In This Article

History Is Speaking to Us … Again

If we want to draw benefits from history, the goal is to capture its most important lessons.

Many investors point to giants like Buffett, Druckenmiller, Zweig, Dalio, Lacey Hunt, Howard Marks and so on… but few take their advice. None of these legends are infallible and each has made mistakes, but when there is agreement among many of them, the prudent observer of history takes notice.

In our 3Q2018 note we wrote:

I grew up in the school of football. … The biggest, fastest, strongest team isn’t always the team that wins. It’s often the most disciplined team who can outthink and adjust quickly on their feet. Lombardi, Parcells, Belichick, Ditka didn’t game plan their Super bowls as they did the first game of the season. They would extensively study film on every player that could possibly be on the field. They knew the capabilities, strengths and weaknesses of both the opposing team as well as their own. They studied the sidelines, hand signals, weight disbursement of an offensive lineman, how much pressure a lineman placed on his knuckles, was a “tell” for whether he was going to explode off the ball (run block) or kick slide into a pass block. They studied every single possible angle looking to exploit a weakness or gain an edge somewhere, somehow…

The prudent investor must study the field with equal diligence.

Dr. Lacy Hunt of Hoisington Capital, one of the most accurate economists over a span of decades, is a student of economic history. As he relates in a recent interview on Real Vision’s MacroVoices:

“Ironically, there have been some pretty smart minds over the years that have looked at the indebtedness problem. One of the first was by the great David Hume writing in 1752” …

Hunt continues…

“My professor, Ingrid Rama said that the Enlightenment could not have occurred without David Hume. Adam Smith, who was mentored by Hume, said that he was the greatest intellect of the age. And Smith knew Voltaire. He knew Ben Franklin. And Hume was the greatest.

In 1752, Hume wrote a paper [called “Of Public Credit”] which I recommend you read. You can get it on the internet easily. It’s only about 20 pages. It’s not in modern English, but it’s very understandable.

And he looks at these cases that were available up until the time of 1752. He looks at Mesopotamia and Rome and a number of lesser cases that have long been forgotten.

And this is what he says. He says when a state has mortgaged all of its future revenues, the state by necessity lapses into tranquility, languor, and impotence. And today, we know that it triggers diminishing returns and an insufficiency of saving to generate physical investment.”

We agree with Dr. Hunt that Hume’s Of Public Credit is not easy reading, but without question it is VERY understandable.

Hume’s observations and conclusions suggest that today’s Central Bankers show hubris more than wisdom. The Federal Reserve officials seem to have learned nothing through the lens of history and have chosen to ignore centuries of lessons.

To paraphrase Hume (saving you some of Ye Olde English):

It appears to have been the common practice of antiquity, to make provision, during peace, for the necessities of war, and to hoard up treasures before-hand, as the instruments either of conquest or defence; without trusting to extraordinary impositions, much less to borrowing, in times of disorder and confusion. Besides the immense sums above mentioned,1 which were amassed by Athens, and by the Ptolemies, and other successors of Alexander; we learn from Plato,2 that the frugal Lacedemonians had also collected [350] a great treasure; and Arrian3 and Plutarch4 take notice of the riches which Alexander got possession of on the conquest of Susa and Ecbatana, and which were reserved, some of them, from the time of Cyrus. If I remember right, the scripture also mentions the treasure of Hezekiah and the Jewish princes;5 as profane history does that of Philip and Perseus, kings of Macedon. The ancient republics of Gaul had commonly large sums in reserve.6 Every one knows the treasure seized in Rome by Julius Cæsar, during the civil wars:7and we find afterwards, that the wiser emperors, Augustus, Tiberius, Vespasian, Severus, &c. always discovered the prudent foresight, of saving great sums against any public exigency.

On the contrary, our modern expedient, which has become very general, is to mortgage the public revenues, and to trust that posterity will pay off the incumbrances contracted by their ancestors. … To trust to chances and temporary expedients, is, indeed, what the necessity of human affairs frequently renders unavoidable; but whoever voluntarily depend on such resources, have not necessity, but their own folly, to accuse for their misfortunes, when any such befall them.8

If the abuses of treasures be dangerous, either by engaging the state in rash enterprises, or making it neglect military discipline, in confidence of its riches; the abuses of mortgaging are more certain and inevitable; poverty, impotence, and subjection to foreign powers.

We have ALWAYS found, where a government has mortgaged all its revenues, that it necessarily sinks into a state of languor, inactivity, and impotence.

1752 … Nearly 270 years ago; Hume, one of the greatest thinkers in history, educates those willing to learn that SAVINGS trumps DEBT, citing a number of dynasties that had been built or toppled based upon, respectively, “prudent foresight” or “mortgaging all its revenues” … and that abuses of mortgaging will inevitably bring “poverty, impotence and subjection to foreign powers”.

Leaving us to wonder if President John Adams had Hume in mind when he stated in 1826:

“There are two ways to conquer and enslave a nation. One is by the sword. The other is by debt.”

Back to the Present

So, what’s the history that we’re making now?

Whether we like it or not, current economic data suggests that either a Depression or a deep Recession lays before us. While some suggest “reflation”, we don’t believe a minor uptick in data supports a V-recovery, nor the bounce of U.S. equity prices to a level slightly below the already egregious highs of February 19th. All valuation metrics pushed their extremes in February, and it is really difficult to imagine fundamentals that support revisiting those levels.

