In This Article

Mad World

As you read this, the world is in the midst of unprecedented change.

Not just here in the United States … this change will be large scale and global (and we’re not just speaking financial markets). For us to suggest we have all the answers as to what our future looks like would be foolish, though to make the assumption that things will go back to business as usual upon a government “quarantine” being lifted, in our humble opinion, is obtuse, linear thinking.

We place a high probability on the thought that everything from how we educate our children, communicate, manufacture, source supply chains, manage our finances and so on will be affected in some way shape or form. We would even go so far as to believe our civil liberties as we know them are in jeopardy of change?! Some would argue quarantine of an entire society based upon an adverse event rate of 1% from a virus may in fact be an outrageous overstep?! This note is not the proper medium for this specific discussion, though the fact remains… life, as we know it, is changing before our eyes.

Some attribute the below quote to Rahm Emanuel while others suggest he paraphrased Churchill:

“You never want a serious crisis to go to waste. And what I mean by that is an opportunity to do things that you think you could not do before.”

And boy… The powers that be are surely not wasting this “crisis”.

Writing this note has proven challenging. In many instances, we’d written entire sections that went obsolete over the course of a few days due to how quickly the Federal Reserve keeps moving the goal posts… Recent days have felt like weeks, weeks like months and March felt like an eternity … and we’ve merely closed out the first quarter of 2020 (1Q2020).

As quickly as things have been moving, TIME and PATIENCE will be one of the more valuable ASSET CLASSES moving forward (in our humble opinion). Recognizing and understanding a shift is upon us is what’s most important right now, there will be plenty of time for identifying companies that will become the dominant players and losers.

8% upside on any given day may “feel” good in the moment, but they pale in regard to the pain of negative -20 to -35% returns the indices put up this quarter (and those who suggest otherwise are lying). Watching your net worth surge or plummet by 10% in any given day isn’t investing and it’s surly not managing risk.

We do our best to not “FEEL” anything, emotions are very powerful and can be extremely detrimental in times like these. We will remain data dependent and probability centric.

We have and will continue to spend quite a bit of time and effort attempting to educate clients and readers on understanding the business cycle. Our “belief” is protecting what investors have worked so hard will never be more important as we move forward.

The Federal Reserve is once again, fighting Economic Gravity … Will they win is a one-sided guessing game, the question we believe to be most poignant at this moment in time is win or lose, what carnage will be left in their wake. What asset classes will prevail given their most probabilistic path?

Hold and pray is what the investment industry preaches (it’s all they know). It’s why it took less than 3 weeks of negative market returns to turn more “Free Market Capitalists” into a bunch of Socialists begging the Federal Reserve to backstop and bailout virtually every industry within our borders, while extending FX dollar swap lines to foreign countries and emerging markets outside of them …

We’ll discuss the importance of all of the above, below…

Before doing so we think it’s important to note a few things:

I’m not a doomsday prepper, I don’t have a bunker in my basement, I don’t root for the failure of American companies or the loss of American jobs… We’re a firm with plenty of retirement account assets, which often restricts certain tools which can be used to profit in down markets…

My high school mascot was the Patriots… I’d like to think the education we’ve provided over the past few years has been nothing but patriotic… Admittedly, not easy to stomach, but truthful, factual and … patriotic.

In our humble opinion, there is an enormous difference between hoping our country fails vs. warning and educating as many investors as we can about business cycles; how they function, where we are in our current cycle and the glaring excesses in our economy perpetuated by poor central banking policy.

Would you consider Paul Revere anti-American for warning the colonial militia the British were coming before the battles of Lexington and Concord? How many lives were saved based upon those who heeded his warning…? How many lives lost by those who ignored it?

For all intents and purposes, we’re nobody’s in this business… We don’t have a Goldman or JP Morgan pedigree; we didn’t go to Wharton or learn complex derivative strategies and we won’t go down in the history books as Paul Revere…

I’m just a guy who’s seen more than he should over his career and opened this firm under the belief we could make a difference for those hardworking Americans who are poorly risk-managed by most in this industry. We believe we have accomplished this and will continue to do so; putting our risk adjusted returns over the years up against anybody’s…

We sure as hell saw this coming before the consensus following PhD/Wall Street “guru’s” … we guided you on how it would unfold, how bond ETF freezes would come, how IG to junk would create waves of uncertainty and opportunity … how the system couldn’t handle the leverage and discussed why…

I contemplated re-issuing our 2Q2017 note in its entirety. We literally hit it all in that note. Just about everything the Federal Reserve is currently attempting to prevent from collapsing today, we discussed in June of 2017; the role of credit and debt in our economy, manufacturing slowdown, auto, consumer, student debt, the volume of junk bonds needing to be repriced from 2019-2021, what Fed Chair Yellen was saying at the time vs. that of a retired Hank Paulson.

While we hope you do read that note in its entirety – we’ll share its final section we titled “The Experts”:

The Experts…

Above, I referenced and provided quotes from Former Federal Reserve Chairman Ben Bernanke. I don’t know him personally, I’m sure he’s a brilliant academic; though, clearly not always right, in fact, very often wrong, and publicly at that. I’m not picking solely on Bernanke here. I could cite examples of Paulson and Geithner – you could name most any CEO at any major financial firm back during that time who said they were “fine”; Merrill CEO John Thain repeatedly said the firm has enough capital, only to rush out and raise more, to then agree to be bought for a fraction of what it was once worth by Bank of America in a move of desperation. Dick Fuld of Lehman Brothers still blames others for the demise of Lehman, not poor risk management, lack of oversight, and plenty of greed. I could go on and on…

Tuesday, June 27th, 2017, during a Q&A discussion in London, Fed Chair Janet Yellen was asked about the likelihood of another financial crisis. Do you want to take a guess at what she said?

“Speaking during an exchange in London with British Academy President Lord Nicholas Stern, the central bank chief said the Fed has learned lessons from the financial crisis and has brought stability to the banking system…”

Yellen also made a prediction:

“That another financial crisis the likes of the one that exploded in 2008 was not likely “in our lifetime”.

She added: “I think the system is much safer and much sounder.”

“The crisis, which erupted in September 2008 with the implosion of Lehman Brothers but had been stewing for years, would have been “worse than the Great Depression” without the Fed’s intervention, Yellen said.

I often wonder how, at times, there can be such a disconnect between what is being said by so many of the most powerful, in the “know” people in this business, publicly vs. reality can be so large? How so many, so close to a situation can be blindsided?

I can only imagine how it feels to have every single word you say, scrutinized down to tone and inflection. How confidence alone, can shift the way hundreds of billions to trillions of dollars are traded every single day? Though, what happens when the weight of the world is no longer on your shoulders? Does your viewpoint change as you distance yourself from the internal strife of running a public company or the Federal Reserve – or the Treasury? Do your thoughts change a bit as possible conflicts of interest disappear?

If you happen to have NETFLIX, assuming you haven’t already watched it, I suggest you watch the documentary:

“HANK: Five Years from the Brink”

Released in 2013, it highlights the 2008/09 crises from the eyes and perspective of former U.S. Treasury Secretary Henry “HANK” Paulson, straight from the horse’s mouth. There is slight perspective from Hank’s wife, Wendy Paulson as well. It’s directed by Joe Berlinger.

While Hank Paulson has said some things that weren’t exactly accurate as he attempted to navigate what was nearly a global disaster. Fast forward 5 years to a time with no spotlight shining down on him; Having had time to reflect and think about things, with no hidden agenda or boss to please; he has, what I believe, to be some very poignant and timely thoughts…

“I get asked all the time, what’s the likelihood of another financial crisis? And I begin by saying it’s a certainty; as long as we have markets, as long as we have banks, no matter what the regulatory system is, there will be flawed government policies – those policies will create bubbles. They will manifest themselves in the financial system no matter how it’s structured and how it’s regulated.”

“When I came to Washington, the largest 10 banks held over 50% of the assets held in the banking system, 10 years early that would have been 10%. Today the problem is worse because obviously to get through the night, we needed to encourage consolidation. Too big to fail is a phenomenon that is definitely NOT acceptable.”

While Paulson does go on to say that he believes the banks are stronger, better capitalized and more prepared for a crisis due to more regulation. He concludes with this message:

“More still needs to be done with the shadow banking markets, the money market funds, the wholesale lending markets – the so-called repo market. When I came to Washington Fannie or Freddie guaranteed or insured roughly ½ the new mortgages in America, today, well over 90% are insured by the government. So today it’s worse.”

“I tend to look forward. The whole reason I am doing this is not because I want to look back, but because I have increasingly come to the view that it’s important that there be a historical record for those that come after me. So, we don’t replay this movie all over again….”

Given Paulson’s words were in 2013, and exploding bad loans have only gotten larger while credits have deteriorated further… My hope would be current Federal Reserve Chairwoman Yellen, give Hank a call.

Writing a note speaking to deteriorating credit and loan defaults brings me no joy. I don’t write these notes to be negative, nor to scare people; I write them from the perspective of what I would want to know if roles were reversed. I write them to empower people. I sincerely believe markets can move significantly higher from here based upon numerous factors, I wouldn’t be invested if I didn’t, but having a greater understanding of how our economy functions, what stress fractures may break and how it more than likely effects markets, helps us all be more prepared to navigate our boat as we head down these rocky waters. Having a capital preservation strategy and other small hedges allows you to take advantage of markets moving higher and seek for shelter when things become too volatile to stomach. Lying to yourself isn’t going to help anyone of our bottom lines. I have saved speaking about the oil and agriculture businesses for a later date, though, definitely something I’ve spoken about in the past and closely watching as rig counts move higher, prices will more than likely continue to fall.

