In This Article

Lighting Money On Fire

“We are a community company committed to maximum global impact. Our mission is to elevate the world’s consciousness. We have built a worldwide platform that supports growth, shared experiences and true success. We provide our members with flexible access to beautiful spaces, a culture of inclusivity and the energy of an inspired community, all connected by our extensive technology infrastructure. We believe our company has the power to elevate how people work, live and grow.” WeWork S-1, “Our Story” page 1

I’m legitimately asking a question here… Can someone tell me what the *$@# this means? Seriously… I’ve been in this business for 23 years and have never witnessed this level of B.S.

I’ll admit – the first 13 pages of this 300+page document paints a beautiful picture for investors. Vision, growth, technology, community, beautiful spaces; it checks all the boxes and has all the buzz words that would excite any investor. I get it – I understand the allure; but!!! If you keep reading, juuuusssst a little further… like to page 14 “Recent Developments” or 15 “Risk Factors” – make it to 21, just make it to page 21…

For those of you who haven’t heard me rant about WeWork in the past or know who they are, WeWork leases large blocks of real estate, beautifully renovates the spaces with a retro feel, then sub-leases the space out to multiple lessees in smaller chunks. You wouldn’t know this by reading the beginning of the S-1 document recently filed ahead of the company’s lofty Initial Public Offering (IPO).

Ahhh – WeWork. We’ve previously written about their “adjusted, adjusted, adjusted” EBITDA (better known as “community adjusted EBITDA”). We’ve discussed CEO, Adam Neumann touting the “Tech-Like” nature of his company. Neumann lauds himself as a pretty deep thinker as he’s gone on record as saying:

“To Assess WeWork by conventional metrics is to miss the point. WeWork isn’t a real estate company. It’s a state of consciousness.”

Folks, you can’t make this stuff up… This pseudo multi-billion-dollar real estate leasing company is described by their CEO as “a state of consciences”?

Again, if you solely read the beginning of this prospectus, you’d think this company is the next Microsoft, Amazon or Apple… More from the prospectus as they tout their “Attractive Economics”:

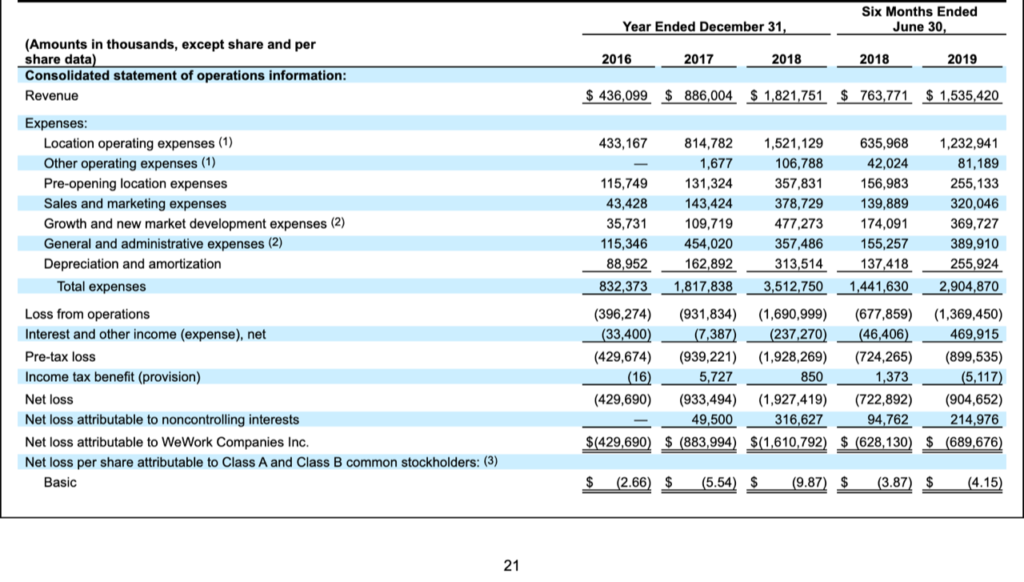

“As of June 30, 2019, our run-rate revenue was $3.3 billion, representing 86% year-over-year growth, and our committed revenue backlog was $4.0 billion, approximately eight times our committed revenue backlog as of December 31, 2017” WeWork S-1 “Attractive Economics” page 14

In May we wrote about the pervasive and dangerous Extend & Pretend mentality of both traditional, and investment banks. We detailed Tesla’s (TSLA) most recent capital raise; WeWork, my friends, is the quintessential poster child of this sickness that permeates our society.