Let’s look at the DATA – and attempt to unpack this in an orderly fashion:

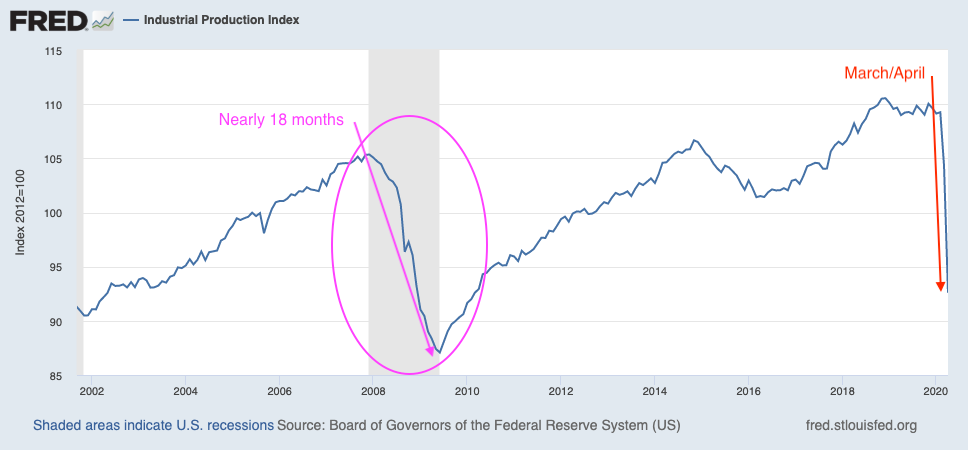

Start with Industrial Production, which fell 11.2% in the month of April, “its largest monthly drop in the 101-year history of the index”. This eclipsed the previous record decline of -10.4% in August of 1945 (largest in HISTORY … seems like it could be bad?!), and it roughly matches in one month the losses of the entire 18 month decline during the GFC.

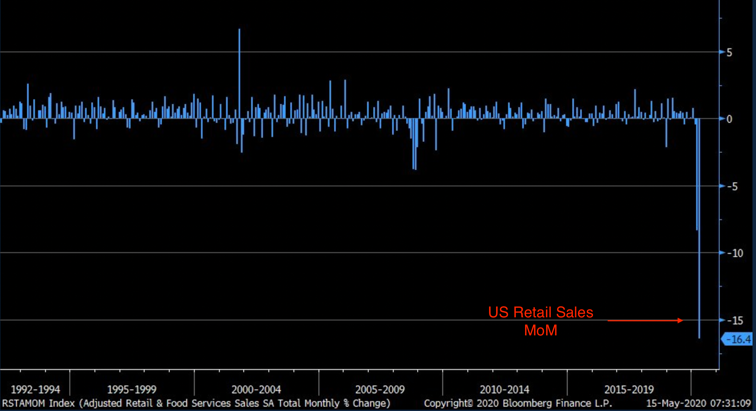

At the same time April Retail Sales fell -16.4% (again, largest in HISTORY) vs Wall Street estimate of negative -12% (The more you read our notes, are you beginning to see a common theme with Wall Street estimates and consensus being perpetually WRONG?!)

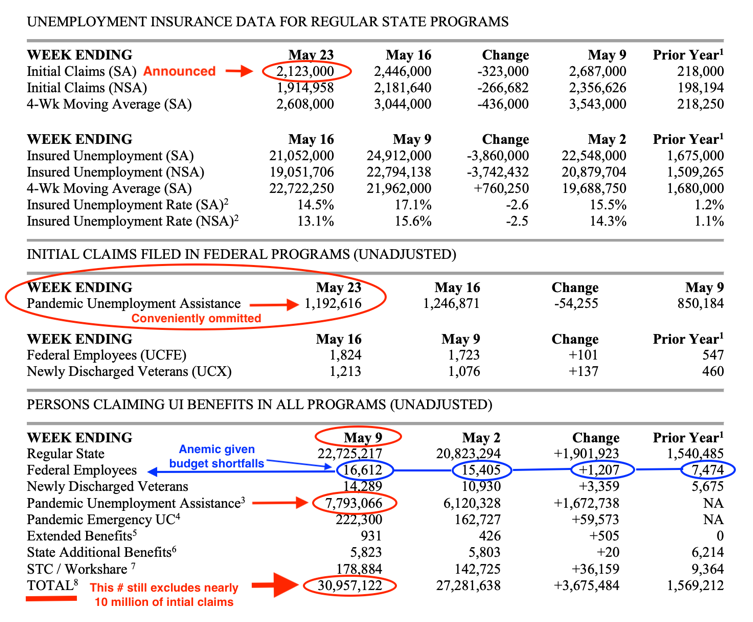

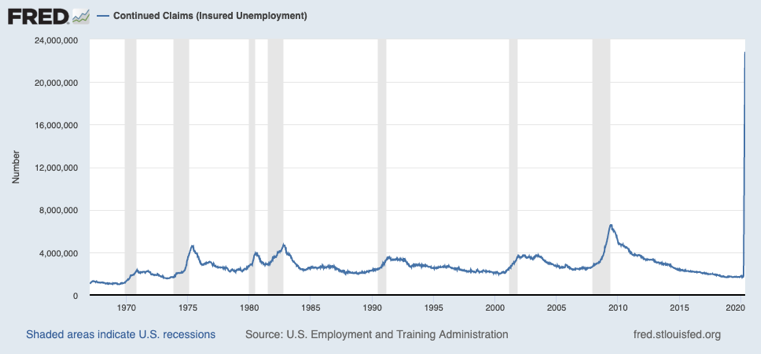

Meanwhile, we’ve just recorded nearly 31 million continuing unemployment claims, including the new PUA (Pandemic Unemployment Assistance) for people who are not eligible for regular state unemployment (eg: self-employed and independent contractors). You can find the full DOL report here.