It looks like we’ve learned nothing from those screaming from the roof-tops and we are replaying the movie all over again … Similar cast, similar Federal Reserve Response, some contrived twists and turns …

Final outcome is TBD.

Free Market Capitalist to Socialist in Record Time

It took the Federal Reserve roughly 2 weeks to go from equity market All-Time-Highs on February 19th to its first emergency rate cut since the GFC (Great financial Crisis 2007-2009) on March 3rd; less than 4 weeks for just about every self-proclaimed Free Market Capitalist from mainstream media to major Wall Street investment firms to turn Socialist as they begged for Multi-Trillion-Dollar bailouts… What’s worse is – in what amounts to be in the blink of an eye, they got them…

If you’ve been reading my notes long enough, you know that Wall Street needs markets to constantly move higher for their canned answer to “risk management” via ETF models to work. Buy and hold only works when things go up. Does it surprise you that in less than 2 weeks into a meager 20% fall in equity prices and blow out in credit spreads the Federal Reserve is executing emergency rate cuts while creating more Credit facilities then ever seen in the history of markets?

We’ve discussed “controlled narrative” for some time, most recently in our March Note. The prevailing narrative from financial experts, Federal Reserve officials and mainstream financial news for the past few years has sounded exactly like this: “The economy is in a good place” – “the consumer is resilient” – “Balance sheet run off is like watching paint dry” – “We see 3 rate hikes in 2019” – “repo operations are temporary measures” – “We see no need for future rate cuts at this time” (2 days later) emergency rate cuts… etc.… These are all quotes from Federal Reserve officials or financial media sources over the past year or so…

And yet: In under 4 weeks from All Time Highs, current bailout estimates stand between $8-12 TRILLION dollars… The ink had yet to dry on the government’s first $2.2 Trillion-dollar bill and Ms. Pelosi is already talking about the next bill needing to be over $1 Trillion… How about you make it a Quadzillion?! F* it, while they’re at it, what about a Bajillion? (which is clearly more than a Quadzillion).

“Breakneck” would be the word I would use to describe the speed at which the Federal Reserve has been moving. “Unprecedented” would be used to describe the size and scope of their programs… In order for you to have the slightest of understanding as to what we mean, we’ll again use historical perspective.

The Federal Reserve introduced QE1 (Quantitative Easing) on November 25th, 2008, which was expanded in March of 2009 and ended March of 2010. Per the Brookings Institute the Fed bought:

“a total of $1.25 trillion in mortgage bonds, $200 billion of debt issued by government-sponsored mortgage companies Fannie Mae and Freddie Mac, and $300 billion of long-term Treasury securities.”

That’s roughly $1.75 trillion in government & mortgage backed securities purchased over a 17-month time frame…

QE2 began November 3rd, 2010 and saw the Fed purchase another $600 billion of long-term Treasuries through June 30, 2011 (nearly 8 months).

September 3rd of 2012 birthed QE3, as the Fed bought $85 billion bonds per month ($40 billion mortgage backed securities and $45 billion Treasury bonds). By the time QE3 finally closed on December 18. 2013, the Fed added another $1.7 trillion-dollars’ worth of government securities to their balance sheet.

September 16th, 2009 the AIG Bailout equated to $85 billion dollars… GM’s (General Motors) restructuring amounted to roughly $50 billion.

Bringing us to current times:

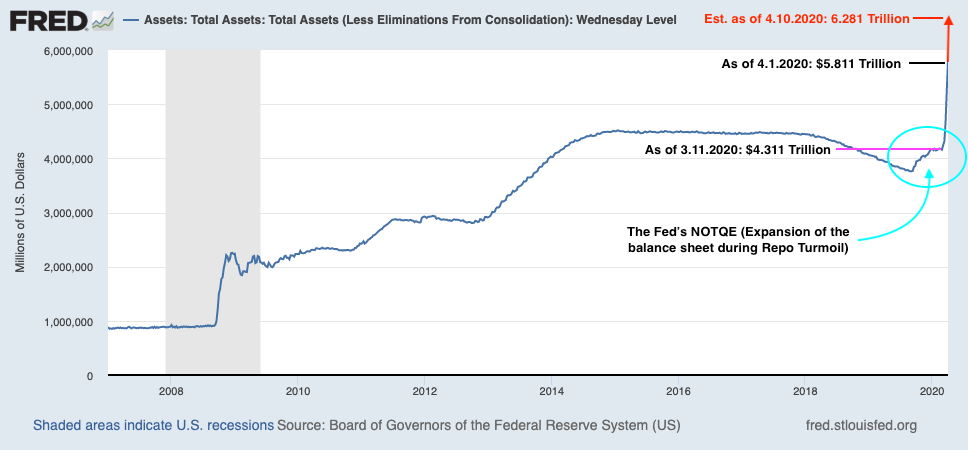

March 23rd – March 27th the Federal Reserve purchased roughly $625 billion dollars’ worth of Treasury and MBS (Mortgage Backed Securities) in a single week ($125 billion PER DAY). Said differently, the Fed bought more Treasuries and MBS in a SINGLE WEEK then ALL assets purchased during the entire duration of QE2 and while slowing down, we’re still looking at between $60-75 billion per day.

In 15 business days, the FED has added just under $1.5 trillion of Treasuries and MBS to their balance sheet, which has exploded from $4.311 Trillion on March 11 to $5.811 trillion. Let me say that again so it resonates … ROUGHLY $1.5 TRILLION … in just over 3 WEEKS. Given the NY Fed’s open market operation time line, by the time you read this note it is with great likelihood the Fed’s balance sheet sits at $6.281 trillion dollars…

Virtually overnight, the Fed has created multiple new lending facilities as detailed in a recent Bloomberg opinion article written on March 27th by Jim Bianco of Bianco Research (we highly recommend the read):

- CPFF (Commercial Paper Funding Facility) – buying commercial paper from the issuer.

- PDCF (Primary Dealer Credit Facility) – supply credit funding auto loans & mortgages

- MMLF (Money Market Mutual Fund Liquidity Facility) – supporting flow of credit to households.

- PMCCF (Primary Market Corporate Credit Facility) – buying corporate bonds from the issuer.

- TALF (Term Asset-Backed Securities Loan Facility) – funding backstop for asset-backed securities.

- SMCCF (Secondary Market Corporate Credit Facility) – buying corporate bonds and bond ETFs in the secondary market.

- MSBLP (Main Street Business Lending Program) – Details are to come, but it will lend to eligible small and medium-size businesses, complementing efforts by the Small Business Association.

While we try to keep these notes within the confines of the quarter this is too important not to share…

4/9/2020

4/9/2020 will be a day that sticks with me for a very long time. It is the date I lost faith in the system… Definitely my profession… and to a degree, humanity…

Just about every profession has a defined set of rules; a construct as to how the proverbial game is played. An accountant works within the IRS tax code; some accountants are better or worse at understanding and interpreting those rules and how they may apply to different entities, but the rules are defined.

Think of a sport like football. There are basic rules to the game. You get 4 downs to move the ball 10 yards, a touchback typically places the ball on the 25-yard line, each team is awarded 3-timeouts per half … Again, we know what the rules are, and then design strategies based upon the construct of the system. (yes, we understand an occasional a penalty is missed – not the point).

Those of us who have been in the financial industry for some time understand the game is skewed. When times are good and equity markets are moving higher, traditional rules apply… When markets see some form of turbulence, you proceed with the understanding that the Refs (Fed) will swing a call, in favor of the Bulls.

Think about it…

Have you ever seen a “circuit breaker” halt trading because stocks move higher by 7% on any given day? What about implementing a “tick” rule when things are moving too high too fast? The answer is NO, you haven’t.

But as soon as equity markets roll over and sell-off (as discussed earlier), we see emergency rate cuts by the Fed, new credit facilities established; short sellers become vilified, the talk of banning short selling and inverse ETFs become daily talking points; heck we recently heard financial media floating the idea of closing markets in an effort to “calm them down”.

While unwritten, not much of this should surprise us; industry veterans should anticipate them…

But when you literally trample all over the rule book because you’re “losing”, it becomes incredibly disheartening.

On April 9th the Fed announced even more credit facilities than they had previously…

- MLF (Municipal Liquidity Facility) – SPV to buy $500B of municipal bonds

- Expansion of PMCCF, SMCCF, MSBLP & TALF

This announcement, however, unlike others includes these new gems where the Fed will:

- Buy JUNK BONDS (if downgraded after March 22)

- Buy JUNK ETFs (HYG)

- Buy PPP (Paycheck Protection Program and CARES loans)

- Expand existing SPVs Buying JUNK BONDS via ETFs.

Given the Fed’s actions in setting up SPVs (Special Purpose Vehicles) and acting in concert with the “approval of” the Treasury Department, the Federal Reserve has relinquished itself of its “independence”. While we could argue the degree of Fed independence and the tightrope they have walked in the past, they remained within the scope of interpretation when it came to rules, laws and mandates.