Marketed as a multi-billion-dollar technology, growth, “WE”, state of consciousness company, their long-term lease obligations per the prospectus sit at $47.2-billion dollars as of June 30,2019 (S-1, page 117), while their committed revenue backlog as of December 31, 2017 was $4 billion. Does this sound sustainable to you?

The firm boasts memberships have doubled every year since 2014. They highlight their success in “scaling” the business – here’s the thing about scaling a business. When you grow or “scale” your business, the “exponential” revenue growth should offset your expenses and LOSSES.

WeWork has definitely grown rapidly, and so have their loses as they seem to be growing in proportion. Per the prospectus, the first half of 2019 brought in roughly $1.5 billion of Revenue with over $2.9 billion of expenses – and as stated above, with nearly $700 million in losses through June 30, 2019. ($689,676) is in millions… That’s what just under $700 million in losses in the first half of this year alone looks like folks! PAGE 21

WeWork’s average lease term is 15-years in duration, while the average lessee’s agreement is 15-months; so, while WeWork is locked into a long-term lease – their clients ARE NOT. They are losing money at an unprecedented rate in an economy which is supposed to be strong.

If WeWork was a human, their jugular vein has been hemorrhaging for years; still, investment bankers initially attempted to value this pig at $47 billion – then slashed it to between $20-30 billion, lord only knows what valuation it will fetch in the end, yet one thing I do know… Without a capital infusion of sorts (public or private), they will be bankrupt soon. If the deal doesn’t get done, and we go over our final edits, it looks like the deal will be pushed (temporarily shelved). Our bet would be WeWork’s largest investor, Softbank, ponies up in an effort to “protect their investment” – hell, Softbank has pulled a few rabbits out of their hat before being a large shareholder in debt ridden Sprint, but this one… Wow… I don’t care if you like their office space, if you think it’s pretty, if you like the free beer – STAY AWAY…

This, my friends, is what I mean by lighting money on fire… Their office space is pretty for a reason, but at some point, bills need to be paid.

In a similar vein to Tesla – the cars or office space can be beautiful, the technology can be brilliant, but at some point, a company needs to make more then they spend…

This Extend & Pretend culture solely exists when credit is abundant and free.

If you could imagine, WeWork “shares” many of the same investment bankers as Tesla (5 of 8 – if you could only see the surprised look on my face as I read the prospectus).

Turning in his Grave

“Those with a responsibility to invest money for others should act with prudence, discretion, intelligence in regard for the safety of capital as well as for income”

The words of Justice Samuel Putnam of the Supreme Judicial Court of Massachusetts, in 1830. At a time where Clipper ship captains hired trustees to manage their money while away at sea, the responsibilities and actions of said trustees were brought into question in the landmark case of Harvard College Vs. Armory.

When John Mclean died on October 23, 1823, his will made sure his wife Ann would be comfortable for life. She received their home, specified personal property and $35,000. $50,000 was then bequeathed to a trust, the trustees – Jonathan and Frances Armory:

“to loan the same upon ample and sufficient security, or to invest the same in safe and productive stock, either in public funds, bank shares or other stock, according to their best judgement and discretion”…“the profits and income thereof to be received and collected by said trustees and paid over to my wife, Ann McLean in quarterly or semiannual payment for the duration of her natural life.” reference, Octavious Pickering pg.447

Ultimately, Mr. McLean set up a lifetime annuity for his wife Ann; upon her passing, the trustees would pay over half of the entire trust fund to the President and Fellows of Harvard College, the other half to the Trustees of the Massachusetts General Hospital.

The issue: Harvard, as a FUTURE BENEFICIARY, took issue with how the trustees handled the money (while Ms. McLean was still alive no less)!

The intricacies of the case are beyond the scope of this note – the findings of Justice Samuel Putnam back in the 1830’s, however, are extremely relevant to this day. His words have become the foundation of what we all know as “The Prudent Man Rule” – the gold standard for responsible money management.

In the words of Octavius Pickering, Counselor at Law, Reports of Cases Argued and Determined in the Supreme Judicial Court of Massachusetts, 1831 – pg. 461

“To observe how men of prudence, discretion and intelligence manage their own affairs, not in regard to speculation, but in regard to the permanent disposition of their funds, considering the probable income, as well as the probable safety of the capital to be invested.”

These are the words which have defined the responsibilities and actions of fiduciaries for nearly two centuries. This case set the precedence and bound investment professionals to act with prudence (sadly a court case was necessary to define this). Our firm was founded on these beliefs, they are the core of Theodore Hesburgh’s words that have been with me for over 23 years.