The headline number Wall Street/Financial media reported was 21 million … a miracle WoW decrease. As reported by CNBC, “Jobless Claims total 2.4 million, still elevated levels, but a declining pace from previous weeks”. You are being grossly misled, by nearly 10 million unemployed, which is why we constantly urge you to read the fine print.

Meanwhile nearly 40.8 million people have reported initial jobless claims over a similar time frame. In the blink of an eye, all of the job gains of the last decade have been erased… (again, the largest losses in HISTORY)

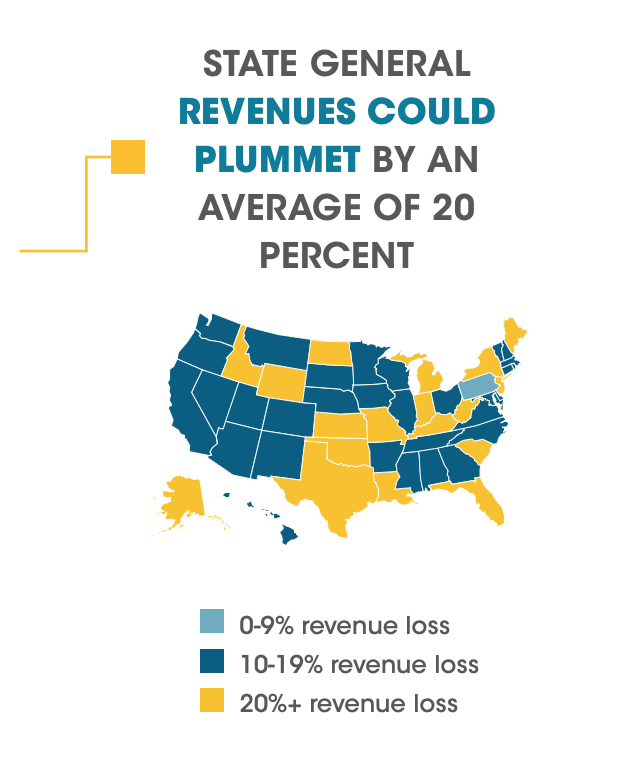

As tax receipts shrink, so too do the revenues of government at all levels and while the federal government relies on its printing press to fund its unsustainable budget deficits, the debt of states and municipalities still needs to be serviced and doesn’t share the same luxuries. UBS sees the Muni-bond market facing it’s “biggest storm in modern history”. Why? As we’ve discussed for years, tremendous sums of debt coupled with budget shortfalls, which must be met with a cut in spending. Budget shortfalls = more job losses to hit the public sector. States can’t operate with shortfalls like this, Moody’s estimates New York at -34%, New Jersey at -35%, California at -19% (see all stated by clicking here).

Are the states and municipalities reaching the stage of “impotence” described by Hume, or being “enslaved … by debt” per John Adams?

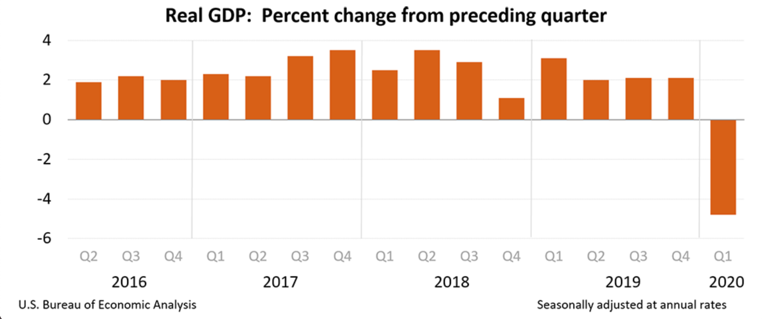

This has all lead the economy to a Q1 contraction of negative -4.8%, the largest GDP decline since the GFC (Great Financial Crisis), which saw GDP fall by -8.4% in 4Q2008…

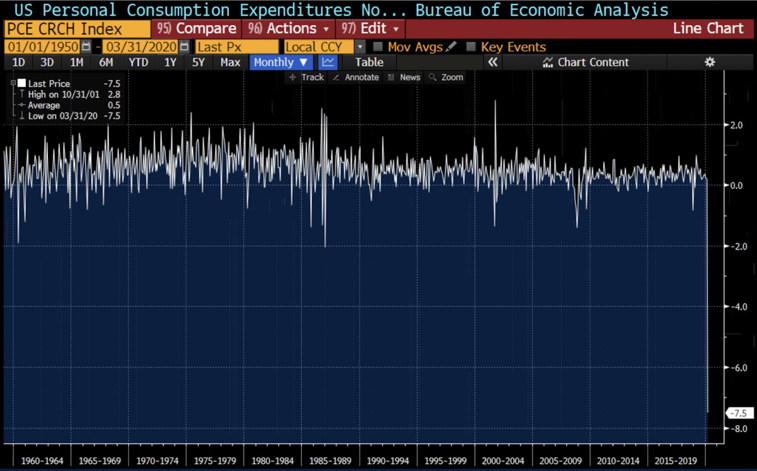

As personal consumption fell off a cliff… (at the risk of sounding repetitious, “the largest decline in HISTORY”)

