In This Article

“The ancient Egyptians understood time as a series of repetitive cycles, instead of something linear” ~Joobin Bekhrad, December 4, 2017

Ouroboros …

… is commonly defined as:

“a circular symbol depicting a snake, or less commonly a dragon, swallowing its tail, as an emblem of wholeness or infinity.”

While the first known ouroboros was found on a “golden shrine” in the Egyptian tomb of King Tutankhamen (King Tut) in 13 BC, the term ouroboros is actually Greek at its origin … directly translating to “tail devourer”.

This symbol has been depicted and contextualized slightly differently over many cultures and geographies throughout the centuries, though, regardless of region the serpent (or dragon) portrayed as perpetually feeding on itself has little to do with it cannibalizing itself, but much more to do with the concepts of unity and cycles. In fact, in some cultures, it was emblematic of THE ETERNAL CYCLE … from destruction to re-creation.

Well renowned Egyptologist, Jan Assman has stated, the symbol, “refers to the mystery of cyclical time, which flows back into itself.”

Similarly, to how we come to expect a change in weather with the passing of each season, ancient Egyptians viewed time through the lens of constant cycles, such as “the flooding of the Nile” river or the “journey of the sun”.

For the Greeks, the symbol of the ouroboros is known as the “oldest allegorical symbol in alchemy”, it represents “eternity, as well as the unity of time’s beginning and end.”

The history of and meaning behind this symbol is truly fascinating, though at this point, the question on most of your minds is very likely, how am I going to tie the emblematic symbolism of the ouroboros to investing/economics.

I’m often asked, what my greatest challenge in writing these notes are?! At this point, my reply is near etched in stone … thinking of creative analogies and ways to keep readers engaged while often describing the same thing over the life of a full economic investing cycle, which often take time to play out.

Earlier this month, Hedgeye financial sector head and macro team member, Josh Steiner quoted his teammate, Christian Drake echoing the same sentiment:

“At a certain point, it’s hard to find new ways to say the same thing” Hedgeye’s Josh Steiner quoting Christian Drake on The Call, 4/6/2023.

Ironically, it was a different thought from Steiner on that April 6th call that triggered our ouroboros introduction …

“Bank lending conditions are causal and reflexive, and they feed forward on themselves … so as they tighten conditions, economic activity slows … slowing economic activity drives non-performing rates (both consumer and commercial) higher … that causes banks to further tighten and contract activity and so on and so forth… UNTIL … you get the circuit breaker, which is the Central Bank, doing a full 180” Josh Steiner, The Call; 4/6/2023

Long time readers have often heard us state that, “IT’S ALL CONNECTED” … describing the dynamic of specific events progressively flowing into each other as a waterfall or cascading affect; for each subsequent event “cascades” or crashes into another and then another; each cascade generating a series of knock-on effects.

A simple example of this would be something we’ve been noting since April of 2022, “As margins compress – profits fall – layoffs are around the corner” … each event progressively knocks into the other; similar to dominoes falling into each other, one by one.

The importance in distinction between our previous waterfall/cascade analogy vs. that of the ouroboros or reflexive loop that Steiner referenced is significant, for with the later example, each subsequent knock-on effect spirals into the other making things worse with each progressive loop; just as the serpent continually eats its tail until it’s dead … so, if we took our simple example from above a bit further:

“As margins compress – profits fall – layoffs are around the corner” … the unemployed spend less – corporate profits continue to fall – margins further compress – more employees are let go! (we’ll discuss this concept and Steiner’s “UNTIL” throughout the piece).

Steiner’s “UNTIL” is extremely important as the banking sector is what drives growth, “UNTIL … you get the circuit breaker, which is the Central Bank, doing a full 180,” which then, ultimately becomes the “rebirth”.

Which begs the question … how alike is our cycle to the death and rebirth of the ouroboros?!

Should markets crack under the stress of an unsustainable debt load given current interest rate/and unsustainable cost of capital, the multi-trillion-dollar question becomes, to what degree do markets resemble their former selves?!

Does the Fed attempt to recreate the economic investing culture of the last two decades that got us into this mess or restore sanity back to investing?

Does it re-emerge from its destruction in similar fashion to its modern self or does the Fed have the ability and resolve, as we discussed last month, to kill the “Fed put” and wild speculation, in an effort to create a more stable economic environment.

In this month’s note we’ll discuss and expand upon these reflexive loops as they fit within the context of the current economic cycle.