They spit on the FRA (Federal Reserve Act) when they began buying corporate bonds and ETFs, but to announce that they will be buying JUNK bonds via JUNK bond ETFs is reprehensible. They are called JUNK for a reason…

“Such policies and procedures shall be designed to ensure that any emergency lending program or facility is for the purpose of providing liquidity to the financial system, and not to aid a failing financial company” Federal Reserve Act Section 13.3

The above quote comes directly from the Federal Reserve Act – section 13.3. We would encourage everyone to read it, so you can understand the scope of what I am saying; there is very little room for interpretation. Additionally, in taking orders from Secretary of Treasury Mnuchin, and President Trump being Mr. Mnuchin’s boss, these SPVs are in essence being run/overseen by the POTUS – the government is now nationalizing our businesses at the expense of taxpayers.

The damage to our financial system goes beyond the scope of what most can fathom…

The Fed is attempting to control the yield curve via their QE price discretion (buying treasury assets up and down the curve) without restriction. They’ve become a small business lender & virtual investment bank of last resort to struggling corporations who can’t get access to credit markets. In accepting virtually everything but the kitchen sink from financial institutions in the form of collateral (including equities, BBB rated bonds, Corporate and now municipal bonds via SPVs (Special Purpose Vehicles) which they are funding at the treasury … they have again distorted the price of RISK in virtually ALL asset classes and markets.

At this point, the Fed and Treasury are not even trying to hide their blatant disregard for rules. They’ve far surpassed “walking a proverbial tightrope” differentiating right from wrong as rules and government procedure appear to be irrelevant in the eyes of Fed officials today; and worse, no one in a position of power is questioning them as they, from the POTUS to majority of Americans appear to view things differently when their net worth and portfolios are down 25-35% and are in all out panic mode to stop the bleeding.

Fueled by a failure to properly risk manage assets by virtually everyone in the industry. Who can blame them, they were encouraged to take on excessive risk via the Federal Reserve’s monetary policy and now they are being taught that the word “accountability” has no meaning? When those making the rules are directly affected by the rules they are breaking (making), conflicts of interest are everywhere…

The fiscal irresponsibility of our politicians and central bankers is criminal… It has decimated millions of jobs within weeks, bailed out Wall Street executives who have mismanaged balance sheets (again) and destroyed the retirements of savers and pensioners … as well as the future financial stability of our great country for our children!

They’re at it Again…

“The Fed’s actions have artificially suppressed the truest of price measures our economy has; INTEREST RATES… Having done so for such an extended time frame, it’s nearly impossible to have honest price discovery in any asset class when THE asset just about everything else is priced off of (i.e. a spread off of these rates) is an artificially low manipulated disaster.” OSAM 4Q2018

Virtually every asset we price in markets, in one way, shape or form is priced off of the risk-free treasury, whether it be a bond spread priced off the curve or an equity discounted cash flow model.

Initially, this quarter saw credit spreads widen at an unprecedented pace (because credit risks were being exposed for what they were) RISKY CREDITS. That was, of course until the Federal Reserve’s newly created credit facilities ramped up their ETF & corporate bond buying bonanzas, turning investors back into IG (investment grade) buyers with the belief being that the Fed will backstop them should things go poorly…

After the Fed’s April 9th announcement, the masses in my chosen profession cheered; gamblers investors jumped back to Junk bonds and Junk bond ETFs with reckless abandon… Did the economy re-open? No … Did the companies we’re trading ownership shares in report positive earnings? Nope … Has COVID-19 disappeared or the death rate begin to decrease? Try again … MLB announce their first game? Nice try!

They cheered because the Federal Reserve abandoned any sliver of morality that may have existed in this industry. They cheered yet another Federal Reserve “kitchen sink” bailout; this one to the tune of $2.3 Trillion dollars…

To this we’ll first say, buying based upon a rating should NEVER be mistaken for buying quality but more so, bond buying, whether it be corporates or junk doesn’t FIX the underlying root cause of this problem. (we’ll comment more on both points later).

As if things couldn’t get more rich?! Guess who’s now in charge of this corporate & Junk bond buying spree?

On March 24th the Federal Reserve hired BlackRock to serve as investment advisor and asset manager for three separate programs within two of the above aforementioned facilities. As reported by Bloomberg:

“BlackRock will serve “as a third-party vendor to operationalize these purchases and transact with the primary dealers,” the New York Fed said”

Yep, the world’s largest asset manager and issuer of ETFs (including those junk bond ETFs that are stuffed with the absolute SHIT credits I’ve been talking about for years) will now be in charge of buying their own garbage assets along with that of their competitors in an effort to manipulate create price stability in markets.

Rest assured, they won’t be able to charge the Fed (taxpayers as the Fed is now backstopped by Treasury) for ALL of their services. Well pin my tail and call me a donkey:

“BlackRock will treat BlackRock-sponsored ETFs on the same neutral footing as third-party ETFs,” according to initial terms of the agreement for that program” WSJ March 27, 2020

Ahhhhh – sure they will… You really can’t make this sh*t up folks – I’m fairly certain there’s a well-known idiom for this circumstance??? Hen’s, meet your new nighttime security guard…

The Fed is doing everything, they can to manipulate markets in an effort to push back the largest credit default cycle in history, they still have a few very large problems, in our humble opinion…

What could possibly go wrong?! Just…

The Mispricing of RISK… AGAIN!

As the Fed takes on an obnoxious amount of corporate debt as collateral, it frees up the balance sheets of banks and hedge funds to further lever them (actively participate and “support” asset prices giving them an artificial floor). These actions coupled with Blackrock buying copious amounts of corporate and Junk bonds along with bond & Junk bond ETFs, are intended to do the same.

As Lisa Abramowicz from Bloomberg recently noted on twitter, “NET DOWNGRADES among Investment Grade bonds ACCELLERATED to $110 billion Monday from $91 billion Friday … The pace of downgrades continues to accelerate from the record pace reached last week”. citing Bank of America research.

The WSJ had this to say on 4.2.2020

“The index, known as the ICE BofAML U.S. Corporate Index, has suffered $569 billion in downgrades since March 16, said Bank of America.”

But what does mispriced RISK really look like?!

Let’s think of an example for a nanosecond, ah – got one:

Argentina literally just defaulted for the 9th time in history a few days ago – on a CENTURY BOND no less. A century bond is as it sounds, it’s a bond that matures in 100-years (a century). This country had defaulted 5 times in the last 70 years, this most recent being it’s 6th since 1951. Who in their right mind thought it to be a good idea to buy a 100-year Argentinian bond due in 100 years when the country had defaulted 5 times since the 1950’s, most recently 2014?! What’s worse, odds are many people likely owned the bond via a bond fund they own and had no idea?! The largest holder of a fairly recent Austrian century bond trading with negative yields was Vanguard Total International exchange traded fund… One of the largest bond funds out there owned by retail investors. Got Junk?!

MISPRICED RISK… 7.9% for 100 years is mispriced risk – negative yielding bonds maturing in 100 years is MISPRICED RISK… and most people have not a clue as the Federal Reserve is burying and hiding this risk, again…

The vast majority of borrowers around the globe have budgeted based upon monthly cash flows. Can I afford the monthly payment? Any interruption to that cash flow would have created this credit default cycle … as we explained in detail, over 2 years ago here. The reaction to COVID19 is no simple disruption, it’s an existential shock exposing every overleveraged company and government out there until the Fed decided to misprice risk, again…

Nearly 2 decades of Central Bank policy has created this quagmire, QT (Quantitative Tightening) got some kindling smoldering, Repo market and the Fed’s NOTQE QE liquidity injections stoked bond prices to all-time highs artificially suppressing risk leading up to this crises, credit spreads FINALLY blow out and widen to reflect and price in true risk (catching up to reality) and now the Fed’s new facilities are destroying the single most important mechanism for true price discovery to take place (as they and Blackstone have become a never ending buyer).

All the while bankruptcy attorney’s prepare for what amounts to be an onslaught of bankruptcies; not just chapter 11 or 13 restructurings, but chapter 7 (I’m out of business).

For those of you who like irony… I have been all over ratings agencies for years as the pace in which they have been downgrading Triple-B bonds from IG (Investment grade) to Junk has been near turtles’ pace.

Would you find it ironic that the within hours of these new facilities being announced both Delta Airlines and Virgin Atlantic were downgraded to Junk? Would you find it funny that the Federal Reserve backdated these programs to buy Junk if it was downgraded AFTER March 22nd?

WHY MARCH 22nd one might ask?