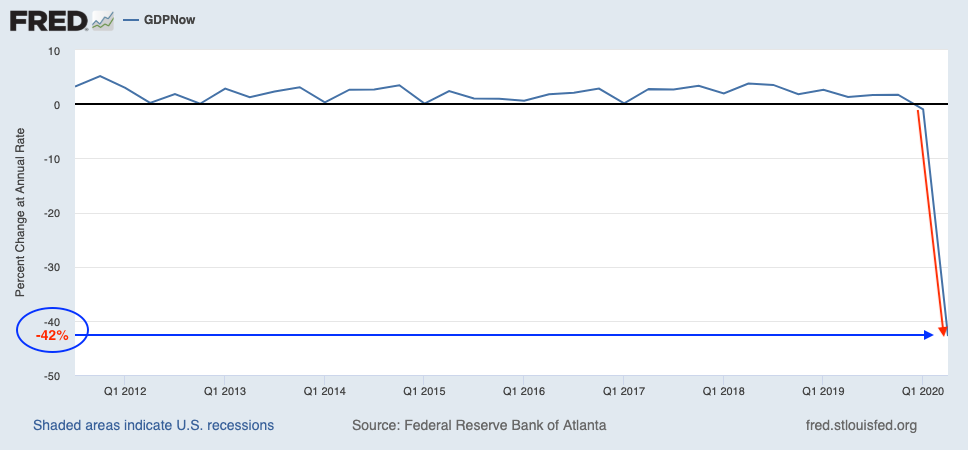

The Atlanta Fed is anticipating a second quarter contraction in GDP of -42.8% (… sigh … the largest decline in HISTORY).

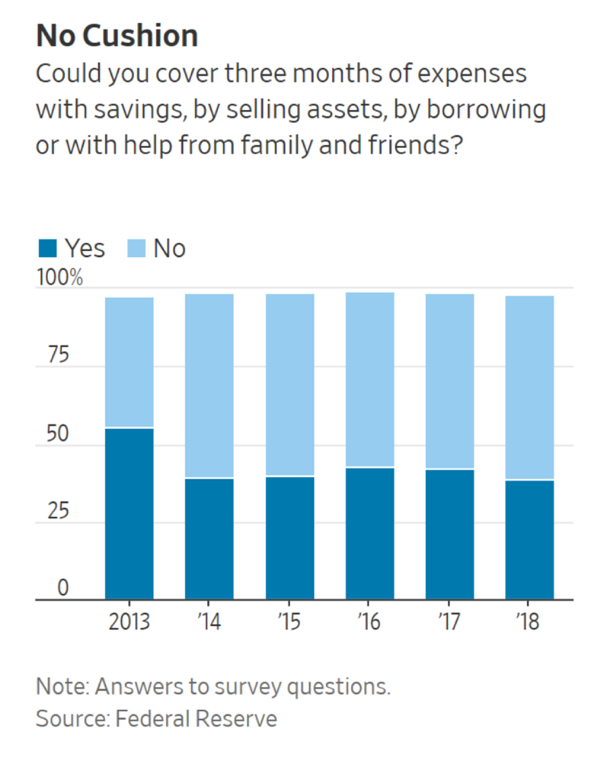

The Fed’s recently released Report on the Economic Well-Being of U.S. Households released on May 14th, suggests, among people who were working in February almost 40% of those in households making less than $40k/yr had lost a job in MARCH! Meanwhile, a Federal Reserve survey and Wall Street Journal report suggests that well over 50% of individuals surveyed could not afford three months of expenses with savings, selling assets or by borrowing…

The Fed’s recently released Report on the Economic Well-Being of U.S. Households released on May 14th, suggests, among people who were working in February almost 40% of those in households making less than $40k/yr had lost a job in MARCH! Meanwhile, a Federal Reserve survey and Wall Street Journal report suggests that well over 50% of individuals surveyed could not afford three months of expenses with savings, selling assets or by borrowing…

The narrative on Wall Street that the consumer is resilient has been shattered!

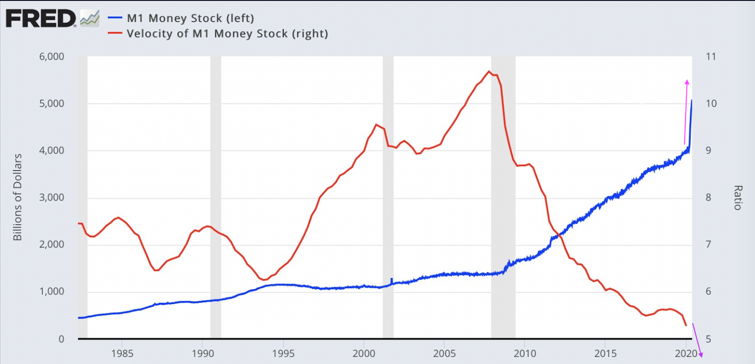

The Fed’s response, and the only tool in their toolbox, continues to be liquidity, as money supply has shot to the moon. Yet the velocity of money, which cannot be controlled by the Fed, continues to decrease … making the increased money supply ineffective (Impotent”?) at stimulating the economy.