The buck stops here

In August of 2022 we reminded you about something we wrote in 2Q2017 … that being, “the primary fuel, which makes our economy function”… as a reminder, we wrote:

The Credit/Debt dynamic is without question, THE PRIMARY driving force behind our economy; without credit, the vast majority of American consumers wouldn’t be able to spend a fraction of what they do … This dynamic is the lighter fluid on the U.S economy’s campfire.

Banks/lenders offer consumers “credit” to buy their home; the consumer assumes “debt” in the form of a mortgage. Without this dynamic, the housing markets freeze, as we witnessed in 2008/09. While outstanding mortgages dwarf other segments of “consumer credit” markets, i.e. Auto loans, Student loans and Credit Cards, these markets are what allows the vast majority of our country to spend any discretionary money at all. Most individuals in the United States do not have the ability to outright purchase any large ticket items without first, being approved to assume a significant DEBT before the “credit” is extended to them.

Without the credit/debt dynamic, discretionary spending grinds to a halt as individuals focus more of their attention to buying necessities: food, heat, electricity, and a roof over their heads and less on more expensive cars, vacations, casual dining, clothing, etc.”

Does any of this sound pertinent given today’s economic environment?!

While the above was written nearly 5 years ago, it echoes just about everything we’ve described over the last year … the below being a quick example written in May of 2022:

“The consumer is shifting their purchases from wants to needs … in a BIG WAY … these products often have smaller margins.”

Just as our opening quote describes the Ancient Egyptians view of the ouroboros, they, “understood time as a series of repetitive cycles, instead of something linear” … if cycles didn’t have a specific rhythm, cadence or flow to them, the concepts behind our words from previous cycles wouldn’t stand the proverbial “test of time”.

This all hits at the very CORE of Steiner’s quote describing the reflexive loop feeding on itself!

As we detailed back in August of 2022 and quarterly thereafter via the Federal Reserve’s Senior Loan Officer survey, there isn’t a financial institution that hasn’t been pulling back on/tightening lending standards (SHOULD YOU FIND THE ONE THAT ISN’T … SHORT IT WITH IMPUNITY).

Financial institutions have been tightening credit/lending standards for nearly a year now … AND THAT WAS BEFORE THE SECOND AND THIRD LARGEST BANK FAILURES EVER!

While the most recent senior loan officer survey isn’t due to be released for another few weeks, we still have the ability to get a glimpse into the post $SNBY/$SIVB bank failure world via a slightly less known regional Federal Reserve survey; that being the Dallas Fed banking conditions survey.

Admittedly, I was unfamiliar with this survey until Hedgeye’s Josh Steiner brought it to subscriber’s attention on that April 6th morning call. There are some definite pros and cons to this survey, for instance, because it’s a regional survey it consists solely of the Fed’s 11th district; data is compiled from Texas, northern Louisiana, and southern New Mexico … making it a smaller survey.

At the same time, data is gathered and released twice per quarter, and while the survey has only been around since 2017, when overlapped with the larger, more broad information from the Fed’s Senior Loan Officer Survey, the data often matches up quite well … making it a fairly good leading indicator.

The brief summary below is literally the opening paragraph from the most recent survey; with data being collected from March 21 through the 29th. So, what did it say?

Loan demand falls and outlooks worsen

Loan demand declined for the fifth period in a row as bankers in the March survey reported worsening business activity. Loan volumes fell, driven largely by a sharp contraction in consumer loans. Loan nonperformance increased slightly overall, with the only notable rise over the past six weeks coming from consumer lending. Credit standards and terms continued to tighten sharply, and marked rises in loan pricing were also noted over the reporting period. Banking outlooks continued to deteriorate, with contacts expecting a contraction in loan demand and business activity and an increase in nonperforming loans over the next six months. Some contacts cited waning consumer confidence from recent financial instability as a concern.

A sample of banker’s comments can be found here, but these two sum things up nicely:

- The effects of rising interest rates on balance sheets [are a concern]—as are recent bank failures in the news and the possibility of contagion, the rising debt of the federal government and other possible bank failures internationally.

- Our commercial customers are having sticker shock when their three- or five-year rate adjustments are coming due. Pricing for good commercial loans is getting very competitive.

While we acknowledge this to be a microcosm of a much larger economy, it has been one that’s proven to be an extremely solid barometer of things to come across the entire financial space … which continues to echo what we’ve been saying for multiple quarters right now:

Both the consumer and small business are being squeezed like no other time in modern history … which constitute the backbone of our country.