Would you find it ironic that the nearly 3 ½ year overdue (our estimation) Ford downgrade to Junk came on March 24th, which means that their newly junk, Junk bonds can be included in the Federal Reserve’s new Junk bond SPV vehicles being executed by BlackRock?! They literally BACKDATED their program to include Ford’s debt because the Junk market can’t handle it…

We’ve been talking about auto manufacturers for years, specifically Ford and GM. 1Q2017, 2Q2017 & 3Q2017…

Many of you have read this piece, but for those who haven’t – Our special note titled MOAB specifically discussed IG to Junk downgrades and the devastating affects it would have on markets. Virtually everything we wrote in that piece over 2 years ago has come to fruition – Investment grade downgrades to Junk, Bond funds freezing redemptions, liquidity being unavailable, and on and on…

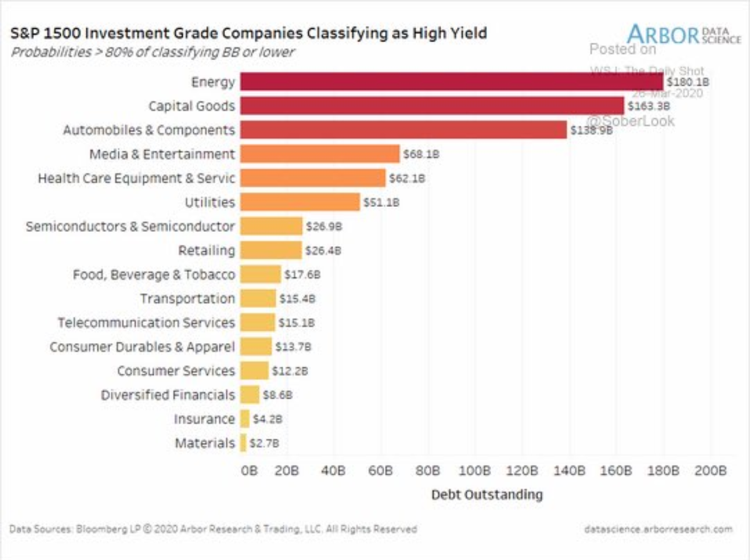

For years we have told clients and readers that a point in time would come where more money would be made buying Investment Grade bonds downgraded to junk while assuming less risk than investing in equities… In 2017, I targeted 2019-2021 based upon the mountain of debt that needed to be re-priced. Just take a look at the volume of debt independent research believes to be BB (Junk) or below (without the ratings agencies “discretion”).

This thesis was playing out brilliantly until the Fed began circumventing the Federal Reserve Act, injecting multiple trillions into credit market, creating 10 newly formed facilities & SPVs buying everything from commercial paper, CLOs, consumer debt (auto, student, house), FX swap lines and Junk Bonds.

Technically, given the Fed’s actions, I have admittedly failed (for now). While I anticipated a robust response from the Fed, their throwing around TRILLIONS with no regard for future consequence is beyond comprehension (more on this later). But it’s important we show you what we mean by the Fed mispricing risk in real time. Just because they’ve done what they have, it doesn’t mean the problem has been fixed. Our assertion is they’ve again given people false hope by masking the true risk.

We’ll use Ford as AN EXAMPLE…

As the crisis unfolded, Ford’s debt which was trading in the low to mid 90’s sold off to roughly fifty-five cents on the dollar ($0.55/$1.00). On April 9th, the day where the Federal Reserve announced their illegal and unethical JUNK BOND PURCHASE PROGRAM prices on Ford bonds jumped from roughly $0.55 to $0.815 or ($0.815/$1.00) – a 48.18% gain in a single day. THIS IS WHAT MISPRICED RISK LOOKS LIKE IN REAL TIME.

It had been reported that Ford was within 15-17 weeks of cash left on the books to operate. If true, it not only shows how poor and inaccurate the ratings agencies were with rating this a BBB for so long. But with high likelihood, their bond prices would have gone MUCH LOWER giving those investors who have been prudently waiting for the ability to make a TRUE risk/reward decision. Do I buy the bonds? Do I think the bonds will recover? Will Ford file for bankruptcy? If Ford files for bankruptcy, where in the credit ladder do the bonds that I own fall? If they go to liquidation, what would the “recovery rate” to bondholders be?

At the moment in time the price of Ford bonds were skyrocketing following the Fed’s announcement to buy Junk, the cost to insure against default was plummeting as the probability of default dropped from roughly 20% to 14% in what amounts to be the blink of an eye.

On 4/13/2020 Vice Chairman of the Federal Reserve Board of Governors, Richard Clarida stated on Bloomberg news:

“There is nothing fundamentally wrong with the U.S. economy.”

And that expansion of the Fed programs to include some junk bonds:

“is to help companies that were investment grade before the crisis.”

What the F*ck is this guy smoking??? Given all we have written in the past about Ford dating back YEARS, Ford should have been JUNK for quite some time ago. The Fed is stomping on every bit of the Federal Reserve Act because these companies “had” an investment grade rating before the virus?! These companies have been poorly run pieces of garbage for years – Ford’s production for the first half of 2019 had fallen to levels not seen since 2016 which we noted here:

“Last week, as reported on by the Wall Street Journal, GM, Ford (F) and Fiat Chrysler (FCAU) reported their worst first-half auto sales in years. GM’s drop to 1.57-million units was its worst since 2013 (a 15% year over year decline), while Ford’s roughly ~290k units was the company’s worst first-half year since 2012) a 27% year over year drop and half of what their first quarter sales were in 2016.”

Ratings agencies have been afraid to deal with the “ratings-based mandates” we’ve highlighted for years because they knew the ramifications; they have failed to do their jobs. Three ratings agencies, all who failed us in 2008 and now screwed the pooch again, are the catalyst to allow the Fed to buy JUNK?! Earth to Clarida, ratings agencies are publicly traded firms who gets paid to rate these bonds, and the more debt they rate, the more money they make. Ford will issue more bonds as IG then they will at Junk, thus more revenue for ratings agencies and their shareholders. Have we forgotten the AAA ratings agencies attached to CMOs in 2008/2009 that brought our economy to a crippling halt?

Ratings agencies are once again complicit in having refused to downgrade countless credits to Junk status even as these companies faced revenue black holes until the Fed finally backstopped their mistakes … Shameful!

Again, I am a nobody and saw this coming from a mile away, Clarida is one of the very few “in charge”; they’re supposed to be the smartest of the smart finance has to offer… Not only have they never seen a crisis coming, but they continue to lie through their teeth because they don’t believe you have the intelligence to handle truth. The Fed has failed us again – Traditional Wall Street has failed you again – when do people start believing in a better way?!

Successes and Failures…

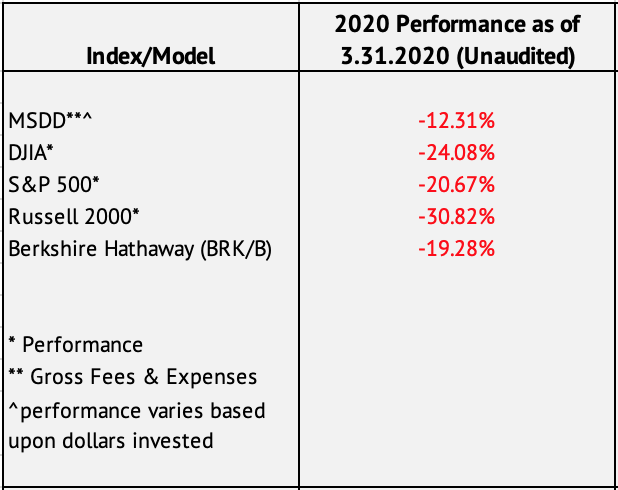

Speaking of the truth – this is how things shaped up for us vs. the broader indices as of 3/31/2020…

If we are looking at a snapshot in time (which readers know I can’t stand), we did outperform just about all major indices and sector ETFs for the quarter. There were times in the month of March, we were down significantly less, while “markets” were down much more. Above, we adhere to the traditional measuring stick.

Had we been reporting to you a week prior we had been down roughly 10% while major indices were down 30, 35 and over 40% for the S&P, DJIA and Russell respectively. As we got closer to quarter end our short exposure put pressure on performance as broader markets rallied into quarter end (and have continued to do so).

Without question, we have been much less volatile than most asset managers out there. Though we have also made mistakes. Some would argue we’ve pressed our short positions a bit too much; we’d challenge suggesting that all depends on your timetable which we’ll discuss below. I believe in striving for excellence and we view our mistakes as failures. We humbly and respectively submit you’ll be hard pressed to find many asset managers who have had the outperformance, limited volatility and drawdowns as we have over this last quarter yet is more hyper-focused on our failures than our successes?! We will strive to get better every day, that’s a promise.

If the Fed is doing so much to prop up asset prices, why not just push our chips all in and capture the upside of quarter end and recent weeks?

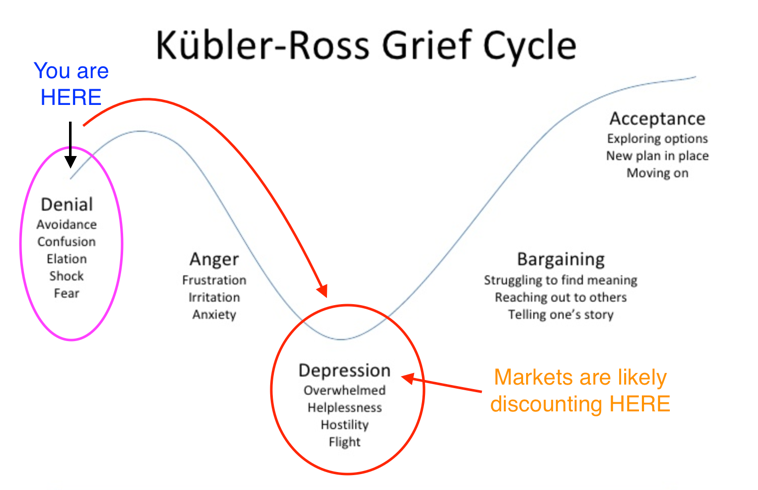

We’ve spoken about economic cycles before; yet there are cycles to human behavior as well; there are stages to the “Grieving process”; 5 that I know of; denial, anger, bargaining, depression and finally acceptance.