“My basic principle is that you don’t make decisions because they are easy; you don’t make them because they are cheap; you don’t make them because they are popular; you make them because they are right”~ Reverend Theodore M. Hesburgh, C.S.C. President Emeritus, University Of Notre Dame

As of market close today, the DJIA, Nasdaq and S&P 500 sit fractions away from their all-time highs while the Russell 2000 is down roughly 10%. In the same breath, we remind investors this comes at the hand of the Federal Reserve having recently decreased interest rates in July from 2.25-2.5% to the now 2.00-2.25% range. We warned this was coming well over a year ago when the Fed was still increasing rates; we detailed the untold, under reported on “why” in our 4Q2018 note. (among others)

Currently, expectations amongst economists per a recent Bloomberg survey suggests the FOMC will reduce their benchmark Fed Funds rate twice more in 2019; another 0.25 basis-points tomorrow followed by a 0.25 basis-point reduction in December. The justification of these reductions come in the name of “cross-currents” i.e. “a global economic slowdown”.

In our most recently quarterly published in July, we told you negative interest rates will be making their way to the United States (you can read that note here). Ironically enough, we provided you with an example of absurdity with Ford borrowing money denominated in Euros cheaper than the US government could borrow at the time. The irony, as we’ll discuss below, is Ford (F), recently had its debt downgraded to JUNK by ratings agency Moody’s (more on this in my next quarterly).

In last month’s issue, we took a look at historic volatility along with judging the quality of our decisions vs. outcomes of those decisions. We noted markets have delivered 10-20% declines when the S&P 500 has had a daily decline of 3% (or greater) nearly 85% of the time over the last decade. Admittedly, 3 whole weeks have passed, and the selloff has yet to occur.

Anticipating where markets will go is a never ending, thought-provoking mental poker game and for the most part, we’ve played our hand well, anticipating things fairly accurately; well before most “experts” (Feel free to read our archives here). We are in the process of archiving OSAM notes written prior to the launching of our website, yet there are still volumes of pages which can be accessed.

There is not a single individual who knows how far markets will run or the exact date of their inevitable collapse. What we hope to accomplish with these notes is to provide investors with an education on how to let your winners run, cut losers before they become problematic; while recognizing major market shifts, at the same time, ignoring headline noise.

Over the years, we have detailed our thoughts, provided data, historical references, and most importantly, from the onset of running discretionary money, just as Justice Samuel Putnam did, we have and will continue to preach prudence and discipline.

Given the current economic landscape, both domestically as well as globally, we have consistently described our view of financial markets as “cautiously optimistic”. We continue to believe in the market “melt up” thesis, as we wrote in our 1Q2019 note (The Conundrum) that based upon the Fed’s actions, a melt-up is even more likely now than ever before. However, in understanding melt-ups, we are well aware of the aftermath also.

Again, from the onset of running discretionary money in 2016, the majority of our portfolio has been and continues to be long equities. Unapologetically and without shame, since our inception, we have recommended holding cash, gold, silver & precious metals (prudence). We’ve held these positions in our years of outperformance and more recently, we’ve suggested investors hold more of the aforementioned adding the thought of short exposure to our allocation mix, AS HEDGES.