The liquidity is promoting asset price inflation (cheers on Wall Street!), but not making it into the hands of those who need it (cries on Main Street!). Conservative estimates are that over 100,000 small business owners that will never open their doors again, while Moody’s estimates that number could balloon to over 1 million as reported by Heather Long of the Washington Post.

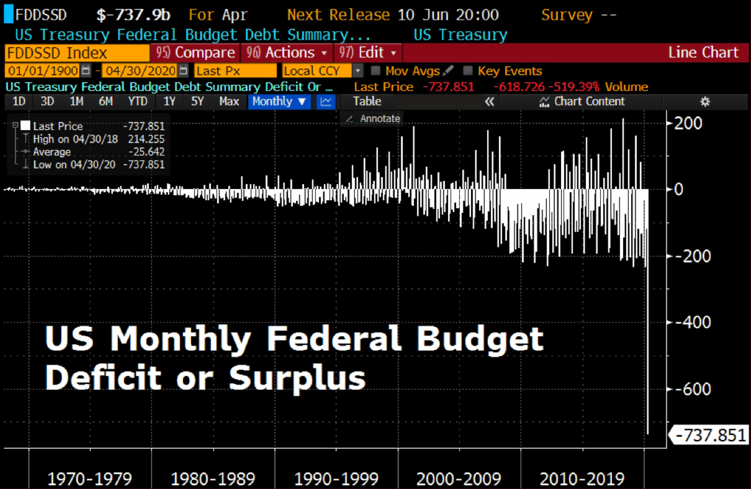

As the Federal Government just spends and spends… April brought a monthly deficit of nearly ¾ of a trillion dollars. … IN ONE MONTH (dare we say it, “largest in HISTORY”).

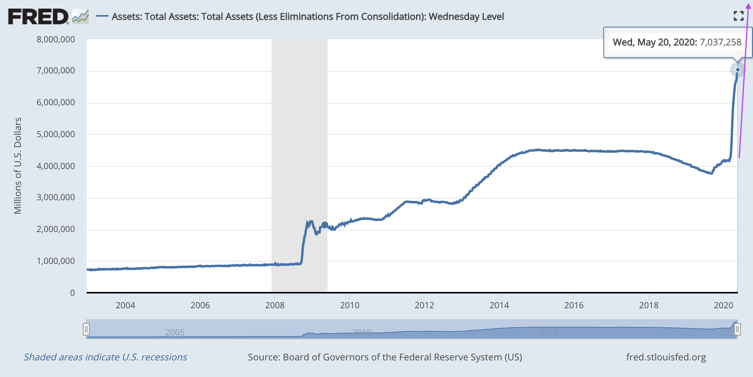

Which is why the Fed’s balance sheet has eclipsed $7 trillion and continues to grow …

And while asset purchases have slowed down, the Fed will need to further increase its balance sheet to support the fiscal spending (and deficits) of the Federal government as shown above.

There are only so many ways to say this…

But, but, but the S&P… While we may very well be witnessing some form of “rebound” in equity prices due to Central Bank liquidity measures, equity market prices have NEVER been more disconnected from fundamentals in the history of Wall Street … and NEVER is a long time…

The bottom line is, our economy has record levels of personal and public debt, and is accumulating more debt at record rates … HISTORIC levels.

The Federal Reserve is attempting to fix a debt and insolvency problem with liquidity and more debt … We will remind you that PRE-virus, Corporate Debt to GDP was the highest it had ever been in HISTORY while staring at the absolute worst credit quality EVER!

In a recent 60 minutes interview Federal Reserve Chairman Powell described it thus:

CBS: Fair to say you simply flooded the system with money?

Powell: Yes. We did. That’s another way to think about it. We did.

CBS: Where does it come from? Do you just print it?

Powell: We print it digitally. So, as a central bank, we have the ability to create money digitally … and that actually increases the money supply.

Flooding the system with money, i.e. “liquidity”, doesn’t solve for “insolvency” … Powell seems to think it does, but some well-respected titans of the industry share our sentiment.

From Giants of the Past to Giants Today

So, where does that leave us today?!

Stanley Druckenmiller, speaking in front of the Economic Club of New York via live stream on May 12, 2020, shared some valuable insight:

“The risk-reward for equities is maybe as bad as I’ve ever seen it in my career here”

Ummmm, yeah, there’s that word again, EVER (over a 40+ year career). And while he did applaud the Fed’s emergency actions in March, he noted they’ve gone too far. His comments below are in reference to an extended period of poor Central Banking policy leading up to March (this should sound familiar to every long-time reader) you can find this excerpt at minute 16:05:

“it’s unbelievable, we went into this – into COVID with $1.4 trillion government deficit with full unemployment, we’ve never seen anything like it. And corporations took their borrowing from $6 to 10 trillion. In my opinion … This was all a result of free money despite many, many chances to normalize from 2012 to 2020.”