The Consumer…

… IS the economy, as we reminded you last month, private consumption, which includes “all purchases made by consumers, such as food, housing (rents), energy, clothing, health, leisure, education, communication, transport as well as hotels and restaurant services,” was nearly 70% of GDP in 2022.

We’ve unfortunately been underscoring the trending deterioration of the U.S. consumer for nearly a year as inflation continues to crush the majority of Americans it becomes clearer with each passing data point released … so let’s talk data!

Shortly after publishing our March note, the Michigan Consumer Confidence survey revealed yet another massive deceleration, as it collapsed 7.5% MoM, dropping 5 points from February’s print of 67.0 to 62.0 in March.

More importantly, in the spirit of “looking ahead” … the “expectations” component of the report dropped 5.5 points from February’s 64.7 to 59.2 … which amounted to an 8.5% deceleration!

This weakness in confidence manifests in what the consumer is a. actually willing to SPEND and/or b. has the ability to spend … and the data shows the “strong” consumer narrative wall street keeps parroting, isn’t spending much of anything on things outside of necessities anymore.

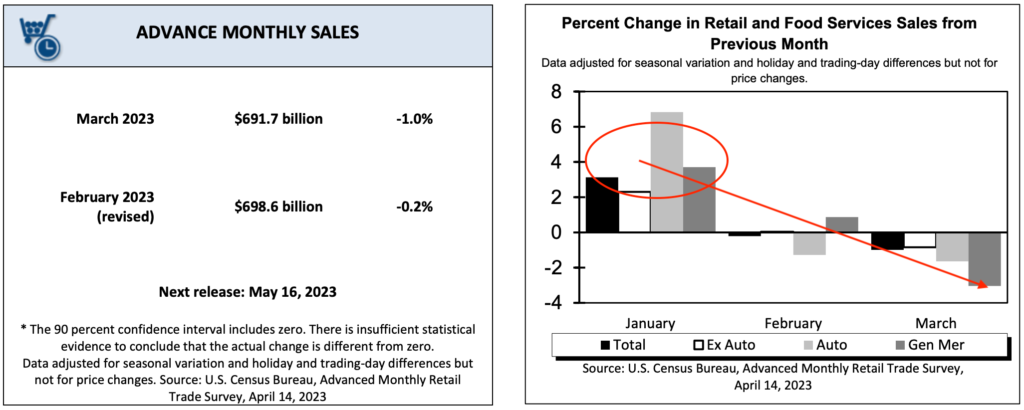

While some on wall street were quick to point to the 3.7% YoY acceleration in U.S. Redbook Weekly Retail Sales vs. its prior week of +2.8% to close out March, we believe following our process to be paramount. In doing so, it was important to recognize that this particular acceleration came on the heels of a previous CYCLE LOW in this particular data series.

With patience being at the core of our process, as to remove any knee jerk emotional reaction, subsequent Redbook Retail sales readings throughout April showed the data resuming their downward spiral, crumbling to NEW sequential cycle lows of +1.5% YoY and +1.1% YoY respectively; (remember, a bounce does NOT a trend make) and this TREND clearly remains DOWN.

Long time readers know we focus on the ROC (Rate of Change) in data, utilizing Hedgeye’s Trade, Trend and Tail models … we’d suggest readers revisit our January discussion regarding the importance of understanding a short-term trade vs. the longer term trending data.

This data series is important as it often gives us a solid read through to the more broad U.S. Retail sales data which came in weaker than “consensus” anticipated decelerating -1.0% MoM.

As we discuss “the consumer”, it’s important to include small businesses in the discussion as nearly 99% of businesses in the U.S. are considered “small businesses”. And depending on whose data you trust, these businesses employ between 45 to 55% of all employees and account for roughly 45% of GDP (down from 50% roughly a decade ago) … and again, private consumption (the consumer) comprises nearly 70% of GDP.

So, when the NFIB Small Business Index reaches its lowest level since the GFC, and is currently in its 15th consecutive month BELOW its 49-year average of 98, as Hedgeye Director of research Daryl Jones noted earlier this month when March’s NFIB data fell by 0.8 points to 90.1 … it should speak volumes to anyone paying attention (a weak consumer and small business with no confidence bleed into the directionality of GDP).

And if you don’t think the data is showing up in the real world, discretionary spending at Costco decelerated by roughly -5.00% from February to March as consumers spend on what they NEED vs. want.