With Equity markets currently down 18-30% from the most outrageous levels in history, the current Wall Street narrative and belief is that further downside is already “priced in”; that we are currently seeing one of the best buying opportunities of our lifetimes. What we believe is currently “priced in” to equity markets is complacency, disbelief and denial. The vast majority of individuals haven’t even begun to shift their mindset and thinking towards down the “grief process” of this economic cycle.

Cycles Matter, as we explained in our 3Q2019 note… As does Economic Gravity, which we explained in our November 2019 note and as we’ve discussed for some time, the FED is attempting to fight both.

Think about this for a moment… over 22+ MILLION people have lost their jobs in the last 4 WEEKS with MILLIONS more in the que. After 4/16/2020, the Fed’s charts are ~10,000,000 people behind…

That’s MILLIONS of “resilient consumers” that have been “over consuming” for the past decade which represents 75-80% of the economy as Jay Powell has reminded us as he’s lied through his teeth for the past two years…

At a time when millions of Americans became unemployed in a blink, asset managers and fiduciaries of Wall Street, those tasked with the responsibility of prudence, determined it was in the best interest of those who follow the 60/40 asset allocation model (which is most individual investors), to rebalance their portfolios jamming equity prices higher into quarter end … taking billions of dollars taken OUT of safe haven assets like US treasuries and invested them into STOCKS.

As markets rallied on from March 24-26th, we systematically added slightly more “short exposure” to our portfolios. It never feels good going against the grain of what consensus is doing and yes, in the “short term”, the gap in our outperformance vs. major indices narrowed (remember we told you rip your face off rallies will occur in Bear Markets). Yet, we’re not investing for three days of performance, NOR are we “window dressing” our portfolios to report to you a “snapshot in time”. Wall Street may have individuals brainwashed to believe end of quarter is the measurable as to which everyone needs to follow – but is it really?

Facts don’t cease to exist because investors chase every last bit of FOMO (Fear Of Missing Out), neither does our thesis. 22+ MILLION people didn’t go back to work over the last week. Markets didn’t become more attractive as they ripped higher in the short term. The economy (not to be confused with “Equity Markets”) didn’t get better because our illustrious POTUS is attempting to manipulate markets by tweeting about higher oil prices. Economic FACTS got uglier:

As unemployment spikes, financial institutions are going to make it MORE difficult for individuals to get or refinance a mortgage or loan (unless guaranteed by the Fed of course) as borrowers become more RISKY credits. You see, bankers (and I’m not talking Wall Street), but small business lenders do attempt to gauge risk. In the Fed backstopping what they are, their masking the ability to measure risk; on the bank lending side as well.

Reducing bank leverage ratios in an effort to allow financials to lend more doesn’t mean that they will. JP Morgan’s just increased their lending standards on mortgage requirements; this is NOT bullish for the housing sector by any means. Whether the government opened the economy tomorrow or not, we are at the very beginning stages of the part of the cycle.

J.P Morgan will not be the only financial institution to implement more stringent requirements on ALL lending, not just mortgages. As financial institutions tighten lending standards, less credit will be extended perpetuating the contraction in the economy. This is classic end of cycle behavior as institutions know people without a job are MUCH MORE APT to fail on their mortgages, auto, student and credit card loans… Should the Fed attempt to put ALL of this under their umbrella?

We fear the long-term ramifications… See Japan’s failed Central Banking policy over a 30-year time frame advised largely by Former Fed Chair Ban Bernanke…

We will concede C&I loans have recently spiked, though it has much more to do with companies drawing on their credit lines than anything else.

While Fed Chair Powell has been cheerleading a “resilient consumer” and “50-year lows” in unemployment, we’ve been telling you why this wasn’t good news, but bad. When earnings are flat to negative over 5-6 quarters “Fat needs to be cut”. That fat = layoffs, layoffs = a weakening consumer. Powell accurately points to the consumer as 75+ % of the economy, (they are just not as resilient as he maintains). At the end of a business cycle, layoffs = weakened consumption, which in turn leads to recession (or in this case, a likely depression). When you place excessive debt and leverage from the consumer to Federal Government on top all BEFORE COVID-19 became a serious catalyst – Houston, we have an enormous problem.

The cycle has to bottom before employers just “rehire” everyone that’s been fired or furloughed. Equilibrium will need to be found. Employers will gradually add employees in an effort to find what that equilibrium is as consumers consumption and demand resurfaces. Again, it doesn’t and won’t just happen overnight.

Take the restaurant industry… In a recent survey by the NRA (National Restaurant Association not the one you traditionally think of with that acronym), they found that of the more than 4,000 restaurant owner/operators surveyed, 11% anticipate they will permanently close within the next 30 days, while 3% said they already had permanently closed.

“Any pundit who thinks that they’re going to use a recent history — and by recent history, I mean the last 100 years, including the Depression — as a template for what is going to go on here? They’re kidding themselves,” said restaurant industry investor and advisor Roger Lipton. Business Insider 3.31.2020

When the economy attempts to turn the lights back on, it won’t just be the restaurant industry that doesn’t snap back in the blink of an eye. Do you sincerely believe people are currently planning luxury cruises with all that money they are making while on unemployment? Travel, hotels, restaurants, Uber/Lyft (ride share services)? Because the government says, “GO”, do you think ALL people will feel warm and fuzzy about getting close to each other?

We argue the answer to all of these questions to be a resounding NO and we believe the data supports our argument.

Time and Space…

There is no check the Fed can write which substitutes time and space… Think about this rationally for a moment. Can you refinance a mortgage without a job? Will you qualify for a mortgage with NO JOB? I hope everyone reading this understands the answer to these questions are NO… As of this morning, 22 million resilient consumers unable to refinance or qualify for a mortgage – what happens to the Real Estate market with NO BUYERS? What happens to mortgage bankers?

Another question to ponder regarding Real Estate. Online companies like Zillow began to buy and flip homes in Mid-2019… What happens to them? Or the likes of AirBnB “super-hosts” which have leveraged countless homes (10-30+)? There is literally zero travel taking place, no one renting these homes out, who’s paying these mortgages?

While at the same time the Fed’s most recent intervention into the MBS (Mortgage Backed Securities) markets are triggering, “a flood of margin calls on hedges lenders have entered into to protect themselves from losses” as reported by Bloomberg, they continued:

The rally in prices for mortgage-backed securities that’s been fueled by the Fed’s large-scale buying is “leading to broker-dealer margin calls on mortgage lenders’ hedge positions that are unsustainable for many such lenders,” the trade group wrote in its letter to SEC Chairman Jay Clayton and Financial Industry Regulatory Authority President Robert Cook.

What happens when large retailers like Dick’s Sports, Staples and Petco don’t pay their rent? Or Cheesecake factory, Mattress Firm, Subway, Tesla? Again, mortgages don’t default overnight, nor does a problem such as the one we are currently in. The Fed is writing checks, delaying mortgage payments and recklessly buying bonds, they are doing their best to replace cash flow and consumption and may be able to do it temporarily; our belief however, is that we haven’t even begun to feel the default rates in very large, systematically important areas of the economy.

Overleveraged cash strapped companies with razor thin margins are no different than highly indebted individuals living paycheck to paycheck. Should cashflows be adversely affected, defaults occur; when it happens to the individual it’s considered “small scale” … when it happens to countless individuals, corporations, and governments at the same time it becomes a crisis of epic proportions.

There are so many people hoping and praying for a speedy recovery for the simple but mere fact that most investors weren’t risk managed properly in the face of this crisis and don’t know what to do when markets sell off daily. We’re seeing enormous stimulus numbers and multiple Federal Reserve initiatives pop up by the day, as they encourage people to buy stocks… Mainstream media suggests these are deals/bargains of a lifetime.

If markets are forward looking instruments and the majority of companies are WITHDRAWING forward guidance, do you believe equities should be trading near 130% market cap to GDP (still one of the all-time high valuations for this metric).

Could there be deals of a lifetime? Sure… Anything could happen. I won’t dismiss the chance that we could see an asset bubble re-appear in the face of all out recession/depression. Given enough government money printing your hyperinflation, in theory, could wind up in equity asset prices?!