We found minute 16:48 to be most poignant:

“I would also say that once we got out of March and into April, I found the $2.3 trillion, where they crossed all kinds of lines, in terms of collateral and stuff we never got near in 2008 somewhat puzzling and aggressive. I could see it if we were still at 2200 (on the S&P) and I could see it if the bond market was shut, I’m talking about the corporate bond market. But it came a week after the MOST AGGRESSIVE BOND MARKET ISSUANCE IN HISTORY and it’s just a little weird to me because in my opinion, the reason they had to do so much was because corporations OVER BORROWED and were OVER LEVERAGED GETTING INTO THIS and those same corporations are now, when we know we’re on the front end of a recession; the answer is to borrow more and … That does not make any sense to me because the Fed is there to solve liquidity problems in open markets … but they are not there, and they are not in any way capable in my opinion of solving solvency problem.”

No mincing words there …

Howard Marks ( Oaktree Capital, specializing in distressed debt investing) understands cash flows and asset values. In a recent Bloomberg interview, Marks noted Oaktree has started “pulling back” since the Fed began its overly aggressive intervention. Marks stated:

“Those of us in the markets believe that stocks and bonds are selling at prices they wouldn’t sell at if the Fed were not the dominant force. So, if the Fed were to recede, we would all take over as buyers, but I don’t think at these levels.” Bloomberg 5/18/2020

Meaning, the Fed is mispricing risk in his world by artificially inflating asset prices. Bloomberg reporter Erik Schatzker noted, “Marks expects “PLENTY” of defaults and bankruptcies when corporate borrowers start running out of cash in the months ahead.”

Marks, without question, understands the difference between Fed liquidity and balance sheet solvency; he also understands … PATIENCE … which we labeled “one of the more valuable ASSET CLASSES moving forward” last month.

Warren Buffett has recently weighed in on this subject as well. Earlier this month, Buffett held a “virtual town hall” in lieu of Berkshire’s annual shareholder meeting. He discussed his thoughts and opinions on today’s current market conditions; subsequent days have also revealed some of his more recent actions.

Key takeaways:

#1 Berkshire sold their holdings in all 4 major airline companies; stating, “the world has changed”:

“I don’t know if two or three years from now if as many people will fly as many passenger miles as they did last year. If the business comes back 70% or 80%, the aircraft doesn’t disappear. You’ve got too many planes.”

#2 Berkshire sold off their stakes in Phillips 66 (energy), Travelers (Insurance), the majority of their stake in Goldman Sachs, while trimming JP Morgan and Synchrony Financial.

#3 (MOST NOTABLE and relatable to Druckenmiller and Marks) Buffett said that he was “starting to get calls” from companies looking for cash; but he, like Marks ran into more unintended consequences of the massive Central Bank stimulus, for those companies, explaining that they:

“were able to get money in the public market frankly at terms we wouldn’t have given to them.”

One of the greatest allocators of capital in history wouldn’t give these companies the TERMS the Federal reserve is providing them.

Equity markets topped out on February 19, 2020 and this was your headline of the day by the FT (Financial Times) “Fed sees ‘more favorable’ US economic outlook” even if they were looking back a few weeks, you literally couldn’t make it up if you tried.

We’ve discussed mispriced risk for some time now. Some of the best capital allocators in HISTORY are now telling you that the Federal Reserve is mispricing risk.

So, to summarize these pages:

David Hume: “when a state has mortgaged all of its future revenues, the state by necessity lapses into tranquility, languor, and impotence”;

Lacy Hunt: “Today, we know that it triggers diminishing returns and an insufficiency of savings to generate physical investment”;

Stanley Druckenmiller: “The risk-reward for equities is maybe as bad as I’ve ever seen it in my career” (mispriced risk);

Howard Marks: “stocks and bonds are selling at prices they wouldn’t sell at if the Fed were not the dominant force” (mispriced risk);

Warren Buffett: the companies calling him “were able to get money in the public market frankly at terms we wouldn’t have given to them” (mispriced risk).

Which brings us to our Final Thoughts…

Embrace the Suck

You may be wondering where this title came from. Recall how winning coaches studied the field and constantly adapted to new realities. ”Embrace the suck” was a phrase we used often on the football field and weight room. Everyone wants to win, but few are willing to put in the HOURS AND WORK REQUIRED to play at an extremely high level. Those who embrace the “misery” that most shy away from, eventually wind up separating themselves from the majority (in a good way). You become the minority by doing what most perceive as difficult but is what’s required if you want to play at a high level and succeed. As is with most things in life, “embracing the suck” becomes a discipline which turns the hard work into routine.

Financial markets aren’t “under stress”; they are structurally damaged. There is a difference between “stress” and a “structural damage”. Over 28 Central Banks around the Globe were cutting rates and had some form of monetary easing policy before COVID-19; which hasn’t solved “the problem”. Japan has pursued aggressive QE since their stock crash in 1990; Japan and Europe have had negative interest rates for years; yet all of those economies are in torpor. Are we supposed to believe that the Fed will have a different result?

Bank credit/debt obligations still need to be serviced and repaid (liquidity doesn’t solve for insolvency) and those who have taken on excessive leverage still need to meet these obligations. Witness the beginning of the oncoming wave of rolling bankruptcies, starting with J Crew, Neiman Marcus, JC Penny, Diamond Offshore, Whiting Petroleum … and now, Hertz.

The bankruptcy formula is simple and repeatable: Sharply reduced revenue = massive $$ shortfall to service debt = default/bankruptcy.