Talk about the ouroboros eating its own tail … without the consumer spending the economy is destined to shrink; when you remove their access to cheap capital and lifelines to credit … their confidence erodes (they without question spend less)!

When Americans lose their jobs, most will change their spending habits immediately (obviously spending less). Individuals watching friends and colleagues getting fired has a similar affect, as many often become fearful of suffering the same fate, thus, putting further pressure on corporate margins.

As the corporate earnings recession gets deeper, these businesses will cut more costs which ultimately equates to firing more employees … talk about the ouroboros eating its own tail, it’s all just one big reflexive loop! Which brings us to how it’s presenting in the:

Real economy

The lack of strength in the consumer not only evident in their lack of confidence or a deceleration in retail sales … it’s apparent throughout the “goods economy” which is driven by the consumer.

For as the retail sales data decelerates from the consumer slowing their purchases of discretionary goods … companies begin to order less merchandise/inventory, which then shows up in the industrial production and ISM Manufacturing data, which bombed in March, decelerating from 47.7 in February to a new cycle low of 46.3; collapsing 10.3 points from 57 on a YoY basis; its 5th consecutive contractionary print (below 50).

NEW ORDERS dropped 2.7 points from 47 in February to 44.3 in March, which makes sense when fewer items are being purchased … this metric is troubling as it’s typically foreshadowing a continuous downward spiral.

Markit Manufacturing PMI for March did accelerate to 49.2 vs February’s 47.3, but again: 49.2 remains CONTRACTIONARY and weakness in “New orders” confirms what we’re seeing in the ISM data.

Adding insult to injury, U.S. February Factory orders continues to communicate economic deterioration, coming in below consensus at -0.7% with January being revised lower to -2.1%, too. We’re now staring at a very noteworthy 3 months of decelerations out of the last 4…

For those who continue to suggest that both the consumer and services side of the economy remains strong, we’d again point you to the data, for that’s not what it’s suggesting …

As the ISM Services Index also saw a significant deceleration in March, cratering to 51.2, vs. February’s reading of 55.1.

It shouldn’t be a stretch to understand how weak the economy is when both manufacturing and services are contracting at this pace. Additionally, you also shouldn’t need a PhD to project into the future when the largest driver of the economy (the CONSUMER), is being squeezed by a combination of higher cost of capital (borrowing rates), less availability to credit and crippling inflation in everything that matters to them, among a host of other reasons.

Again, it’s a reflexive loop … and it should be troubling to more than just the handful of us trying to warn investors of what lies ahead. As we wrote in our 3Q2020 note, “The surface area of the sinkhole is literally the last domino to fall.” … “equities” represent the surface area of markets.

To summarize where we are at this point, we know Liquidity is decelerating on a trending basis, as is Confidence which is adversely affecting the “Goods Economy” via Retail Sales, Manufacturing and CapEx … we also know that New Orders are slowing and the “Services” side of the economy is cratering, too.

Unfortunately, we’re entering the stage where the ouroboros begins to eat itself at a faster pace!

With this in mind, we’ve presented and backed all of the above with the data! Now let’s briefly discuss the two primary metrics that the FOMC uses which dictates their policy, Labor and Inflation, and how they fit into the cycle?!

Labor & Inflation

As we’ve noted in the past, the FOMC is backward looking as they consistently rely on stale metrics to drive their interest rate policy decisions. On the surface, from a historic point of view, current labor data remains “firm” … however, as we’ve been noting for some time, the incremental softening continues.