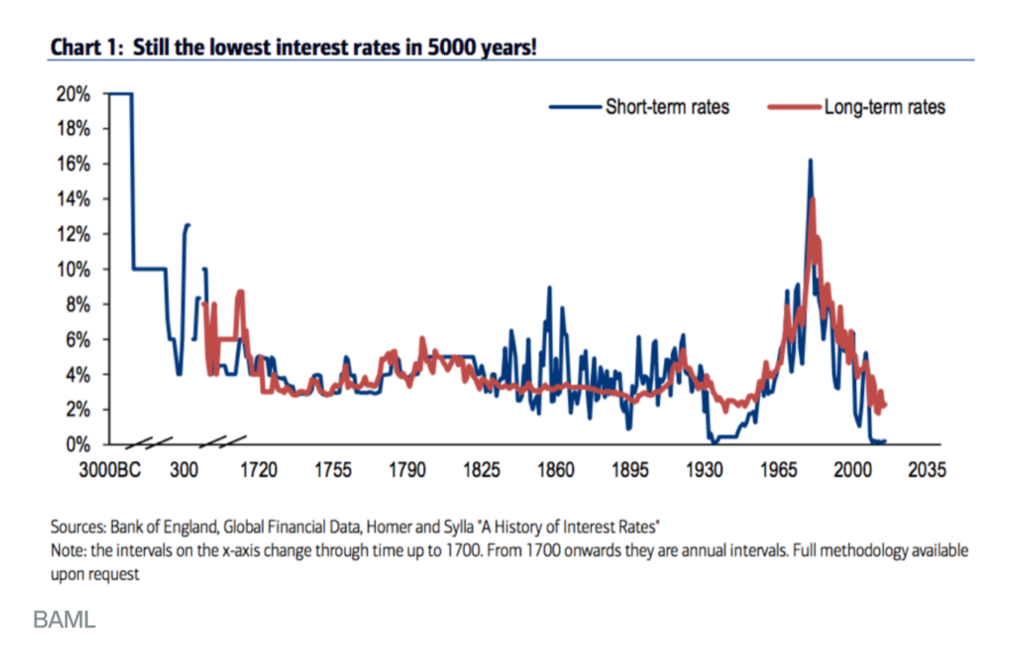

One would think every “Prudent Man” managing financial assets at this time would be obligated to do so; a modest hedge as we, every individual with a heartbeat (investor or not) are first hand witnesses of an event never seen before in 5,000 years of recorded financial history.

We’re talking about Negative Interest Rates…

Chasing Unicorns

Never in the 5,000 years of recorded financial history have we witnessed negative interest rates let alone $17-TRILLION dollars’ worth, globally. Financial news network talking heads to PhD economists and global central bank leaders speak confidently about the impact of negative rates and MMT (Modern Monetary Theory) in an effort to ease the minds of investors, lauding it as a savior (because they’ve seen it before???!).

We argue the prudence of large investment banks bringing over leveraged, cash guzzling companies public with no visible positive earnings stream in sight. We believe there is a lack of prudence in conventional asset allocation models sold to investors by Wall Street; a dangerous complacency or malaise surrounding how they are marketed as we stare at, what can only be described as a Unicorn, dead in the face. A unicorn, a fable never seen before; until recently, that was the prevailing thought surrounding negative interest rates.

10 years of ZIRP (Zero Interest Rate Policy) has fostered malinvestment, expanding a debt fueled credit bubble, creating zombie companies which can only function with the ability to borrow more money at near zero interest rates; failing to produce a stable economy as corporate revenues and earnings are slowing at a more rapid rate quarter over quarter. So, if zero interest hasn’t worked, negative rates are sure to do the trick, right?! SMH… It’s akin to building the Great Wall of China on an enormous pile of loose sand, the structure won’t hold sitting atop a foundation with no stability.

What economists, bankers or politicians who support MMT & negative rates have failed to mention is how negative interest rates will affect a “Fractional Reserve Banking System” – For those of you who don’t know what that phrase means, it’s the financial system in which we operate in today. To overly simplify, assume you give your bank $100, they keep $10 in reserve on the books and then proceed to lend out $90. Under normal circumstances, when a bank leverages their balance sheet maintaining a mere 10% in deposit reserves, lending out roughly 90% of their balance sheet, they currently earn positive returns on the newly created money as interest compounds on top of interest. Historically, this has been positive for banks…

Now ask yourself a simple question – what happens when rates go negative and yield curves are flat to inverted for an extended period of time?

It doesn’t take a genius to see where this one’s going… Let’s just take a walk around old school, bellwether European financial behemoths.

We’ll start in Spain with Banco Sabadell:

How about Banco Santander?

Societe Generale?

You might be saying, but Mitch, I’ve never heard of these institutions… Alright, what if we looked at Credit Suisse? Surely, you’ve heard of them…