This formula is the same for the individual, too. No income = no ability to make mortgage, car, credit card, student loan payments = default/bankruptcy. Just ask the more than 4.5 million homeowners that are currently in mortgage forbearance … that’s roughly 9% or more than $1 trillion worth of mortgages in forbearance as delinquencies saw their highest increase EVER (yes, largest in HISTORY) in April jumping from 3.4% to 6.5%.

40 million lost jobs — if people are missing mortgage payments, what do you think is happening to consumer credit cards and auto loans? Currently, 15 million credit cards are in forbearance along with 3 million auto loans, representing roughly 3% and 3.5% of all cards and auto loans … and we are at the early stages of this recession/depression. Our wager is that these figures will get substantially worse, as will student loan debt, as unemployment insurance expires, rent/mortgage forbearance expires, and layoffs continue…

The bankruptcy equation holds true for governments as well – local, state & federal … shuttered businesses and personal bankruptcies = decreased tax revenue = budget & pension shortfalls = defaults PLUS layoffs at the government level, which we haven’t seen in the data yet.

Ask yourself this – can the Fed keep us out of a depression while tens of millions are out of work? Maybe? Maybe not… What are the odds?

Can the Fed create an ever-larger asset bubble (on Wall Street) while millions wait in food bank lines (on Main Street)? No one knows when this falls apart as ever more bankruptcies in the corporate and personal space begin to build on each other; as mortgages, credit cards, auto loans move from forbearance into default.

While the Fed’s liquidity may produce short term asset reflation (our current equity bounce), centuries of history confirms their solution of borrowing money (taking on more debt), to hand out to both businesses and individuals, will NOT promote growth and will end very poorly.

As Dr. Lacy Hunt reminds us:

“Remember, debt is an increase in current spending in exchange for a decline in future spending, unless you generate an income stream to repay the principal and interest. And we’re borrowing astronomical sums.

But the funds are going to maintain daily living needs of people to put food on the table, pay their rent. A humane activity, politically popular. But it will not generate an income stream to repay principal and interest.”

This last point, of borrowing beyond the means to generate income that will repay principal and interest, is what economist Hyman Minsky refers to as Ponzi financing. You may remember Minsky from the term “the Minsky Moment” that touched public awareness in September 2008.

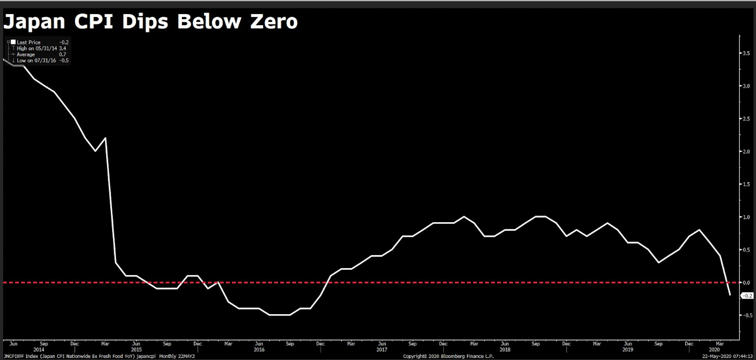

As we mentioned in last month’s note, Japan’s failed Central Banking policy of the last 30 years reminds us of who’s been right or wrong with their economic calls. It just so happened as we were finishing up this note, Bloomberg financial news journalist Tracy Alloway reminded us yet again as Japan’s CPI just fell below zero, AGAIN.

It is also a point of caution to note as we did last month, that Japan’s stock index, the Nikkei 225, touched 39,000 in 1990, just before their crash. It has never seen that level again.

Maybe the Fed will have better luck with its QE strategy?! Or maybe it’s wisest to avoid broad indices as an investment tool.

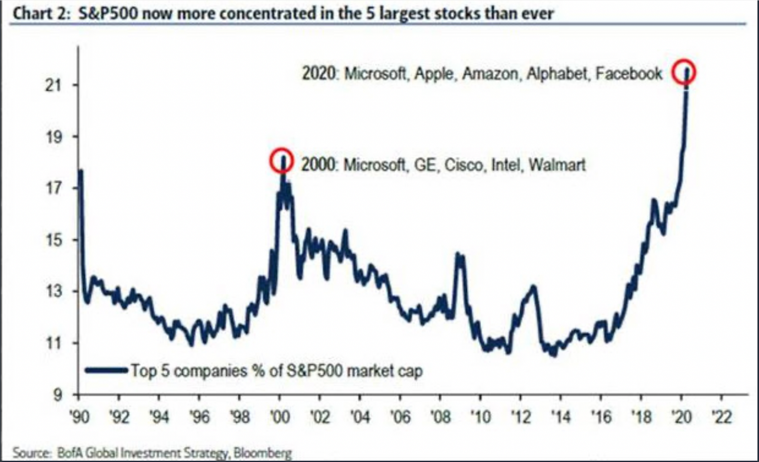

For those people who continue to measure “market return” vs. the benchmark index of the S&P we would urge significant caution. As a cap weighted index in an ETF/passive world, the construction of the S&P no longer provides a viable proxy or barometer of the “broader” economy or “value” as 5 companies now represent just over 23% of the index.

Asset prices may move higher, but if the tapering of 2017/18, history and economics have taught us anything, we will never be able to normalize without some serious pain. Overinflated bubbles always pop, and concentration risk is very real!