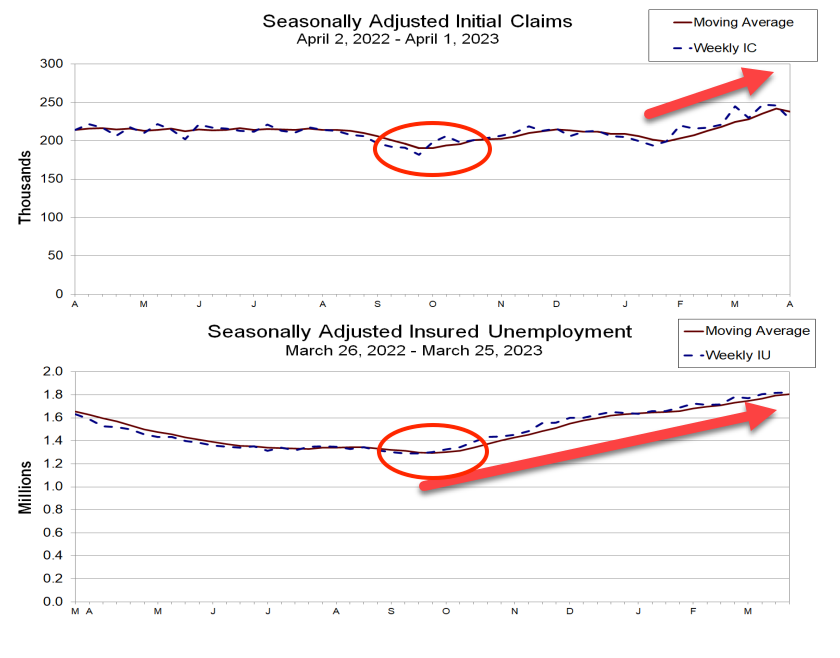

While weekly jobless claims admittedly remain near all-time lows, with April 1st’s +228k being a slight deceleration from March 25th’s 246k; claims from April 8th & 15th have both sequential accelerated up +240k & +245k respectively; with April 15th’s +245k representing a 35% increase from September 24th’s + 182k cycle low.

Ironically, Continuing Claims bottomed at 1.289MM, a mere few weeks prior on September 10th, 2022, and while the most recent claims report also remains historically low at 1.823MM … accelerating a stealth 41% from September’s trough to current times (more job losses + more continued claims = no bueno)!

Hedgeye’s Josh Steiner recently tweeted a chart providing a visualization of the dynamic described above, with a similar observation, “It’s easy to miss because it’s still nominal/unremarkable, but the early signs of a trend are apparent in the claims data.”

Though, as both history teaches us, and Hedgeye CEO Keith McCollough often reminds us … “RISK happens slowly, then all at once!”

Additionally, March’s ADP Employment report decelerated to its second lowest print in the last year coming in at +145K vs. +261K … per the release:

“Our March payroll data is one of several signals that the economy is slowing,” said Nela Richardson, chief economist, ADP. “Employers are pulling back from a year of strong hiring and pay growth, after a three-month plateau, is inching down.”

All of this data echoes the NFIB small business report we discussed earlier, as owners expecting business conditions to improve in the next 6 months registered a net negative -47%

Moreover, as we’ve been noting since January, data out of Challenger, Grey & Christmas again, revealed job CUTS ACCELERATING to +89.7K in March, which is up roughly 15% MoM … nearly a 320% increase on a YoY basis!

If you really want to get super granular with the Labor data, take an hour and listen to economist David Rosenberg during the very recent Hedgeye Investors Summit … the next few points I’ll be crudely paraphrasing Rosenberg, so credit to him:

- Rosey (as he’s known in the industry) notes that in “half of the cycles leading back to 1950, employment is still rising into the early months of the recession.” … to the point we’ve been making for over a year, labor is the latest of late cycle indicators.

- His deeper dive into the employment data shows that “goods producing” employment was down, while the services side of the report was up. He flags this as “yet another late cycle indicator” and an “important divergence” … “for the services side of the market literally “services” the goods producers … who are now cutting”.

- “The labor market is a very complex beast, and you can’t look at it just with bodies … you have to take a look at it also with respect to the hours that the bodies are putting in” Economist David Rosenberg minute ~ 39:10 Hedgeye Investing Summit

Which leads us to:

- Companies reduce “hours worked” before they lay people off; and based upon the “Index of aggregate hours worked”, total labor input into the economy has been -0.1 two months in a row and while that might not sound like much, when considering 150MM workforce army … payrolls, when adjusted for hours worked, have been negative -140k.

Finally, the February JOLTS (Job Openings & Labor Turnover Survey) data declined by roughly -5% MoM to 9.93MM Job Openings, we initially highlighted this metric for our current economic cycle last May, shortly after they peaked at 11.85MM in March. This data continues to suggest that there are fewer and fewer job openings; hiring is quickly being replaced with layoffs!

The labor force is without question, contracting … as the loop continues to spiral, it should be clear to all of our readers that very few individuals in this business utilize a forward looking macro-economic process let alone an accurate/reliable one; this includes the CEOs of the largest companies in the world.

As we wrote last month:

While CEO’s, much like the Lorax’s Once-ler, are focused on biggering and Biggering, and BIGGERING, selling nothing but a trajectory for growth, it’s as if they outright refuse to conceive what happens after the last tree has been chopped! They are blind to the cycle and the small, incremental changes in data or the “particulars” as Hedgeye CEO Keith McCollough often says.

