future results. Investments in securities are subject to investment risk, including possible loss of principal. Prices of securities may fluctuate from time to time and may even become valueless. Securities in this report are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. Before making any investment decision, investors should read and consider all the relevant investment product information. Investors should seriously consider if the investment is suitable for them by referencing their own financial position, investment objectives, and risk profile before making any investment decision. There can be no assurance that any financial strategy will be successful. All data presented is based on the most recent information available to Other Side Asset Management, LLC as of the date indicated and may not be an accurate reflection of current data. There is no assurance that the data will remain the same. This commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results to differ materially, and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. No graph, chart, or formula in this presentation can be used in and of itself to determine which securities to buy or sell, when to buy or sell securities, whether to invest using this investment strategy, or whether to engage Other Side Asset Management’s investment advisory services. In addition to the Other Side Asset Management’s advisory fee, overall returns may be reduced by expenses that an investor may incur in the management of the investor’s account, such as for custody or trading services, which will vary by investor and may exceed the trading costs reflected herein.