Though, if you’re one of the 22+ million (and growing) unemployed standing in a food bank line for 4 hours waiting on some hamburger helper while farmers around the country are plowing under their fields of fresh produce as the government mulls over whether or not to PAY oil producers to NOT PRODUCE and equity markets began hitting all-time highs because governments are bailing out wealthy CEOs who took on too much risk, how would you feel? My friends, I apologize to be the one to tell you this, but this has just begun…

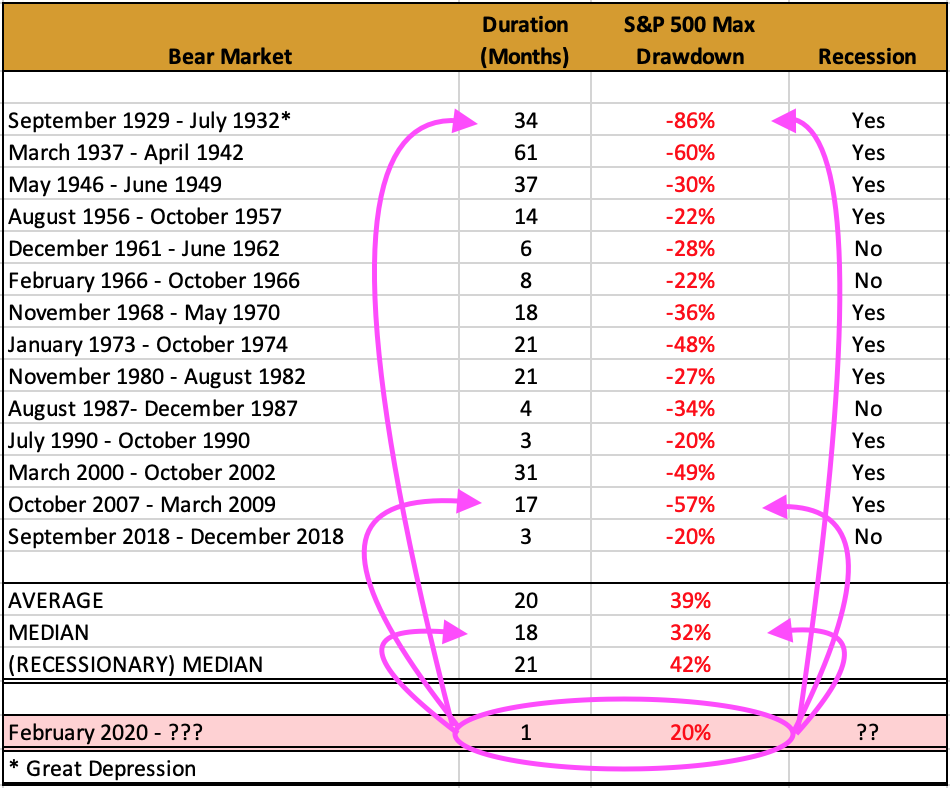

Below is a simple spreadsheet showing the typical duration of Recession/Depressions along with the average drawdown.

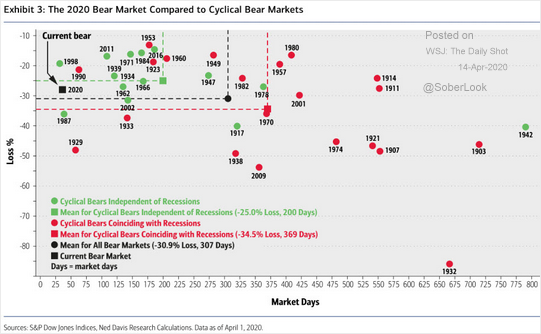

As I was finalizing my proof reading, Danielle DiMartino Booth presented the below graph courtesy of @SoberLook the WSJ’s Daily Shot which is a much better illustration of where we are in the cycle relative to other bear market cycles since 1900.

We are making new records…

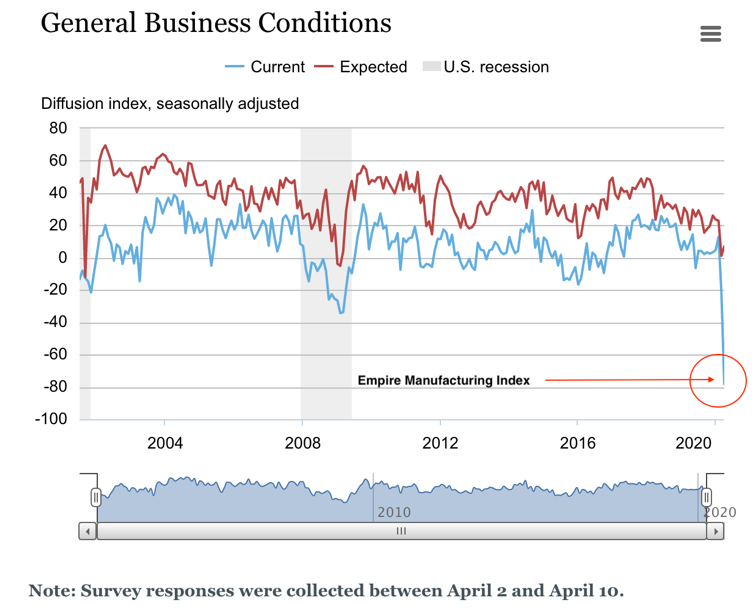

Unfortunately, they just are not the ones that support inflated asset prices. Such as… The Empire Manufacturing Index fell to -78.2% – LOWEST on RECORD. This below graphic should speak for itself – NO commentary necessary.

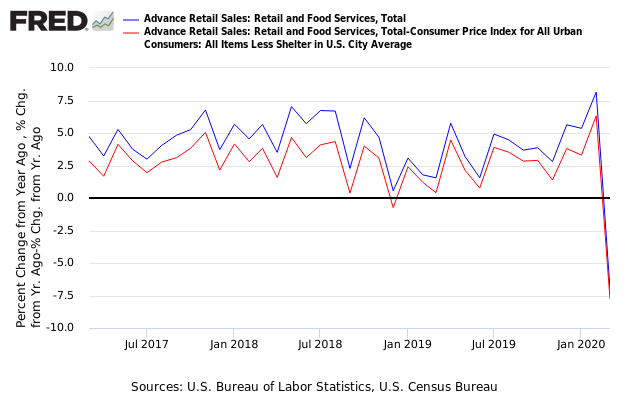

Headline Retail Sales for March came out @ -6.17% down -10.78% MoM which is the largest MoM (Month over Month) decline EVER (for those wondering, “EVER” is kind of a long time) … Mind you, this is for March – April will have been shut down completely.

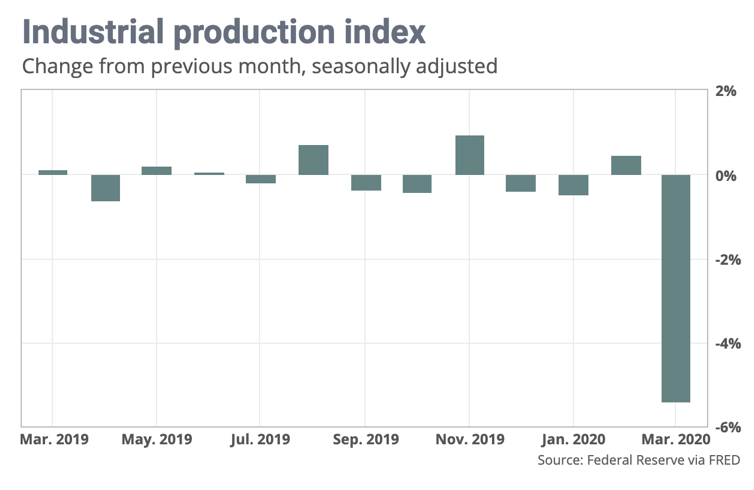

March industrial Production was -5.4% against a -3.2 to -4.0 estimate … This is the worst reading since 1946 post WWII.

Peak to trough from 4Q2007 to 2Q2009 real GDP fell -4.3 percent, the largest decline in the postwar era. The unemployment rate, which was 5 percent in December 2007, rose to 9.5 percent in June 2009 (roughly 19 months). 2Q2020 alone is anticipated to see -6% GDP decline … again, perspective: the second quarter alone will be worse than entire peak to trough decline of the entire GFC. Do you honestly think prices should remain elevated near all-time highs with 3Q2020 likely to be worse?

At the bottom of the great depression in 1934 we still saw 75% productivity off of highs with 22% unemployment. Equity markets were down 86% during the Great Depression and 57% peak to trough during the GFC. I don’t think Mr. Bernanke studied the great depression as much as he leads on. Maybe he should read Hoover’s Memoirs? Eh… why let history get in the way of an agenda when you can just re-write it?!

Understanding what I just wrote, given the size and scope of our current situation with the majority of global business screeching to a halt, do you think equity markets are being realistic given the underlying economics or is something slightly off? Our opinion is something will give … equity prices may move higher, BUT AT WHAT COST?! Arguably, it won’t be good, but more importantly are there safer ways to be positioned then simply thinking stocks?

We’ll continue to stick with Odds over Outcomes as we wrote about in August of 2019; investing based upon the most probabilistic outcomes as the underlying data presents itself.

We don’t make “emotional” investing decisions here. What emotion I have or internalize is checked at the door when it comes to our process. We look to the real underlying economic data in order to make the best decisions based upon the highest probable outcomes within the scope of an Economic Cycle.

Recessions and crashes aren’t fixed in a 4-day or 2 week-long equity market rallies. They aren’t fixed because the Fed creates multiple SPV’s or decides they want to throw $6-12 trillion in bailouts while handing out $1-3k checks to the American public. Wall Street can only turn a blind eye to the abhorrent economic data for so long.

At some point in time PhDs at the Fed and politicians will learn you can’t fix a credit crisis by writing checks and pushing more credit. They are fixed when the business cycle has time to work through the credit default carnage.

We’re not going to flip-flop our positioning on a day to day basis because the gap in outperformance between our models narrow on emotional buying, fear chasing, and absurd quarter ending rebalances. We’re going to manage that risk the best we know how. We do plan on making adjustments to our position sizes and will look to trade around some of those core positions.

I don’t do politics – don’t talk them often – though If someone were to label me it would likely be libertarian. I have never and will never beg for bailouts. I am a firm believer we are all products of our decisions (some have easier or more difficult decisions to be made), none the less, had investors been properly risk managed through this process and corporations run prudent balance sheets they wouldn’t have needed to beg for handouts from the Fed. Those who take excessive risks should fail (in my humble opinion).