$META, $AMZN, $DIS, $DOCU, $EA, $IBM, $MSFT, and on … have all announced multiple layers of layoffs over the past 9 months … the first is most often never the last and the list is massive, growing daily.

Sadly, the reality is that in the minds of these CEOs, it would stand to reason that they would have been hiring while we were suggesting to proactively prepare for a massive downturn! That’s why cycles typically unfold as they do … because so few ever consider the thought that the music will eventually stop.

As a quick aside, speaking of those with a poor or no macro process … in our November 2022 “Final thoughts” we wrote:

As we’ve stated for nearly a year, GDP will first crater from 7 to 2, then to zero and eventually it will trough in outright negative territory. This, as we head deeper into a U.S. corporate profit recession. This will force even more U.S. based businesses to expand their cost cutting efforts (layoffs) even more than they originally believed they’d have to, creating a self-feeding downward spiral.

However, even with GDP and inflation falling, and layoffs rising … there will still be no data points directly tied to the Fed’s mandates that will be anywhere near a level which would trigger any meaningful bailout large enough to thwart off this U.S. corporate earnings recession.

The Atlanta Fed literally just cut their most recent GDP forecast by more than 50% the day before GDP is released … we’re not lying when we tell you these people have ZERO forward outlook?! Our wager is they got the report and cut their numbers just enough as to not look like complete fools when the data is reported.

The only way we’ve been able to map out the most probable economic outcomes with the accuracy that we have has been by integrating a sound macro approach into our investment thesis, following a repeatable process and MOST importantly, utilizing the services of Hedgeye … FULL STOP!

There is no question our economy and markets would all be in a better place if more corporate CEOs did as well … reality suggests they don’t … which just accelerates the layoff cycle and the ROC (Rate of Change) in which Americans will pull back on spending, further perpetuating this downward reflexive loop! Though I digress…

When discussing the Fed’s inflation metrics, as we alluded to in our November note … be it CPI, core CPI or PCE, none of these data points will provide the Fed with a natural pivot point in the near future.

We’ve been extremely repetitive over the year in reminding you that the Federal Reserve’s inflation “target” is 2% … why?! because Fed Chairman Powell has been emphatic about it … most recently at his March 22nd press conference:

“Inflation remains too high, and the labor market continues to be very tight. My colleagues and I understand the hardship that high inflation is causing, and we remain strongly committed to bringing inflation back down to our 2 percent goal.” Jerome Powell 3/22/23

Powell literally concluded the press conference stating: “rate cuts are NOT in our base case, … so that’s all I have to say!”

Along these lines, we’ve been explaining to readers for some time that based upon how the CPI is calculated, given the lead/lags in data inputs, 2% is mathematically impossible without an outright collapse in all things.

Earlier this month, headline CPI decelerated to +0.1% MoM for March, versus +0.4% in February; and +5.0% vs. +6.0% YoY for March and February respectively! Core CPI (less food and energy) mildly decelerated to +0.4%, vs +0.5% MoM, though accelerated to +5.6% YoY in March, vs. +5.5% in February.

And herein lies the problem …

The largest negative inputs to this most recent data print were gasoline at -17.4%, energy related commodities at -17.0%, fuel oil at -14.2%, and used cars coming in at -11.2%.

We know that the largest component of the CPI market basket is shelter … with a weighting of 33%; energy (and its related inputs) run a close second. As a reminder, the shelter component flows into the data on a 12–15-month lead/lag so even though it topped out in July 2021 … it remained elevated for nearly 9 months before it meaningfully deteriorated … so, while the shelter component appears to be rolling over … there is still some time left on the clock for it to remain a positive contributor to the data series.

With OPEC nations feeling the pain from a mid $60’s oil price, they unexpectedly announced a production cut of 500k barrels per day on April 2nd sending prices higher (into the low $80s/high $70s).

Can anyone tell us what happens to CPI when the second largest contributor and primary negative input turns positive?! As we wrote within minutes of the most recent CPI data being released on April 12th … it equals a #reacceleration … and we haven’t even discussed the Manheim used car data recently reaccelerating, which also increased the odds of our next CPI print being hotter than expected … right before the next FOMC meeting.