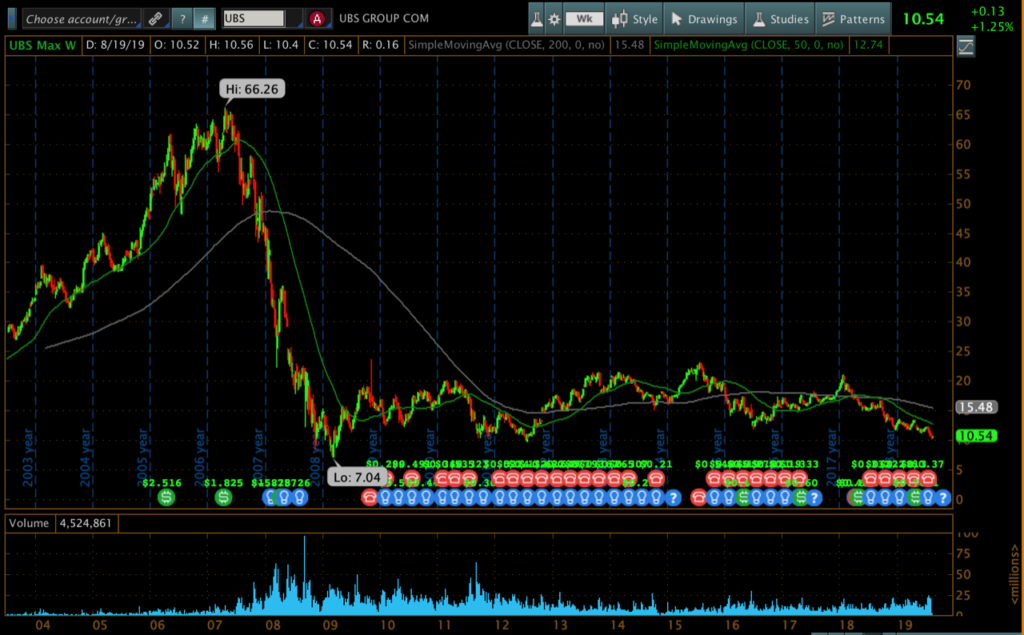

UBS? The Union Bank of Switzerland… The multinational diversified financial investment bank that had bought Paine Webber so many years ago…

The pride of Germany… Deutsche Bank:

We could keep going… Some will argue how much more “well capitalized” our banking system is. Though in a recent interview with RealVision, Thomas Mayer, founder and managing director of the Flossbach von Storch Research Institute believes (and I’m paraphrasing) a combination of weaker growth (relative to the US), a fragmented banking system, years of a FLAT yield curve when combined with NEGATIVE INTEREST RATES collectively attribute to the difference and all adversely affect book value.

We argue weaker growth is more a symptom of a flat or inverted yield curve, which we now see here in the US. With little to no margins, banks pull back on business activity. I personally know business owners whose banks are already scrutinizing revolving credit facilities. Our president is tweeting for negative interest rates and the FOMC is currently in an easing cycle.

If 2008/2009 taught us anything about financials, it should be book value means very little when the underlying assets on their books are illiquid; their value can drop faster than terminal velocity in times of a credit crisis.

I’d be curious as to what real estate companies’ assets are WeWork’s liabilities?!

While many may not know who Mayer is, his career has been with Goldman Sachs, the IMF as well as chief economist at Deutsche Bank – he’s no dummy. Mayer’s final thoughts of the interview assuming the ECB continues with their current policy: Mayer describes the ramifications as “a Tsunami which you can see coming”. If this happens, he sees a “banking crisis combined with a sovereign debt crisis”, finally, “unfortunately, I see no easy or orderly way out of it…”

There are always warning signs

We’ve often referenced the book “This Time it’s Different: Eight Centuries of Financial Folly” by Carmen M. Reinhard & Kenneth S. Rogoff. While impossible to sum up the body of their work in a mere paragraph, loss of confidence seems to be the determining factor in what drives a crash, there is no one tangible indicator or ratio that sends markets into a death spiral. Though, we’ve noted in most cases, there are warning signs along the way.

We have detailed many of flashing yellows over the past few years but have also stated that caution is warranted the larger the event and more frequent the occurrence.

- The aforementioned WeWork IPO and the scandals surrounding their CEO is a sign we’re nearing a top

- The last few “Billion-dollar” Tech IPOs, all of whom are losing money – most now trading below their IPO prices are a sign of a top (SNAP, DBX, PVTL, UBER, LYFT, SPOT, PINS, CLDR)

- An abrupt change in Fed monetary policy (Hawkish to Dovish) is a sign of a top (doesn’t get larger)

- $17 trillion dollars in negative yielding global debt

- Negative mortgages being issued in Denmark

- GAM Investment gates funds in mid 2018 due to liquidity issues

- All Star European manager Neil Woodford freezes redemptions in June 2019

- H2O Asset Management backed by Natixis suspends redemptions (again – liquidity)

- General Electric (GE) recently being called a bigger fraud then Enron by the Bernie Madoff Whistle Blower (where are the credit ratings agencies?)

- The fall of Ford (F) as Moody’s just downgraded their debt to Junk (at what point will the other ratings agencies?) – I seem to remember writing about Ford 2-3 years ago

Independently, these would be considered “anomalies”, yet collectively they add up to much more. liquidity issues, alleged fraud, American icons turning to junk, FOMC easing cycle, in what people are calling a strong economy?!

Do you really believe it’s time to put your foot firmly on the proverbial gas and be fully invested? Do you really think a typical mutual fund or ETF model will protect you when the bottom falls out? We will continue to ask this question, our clients know what they are doing differently, but for those sitting on the fence or yet to be clients, what are you doing differently today then you were in 2001/2002 or 2008/2009 when markets decimated most investors?