Bankruptcy laws exist for a reason. If you’re going to backstop anyone, backstop “we the people”. $350 billion in small business loans to 4.5 trillion to irresponsible CEOs of large businesses doesn’t really seem all that “fair” when nearly 50% of our economy is small business. (again, in our opinion)

This continues to be a leverage, debt and credit quality problem. As we have SCREAMED for some time – you can’t fix a credit/debt problem with obnoxiously more debt. EVERYONE is and has been over leveraged for decades now; the resilient consumer narrative that has been sold to the American public has been a flat out lie and is exponentially worse with 22+ million Americans no longer being in the workforce. Corporations, governments (local, state and federal) as well as EM (emerging markets) are up to their eyeballs in debt…

Why am I beating this concept along with that of mispricing of risk to death?

The Fed Reserve buying debt may support asset prices in the short term, and in many cases, we’ve watched it surge. What we are having an extremely challenging time seeing is how they can artificially manufacture consumption in perpetuity. Clearly, they are now handing money out to all individuals, companies, governments, etc.. in an effort to replace cash flows from unemployed individuals. How do they turn the spigot off? With the POTUS overseeing the Treasury who’s overseeing these SPVs buying assets in an election year? (spoiler alert: they can’t)

We don’t believe the Fed will be able to replace consumption to the degree that it was; they can supplement unemployment for a while, but to what degree and for how long … Got GOLD?

We have a strong conviction for gold, for those who don’t understand why, we would urge them to study history. In the near term, we also believe in the US dollar. I know this is conflicting for most as one would think the dollar would get decimated given what the Fed is doing, however, when viewing the dollar through the lens of the rest of the world, there is an enormous dollar shortage. This, in and of itself will create more issues for Emerging Markets and their debt denominated in dollars, but this topic is outside the scope of this note.

Treasuries will be bought to by the Fed so long as the government needs to fund its deficit spending. Additionally, given all the unemployed and poor consumption data, we still like treasuries along the curve.

We believe buying equities with little to no earnings at these valuations is dangerous, as is buying those companies who are staring at a consumption cliff (those who pulled so much consumption forward as people prepared for the shutdown has now created a gap in forward demand). How many people need more toilet paper?

We will dip our toes back into well run businesses with solid free cash flow as things become clearer. We touched on this earlier; the Fed can’t place people back into Disney World nor put them on airplanes or into hotels with fancy restaurants attached to them. With what little in savings individuals have, that money will more than likely go to consumer staples, some discretionary and utility companies (which just happen to be your recent outperforming sectors).

While earnings have just begun to be released, the average release is -34.5% as I write.

We have shied away from buying just about anything “equity” given volatility where it is. We are in the early innings of this and with such a short period of time having past, we don’t believe we’ve begun to see the adverse effects of the millions unemployed is such a short time frame (Good gracious, millions more are still furloughed and on the chopping block).

The markets may get a boost from the “economy re-opening” and yes, some will go back to work… The question then becomes, how many and in what time frame? Currently estimates we read are roughly 1/3 will go back to work leaving nearly 2/3 out of a job for an extended period of time.

The crux of all of this breaks down to just because the Fed has done what it has, it doesn’t mean this crisis we are in is over? Should they nationalizing everything, as it feels like they are doing right now, it’s a disaster in waiting with a tremendous amount more that can go wrong… AND should they succeed, at what cost will it come?

Many FAANG companies are reaching all-time highs. Google is an advertising firm – they SELL ADVERTISING. Expedia announced this morning they will be slashing their advertising budget by 80% … they will not be the only ones.

We would urge all who are currently in the buy and hold mantra to use this time (up days) as opportunities to re-think your goals and objectives; you may not get many more opportunities to mitigate your risk at current levels?! And should you, you may not want to be “fully invested” watching your life’s work fluctuate by 5-10% on any given day when the chickens come home to roost?!

Global Chief Investment Officer of Guggenheim Partners, Scott Minerd (@ScottMinerd) said it best when he recently tweeted:

“The #Fed has made it clear that it will not tolerate prudent and responsible investing”

As we mentioned in the introduction – Time and Patience are our assets right now … we’re also doing our best to be Prudent at a time when the Federal Reserve is doing everything, they can to make it as difficult as possible.

We’ll continue focus on managing our risk, seek out asymmetrical risk reward set ups, letting our winners run while cutting our losers before they become problematic. We remain firm in our process and discipline.

As always, we’re happy to discuss our market thoughts along with these strategies and more, never hesitate to reach out with any questions or concerns. Thank you for your continued trust and support!

Sincerely,

Mitchel

Mitchel C. Krause

Managing Principal & CCO

We wanted to end it where we did based upon the note getting a bit long in the tooth, however for those of you still reading – please find below our fan favorite section: You just can’t make this sh*t up!

You can’t make this sh*t up…

On March 26th, in an unprecedented Today show interview, which I encourage you to watch by clicking here, Federal Reserve Chairman Jerome Powell spent over 11 minutes showing Savannah Guthrie and the American people his best Fred Astaire impersonation, tap dancing his way into history as one of the greatest fabricators of truth in Federal Reserve President history.

But truly, Powell’s unprecedented 7:00am performance on March 26th takes the cake… Just in time for the first Initial Jobless claims to explode through 3.3 million Americans out of work in a single week Powell stated:

“We may well be in a recession, but again, I would point to the difference between this and normal recession. There is nothing fundamentally wrong with our economy, quite the contrary, the economy performed very well right through February, we’ve got a 50-year low in unemployment for the last couple of years. So, we start in a very strong position. This isn’t something that’s wrong with the economy.”

Planes dive-bombing towers in 2001 weren’t normal either Jay – neither were CDO&CMOs blowing up in 2008 due to lax government policy, irresponsible lending and greedy Wall Street executives that created the largest mortgage crisis in history. The economy wasn’t normal in September when Repo markets required 10’s to 100’s of billions of dollars on an o/n (overnight) basis to function while you stood at your pulpit on September 18th lying through your teeth as you said:

“Funding pressures in money markets were elevated this week, and the effective federal funds rate rose above the top of its target range yesterday. While these issues are important for market functioning and market participants, they have no implications for the economy or the stance of monetary policy”

He continued:

“These temporary operations were effective in relieving funding pressures, and we expect the federal funds rate to move back into the target range.”

These operations were by no means “temporary” nor did they relieve funding pressures as the Fed continued their Repo operations for the last 6 months finally offering up to $1 trillion in o/n repo, in the wake of a virtual implosion of credit markets… Tax Day, temporary, relieved, we’ve got things under control – all BS.

It wasn’t normal in 2017 when $F (Ford) “looked beyond credit scores” to drive revenue, as ratings agencies bypassed downgrading credits like these as miraculous blowout numbers in September 2017 righted all wrongs… Which was the narrative, the reality was the over 700k units generated that month came from replacing those vehicles lost when Hurricane Harvey decimated Louisiana and Texas – which were facts that failed to fix a persistent problem.

It wasn’t normal for companies like $RCL (Royal Caribbean) to spend $2.7 billion over the last 3 years on dividends and buybacks while the airline industry used nearly 96% of their FCF (Free Cash Flow) over the past few years on buybacks, too. As both industries now beg for a bailout citing COVID-19 rather than simply being obnoxiously mismanaged. The $45 billion the airlines industry spent on buybacks would look really good on their balance sheets right now as they lobby for $50 billion from taxpayers (the government) …

Powell also continued to perpetuate another false narrative we’ve been discussing for some time:

“The job market remains strong. The unemployment rate has been near half-century lows for a year and a half, and job gains have remained solid in recent months. The pace of job gains has eased this year, but we had expected some slowing after last year’s strong pace.”

We, along with every other financial mind who has studied economic cycles have argued unemployment at 50-year lows is NOT a positive sign at the end of a business cycle Jay – it’s a sign of danger when the economy has flat to negative earnings (especially when those EPS are manufactured) as businesses will cut FAT Jay … Businesses reduce head count when earnings are flat to negative. But you KNOW THIS – you’re worth $100mm profiting off of excessive leverage. What you’ve done is you’ve SOLD OUT…

The Hubris… He continued:

“What’s happened is investors all over the world have pulled back to LESS RISKY things. That’s understandable. What that’s meant is many places in the capital markets which support borrowing by households and businesses, I’m talking about mortgages and car loans and things like that have just stopped working…”

EARTH TO JAY – when mortgages and car loans “JUST STOP WORKING” because people want to assume LESS risk, the economy is NOT OK… it’s not healthy and it has little to do with a virus. As discussed above, while the VIRUS may be a catalyst (like a plane or CMO that was improperly rated by the ratings agencies) emergency lending powers weren’t needed because of the virus – they were needed because you’ve been feeding too much leverage to hedge funds via sponsored repo (Bank of International settlements pg 23; December 2019 note) among others… It’s because credit quality has deteriorated to sh*t.

You’re NOT bailing industries out because of a virus – you’re bailing them out and backstopping them now because they ran sh*tty balance sheets by excessively borrowing at cheap levels perpetuated by you and your recent predecessors.

Now your balance sheet is about to explode to $10 trillion and you “don’t really see” long-term RISKS of your current actions?!!?!

WHAT HAVE YOU SEEN? You, Bernanke, Yellen – you’re all literally walking around blind while destroying the economy…

What about PENSION PLANS JAY? Our savers JAY?