When 23% of the S&P is 5 companies…

When 42% of the XLK is 2 companies…

When 50% of the QQQ is 6 companies…

There are some very important questions everyone should be asking:

- What are the most probable outcomes, given the current economic data?

- What are the global equity, currency, commodity & bond markets telling you, that US equity markets are ignoring?

- Can we capture upside while protecting our downside and if so, how?

Which leaves us with our highest conviction trades. Our highest conviction trades don’t fall within some marketing ploy 60/40 portfolio split, but when push came to shove and markets have been smoked, our capital preservation strategies and allocation have kept clients sleeping soundly at night. We’re still in the early innings of this. The S&P 500 could very well hit all-time highs, artificially supported by unsustainable liquidity provided by the Fed. But, make no mistake … it is unsustainable, there are ramifications to what the both the Federal government and Federal Reserve are doing.

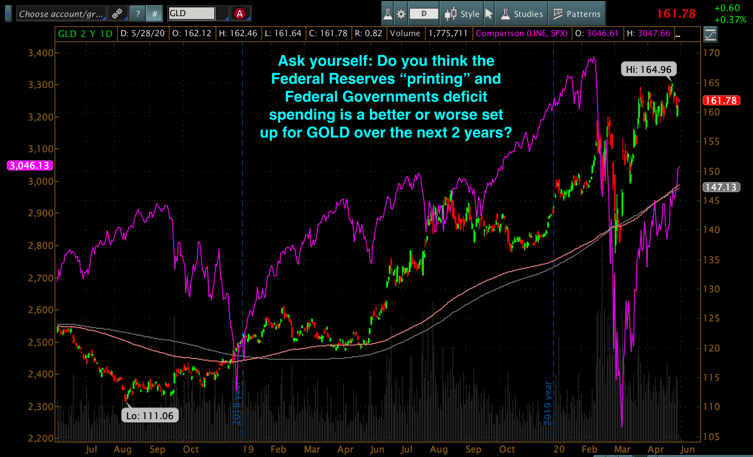

- Gold (and gold stocks) – Gold will benefit from both sides of the Fed actions: if the Fed attempts to normalize and markets correct, it becomes the safe haven trade; or, if the Fed continues to print, gold becomes the sound money trade.

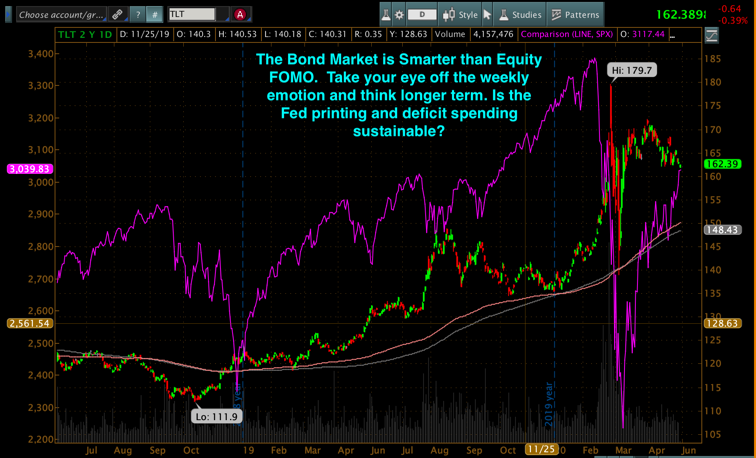

- Treasuries – interest rates will most likely go negative regardless of what Federal Reserve officials tell you. Given a Negative GDP print and positive 10-year, real rates will be like a noose around company’s necks. Treasury yields will have to be capped in some shape or form given the increase in debt service ratios.

But, while yields on government debt may remain low (and bond values high) for some time, rates on corporate debt will likely increase, causing corporate bonds to decline in value.

- The US dollar – yeah, not what most were expecting, but given the copious amounts of EM (Emerging Market) debt denominated in USD, and the current shortage of the currency, it is highly likely there will be an increasing demand for dollars. As EM currencies get obliterated, it takes more of their currency to buy more USD, creating a vicious cycle – sell their currency for more USD pushed the $$ higher and their currency even lower. This will continue to wreak havoc in EM for some time … (until it doesn’t, but we believe there’s a loooong way to go before this ship rights itself).

- US equity – (very selective minority) focusing on those companies which have the ability to benefit from the Fed’s actions (MAINTAINING CAPITAL PRESERVATION STRATEGIES ON EVERYTHING WE OWN). As discussed above, avoid exposure to broad indices. They don’t perform well with high concentration levels in a bear market.

As investors we all have a choice; we can ‘embrace the suck’, allowing us to sleep at night knowing the hard work has been done as we sit atop copious amounts of data and have CENTURIES of HISTORY on our side…

OR

We can get trapped into a FOMO trade and fall through a trap door as most investors did in February … your choice!

We will continue to mention, whether you know it or not, times like NOW are the reason you have hired us or consider doing so… As always, we’re happy to discuss our market thoughts, never hesitate to reach out with any questions or concerns.

Thank you for your continued trust and support!

Sincerely,

Mitchel C. Krause

Managing Principal & CCO

4141 Banks Stone Dr.

Raleigh, NC. 27603

phone: 919-249-9650

toll free: 844-300-7344

mitchel.krause@othersideam.com

Please click here for all disclosures.