So, while February PCE data also decelerated to +0.3%, vs +0.6% on a MoM basis, and to +5.0%, from +5.3% YoY, it is clear that inflation is slowing, but at the same time … 5% is still 150% higher than the Fed’s 2% inflation mandate, which more than likely won’t stop the Fed from raising rates.

The Fed does NOT look at the RoC (Rate of Change) in the data, they look at levels … it’s the reason we were able to tell you inflation was peaking in January of 2022 the same time markets saw it, while it took the Fed until July.

The sad reality is that the current pace of disinflation/deflation doesn’t stop this reflexive loop … if anything, as we’ve described above, given how the Fed reads the data it likely re-enforces their decision to continue to raise rates.

There are only two things that we currently see as catalysts to shift the Fed’s trajectory, which we’ll conclude with … though we caution … neither of which are bullish! But before we do, we like to quickly revisit one of the proverbial bombs that continues to implode with each passing day.

Odds & ends

Everything we’ve discussed feeds on itself … as we said earlier … it’s ALL CONNECTED!

The Fed tightening into an economic slowdown, sucking liquidity out of the system at an unprecedented pace is forcing asset managers to de-leverage and sell into markets with limited to no liquidity … it’s literally collapsing the commercial real estate markets in real time. It’s the very reason asset management firms like Blackstone gated their private REIT (BREIT) as we’ve written at length about since January.

There is not a single thing Blackstone management could say which would change our opinion that they are misleading investors about the true value of their fund. Real world examples of the collapse in commercial real estate are popping up everywhere … eventually they won’t be able to hide it!

Most recently, the once coveted Century Plaza in Los Angeles was just acquired by David and Simon Reuben from Michael Rosenfeld for a bid of $1 billion dollars. While that might seem like a lot of money, (a.) they were the ONLY bidder and (b.) $1 billion dollars is a 40% DISCOUNT to the $2.5 billion dollar development cost.

Nobody ever wants to hear that they’re the only bidder … on anything … but it’s happening more regularly in commercial real estate. Those who care to read an excellent article on BREIT, please click here. It was shared with us by our friend David Auerbach @DailyREITBeat at @armadaetfs … These markets are getting less liquid by the day and as more people need to get out, less will be able to.

On the multi-family side of things, the volume of apartment buildings sold in 1Q2023 was down 74% YoY which registered the largest drop in 14 years … this pushed prices down roughly 13% through February from their July 2022 peak.

With both prices and volumes down on the apartment side there’s roughly 500k units scheduled to come to market this year … which is the largest volume in supply added to the market in 40 years … in this elevated cost of capital environment … with regional banks being the number 2 provider of capital for multifamily loans (second only to government agency backed lending as they reduce), how do you think this will work out for this market?!

The commercial real estate market is a $20-25 TRILLION dollars … I’m sure it’ll be fine (sigh … palm meet forehead)!

It’s important to reiterate, as asset prices in multiple markets are pushed lower, financial institutions will continue to tighten lending standards while simultaneously pulling back on credit availability … sucking the life out of an already crippled U.S consumer who desperately NEEDS the money.

In turn, consumers are losing confidence as they watch both, their savings and purchasing power erode with credit lifelines either capped or pulled and credit card rates skyrocketing … eclipsing 20% across ALL accounts and in many cases, higher.

RECORD interest is now being paid on RECORD amounts of debt (as we’ve been highlighting for nearly a year, first in April 2022, then May 2022 and most recently January of 2023):

“Remember how we told you the explosion in credit wasn’t a good thing in both Apriland here in May?!

… the last two months have literally hocky sticked (re: consumer credit) to SEQUENTIAL Month over Month ALL-TIME HIGHS” …

At that time we noted:

… the national rate on credit cards is nearly 16.58% and climbing, lower credit scores borrow north of 25%, which means borrowers tend to tap their credit cards only as a measure of LAST RESORT”

Why wasn’t it a good thing?! Because on top of everything we’ve already discussed, the consumer doesn’t have the ability to de-lever in this environment, they NEED MORE to just survive. Nevertheless, this will spiral us straight into record defaults on ballooned credit card debt, which will accelerate as layoffs do.

Businesses are watching this unfold as internally, their margins collapse given higher input costs and a consumer spending less, sending their confidence into the sewer … this ultimately leads to those accelerated layoffs … and while inflation is falling, it’s not doing so a. quickly enough to change or alter the Fed’s policy or b. to a level where the consumer needs it to be.