The first honest thing you have said in years is as follows:

“What I’m really saying is we don’t know. The sooner we get through this period and get the virus under control – the sooner the recovery can come. We don’t have comparable experiences to go back and look at… We know that economic activity will decline, probably substantially in the 2nd quarter, but I think many expect and I would expect the economic activity to resume back up in the second half of the year. Very hard to say precisely when that will be, and it will really depend on the spread of the virus, the virus is going to dictate the timetable here.”

Which means you have no F’ing clue and can NOT speak intelligently to the lasting economic impacts or effects of this situation. You HAVE NO IDEA – NONE. Millions of people without work are millions who are no longer the “resilient consumer” you claim them to be? SHAMEFUL… There is literally ZERO accountability in Washington; from our elected politicians or appointed officials, it’s saddening. 3.3 million out of work last week, 6.6 million out of work this week. how many next week? and the following… We owe it to our children to demand better.

You need to set up SPV to buy all the sh*t credit you created – as you let CEO’s off the hook for reckless behavior while running up a credit card bill taxpayers will NEVER be able to pay off… SCREWING THE AMERICAN PEOPLE AGAIN. AGAIN!!! you’re not a bank – your job isn’t to “Support the flow of credit in the economy… to households and businesses” that’s JP Morgan’s job.

They aren’t lending because millions are out of work and risk of default is HIGH, which happens at the end of every business cycle…

You, Clarida, Yellen, Bernanke were all made for each other. The hubris! Ignorant, arrogant morons.

Shame on Private Equity firms, overleveraged hedge funds and central bankers who extended the credit to these firms to begin with. Shame on those at the Federal Reserve who are bailing out their ilk who went to work for these hedge funds. Shame on pension fund managers for fueling this debt bubble by buying the covenant light crap banker brought to them. Pension fund managers had a choice, they could have been prudent and said no to Wall Street – they could have said no to Private Equity rather than to expose those hard-working Americans who paid into the system based upon the promise of their retirement being prudently taken care of.

Ah – shit. I could go on but so few care anymore… I’m truly disgusted – just pump my stocks… you really can’t make it up.

Appendix A: Federal Reserve ActSection 13(3):

3. Discounts for individuals, partnerships, and corporations

- In unusual and exigent circumstances, the Board of Governors of the Federal Reserve System, by the affirmative vote of not less than five members, may authorize any Federal reserve bank, during such periods as the said board may determine, at rates established in accordance with the provisions of section 14, subdivision (d), of this Act, to discount for any participant in any program or facility with broad-based eligibility, notes, drafts, and bills of exchange when such notes, drafts, and bills of exchange are indorsed or otherwise secured to the satisfaction of the Federal Reserve bank: Provided, That before discounting any such note, draft, or bill of exchange, the Federal reserve bank shall obtain evidence that such participant in any program or facility with broad-based eligibility is unable to secure adequate credit accommodations from other banking institutions. All such discounts for any participant in any program or facility with broad-based eligibility shall be subject to such limitations, restrictions, and regulations as the Board of Governors of the Federal Reserve System may prescribe.

- As soon as is practicable after the date of enactment of this subparagraph, the Board shall establish, by regulation, in consultation with the Secretary of the Treasury, the policies and procedures governing emergency lending under this paragraph. Such policies and procedures shall be designed to ensure that any emergency lending program or facility is for the purpose of providing liquidity to the financial system, and not to aid a failing financial company, and that the security for emergency loans is sufficient to protect taxpayers from losses and that any such program is terminated in a timely and orderly fashion. The policies and procedures established by the Board shall require that a Federal reserve bank assign, consistent with sound risk management practices and to ensure protection for the taxpayer, a lendable value to all collateral for a loan executed by a Federal reserve bank under this paragraph in determining whether the loan is secured satisfactorily for purposes of this paragraph.

- The Board shall establish procedures to prohibit borrowing from programs and facilities by borrowers that are insolvent. Such procedures may include a certification from the chief executive officer (or other authorized officer) of the borrower, at the time the borrower initially borrows under the program or facility (with a duty by the borrower to update the certification if the information in the certification materially changes), that the borrower is not insolvent. A borrower shall be considered insolvent for purposes of this subparagraph, if the borrower is in bankruptcy, resolution under title II of the Dodd-Frank Wall Street Reform and Consumer Protection Act, or any other Federal or State insolvency proceeding.

- A program or facility that is structured to remove assets from the balance sheet of a single and specific company, or that is established for the purpose of assisting a single and specific company avoid bankruptcy, resolution under title II of the Dodd-Frank Wall Street Reform and Consumer Protection Act, or any other Federal or State insolvency proceeding, shall not be considered a program or facility with broad-based eligibility.

- The Board may not establish any program or facility under this paragraph without the prior approval of the Secretary of the Treasury.

- The Board shall provide to the Committee on Banking, Housing, and Urban Affairs of the Senate and the Committee on Financial Services of the House of Representatives–

- not later than 7 days after the Board authorizes any loan or other financial assistance under this paragraph, a report that includes–

- the justification for the exercise of authority to provide such assistance;

- the identity of the recipients of such assistance;

- the date and amount of the assistance, and form in which the assistance was provided; and

- the material terms of the assistance, including–

- (aa) duration;

- (bb) collateral pledged and the value thereof;

- (cc) all interest, fees, and other revenue or items of value to be received in exchange for the assistance;

- (dd) any requirements imposed on the recipient with respect to employee compensation, distribution of dividends, or any other corporate decision in exchange for the assistance; and

- (ee) the expected costs to the taxpayers of such assistance; and

- once every 30 days, with respect to any outstanding loan or other financial assistance under this paragraph, written updates on–

- the value of collateral;

- the amount of interest, fees, and other revenue or items of value received in exchange for the assistance; and

- the expected or final cost to the taxpayers of such assistance.

- not later than 7 days after the Board authorizes any loan or other financial assistance under this paragraph, a report that includes–

- The information required to be submitted to Congress under subparagraph (C) related to–

- the identity of the participants in an emergency lending program or facility commenced under this paragraph;

- the amounts borrowed by each participant in any such program or facility;

- identifying details concerning the assets or collateral held by, under, or in connection with such a program or facility,

shall be kept confidential, upon the written request of the Chairman of the Board, in which case such information shall be made available only to the Chairpersons or Ranking Members of the Committees described in subparagraph (C).

- If an entity to which a Federal reserve bank has provided a loan under this paragraph becomes a covered financial company, as defined in section 201 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, at any time while such loan is outstanding, and the Federal reserve bank incurs a realized net loss on the loan, then the Federal reserve bank shall have a claim equal to the amount of the net realized loss against the covered entity, with the same priority as an obligation to the Secretary of the Treasury under section 210(b) of the Dodd-Frank Wall Street Reform and Consumer Protection Act.

[12 USC 343. As added by act of July 21, 1932 (47 Stat. 715); and amended by acts of Aug. 23, 1935 (49 Stat. 714); Dec. 19, 1991 (105 Stat. 2386); and July 21, 2010 (124 Stat. 2113). As enacted by Public Law 111-203 (124. Stat. 2115), “any reference in any provision of Federal law to the third undesignated paragraph of section 13 of the Federal Reserve Act [FRA] (12 USC 343) shall be deemed to be a reference to section 13(3) of the FRA.”]

SEC. 4003 EMERGENCY RELIEF AND TAXPAYER PROTECTIONS

(a) In General.—Notwithstanding any other provision of law, to provide liquidity to eligible businesses, States, and municipalities related to losses incurred as a result of coronavirus, the Secretary is authorized to make loans, loan guarantees, and other investments in support of eligible businesses, States, and municipalities that do not, in the aggregate, exceed $500,000,000,000 and provide the subsidy amounts necessary for such loans, loan guarantees, and other investments in accordance with the provisions of the Federal Credit Reform Act of 1990 (2 U.S.C. 661 et seq.).

(b) Loans, Loan Guarantees, And Other Investments.—Loans, loan guarantees, and other investments made pursuant to subsection (a) shall be made available as follows:

(1) Not more than $25,000,000,000 shall be available to make loans and loan guarantees for passenger air carriers, eligible businesses that are certified under part 145 of title 14, Code of Federal Regulations, and approved to perform inspection, repair, replace, or overhaul services, and ticket agents (as defined in section 40102 of title 49, United States Code).

(2) Not more than $4,000,000,000 shall be available to make loans and loan guarantees for cargo air carriers.

(3) Not more than $17,000,000,000 shall be available to make loans and loan guarantees for businesses critical to maintaining national security.

(4) Not more than the sum of $454,000,000,000 and any amounts available under paragraphs (1), (2), and (3) that are not used as provided under those paragraphs shall be available to make loans and loan guarantees to, and other investments in, programs or facilities established by the Board of Governors of the Federal Reserve System for the purpose of providing liquidity to the financial system that supports lending to eligible businesses, States, or municipalities by—

(A) purchasing obligations or other interests directly from issuers of such obligations or other interests;

(B) purchasing obligations or other interests in secondary markets or otherwise; or

(C) making loans, including loans or other advances secured by collateral.

(c) Terms And Conditions.—

(B) FEDERAL RESERVE ACT TAXPAYER PROTECTIONS AND OTHER REQUIREMENTS APPLY.—For the avoidance of doubt, any applicable requirements under section 13(3) of the Federal Reserve Act (12 U.S.C. 343(3)), including requirements relating to loan collateralization, taxpayer protection, and borrower solvency, shall apply with respect to any program or facility described in subsection (b)(4).

Please click here for all disclosures.