The serpent keeps feeding

As we discussed earlier (again, detailing since August 2022), financial institutions have been tightening lending standards for some time … and with every passing day, the serpent continues to feed on itself, which leads us back to the two scenarios we can think of that could get the Fed to pause their interest rate hikes!

The first is more devious but a very real scenario.

That being … given the recent turmoil in regional banks, the banks themselves tighten credit and pull back on lending so much, that it does the Federal Reserve’s job for them. Powell was very direct with this answer at the Fed’s most recent press conference:

“the events of the last two weeks are likely to result in some tightening credit conditions for households and businesses and thereby weigh on demand, on the labor market, and on inflation. Such a tightening in financial conditions would work in the same direction as rate tightening.” Chair Powell’s March 22, 2023, press conference pg. 6

“The events of the last two weeks” Powell was speaking of were the 2nd and 3rd largest financial failures EVER.

And as we go to print … we may be staring at another as rumors are swirling that First Republic may be taken into receivership by the Fed/FDIC. While there is the possibility $FRC attempts to raise capital at pennies on the dollar while selling a significant portion of their Held to Maturity (HTM) portfolio given this recent move in treasury yields, touting their loyal depositor base … deposits at $FRC still declined roughly 41% in 1Q2023 inclusive of the $30 billion dollar infusion from a consortium of banks led by $JPM; nearly 58% when excluding that infusion as noted by @Overshoooot

As we described earlier, the Dallas Fed banking conditions survey has already given us a preview into the Fed’s Senior Loan Officer survey … however, this survey will have to be EXTREMELY bad in order for the Fed to pause … as they’ll be staring at a continued hot CPI print (Ahh … what to do??!? What to do?!!?)

If they alter their language, it’s likely to mean lending around the country has come to a screeching halt! Should this occur we’d say (a.) a pause in NOT a cut and (b.) given where interest rates are it changes nothing in terms of easing lending standards and (c.) this would send us further into reflexive loop to hell.

Scenario one is about as far from bullish as it gets as it does nothing to disrupt the reflexive loop Steiner described … if banks tighten harder, faster … the serpent just begins to eat itself at an expedited pace … every segment of the loop we’ve discussed accelerates, sending the economy from recession to a probable depression. (uplifting, I know)

The second thing that could get the Fed to possibly redirect is the functionality of markets outright “breaks” … and asset prices collapsing does not equal “breaking”!

We don’t believe any of us wants to find out how this translates into asset prices?! Given this scenario … no one has the ability to answer our initial question … “to what degree do markets resemble their former selves?!” … with any degree of certainty, either.

How can anyone, with any form of intellectual integrity suggest with certainty what the rebirth of the economy will look like if we don’t know what the final “solution” is?! Clearly, we can guess, but for all those suggesting the Fed will “pivot” … the pivotal question becomes, HOW?!

If the answer continues to be how they “saved” both $SBNY and $SIVB, that didn’t bode well for equity or bond holders of either of these companies. Neither did their initial attempt at saving $FRC. And given current money market yields in the 4.00% to 5.00% range, why would anyone hold a deposit of size at any regional bank offering a yield of 30 basis points on deposits?! So what fixes the current run on deposits?!

At this moment in time, the regional banking structure is broken … if the deposit exodus at regionals moves forward with any resemblance to that of $FRC, investors should be prepared for something that looks the S&L crisis of the 1980’s & 90’s.

If this is the case, consumer, commercial & industrial (CNI) and commercial real estate (CRE) loans will dry up faster than most would believe and untapped credit lines will be likely be closed … which as we learned throughout this piece, just further accelerates this reflexive loop.

Final thoughts

“This is an Economy that’s driven by credit” Economist David Rosenberg 4/20/2023 Hedgeye Investing Summit

It may sound crazy, but it is our belief the Fed wants a collapse in asset prices … a controlled demolition if you will. Powell is attempting to kill the “Fed put” … he’s trying to break the cycle of the Fed coming to the markets rescue with every subsequent “emergency” … killing inflation is his cover.

They’ve already told the world to EXPECT the unemployment rate to rise and that investors should anticipate significant volatility and downward pressure in asset prices … it’s what their “blunt tools” do!

Showing the world, they can ward off bank failures while saving depositors as equity and bond holders are crippled has given them a sense of power (temporary or not) and sent a message to the market that poor behavior will no longer be rewarded?! Whether it was poor behavior or not, they’ll say it was, just as they did with Silicon Valley Bank.

Accelerating bankruptcies just adds another dynamic to this mess. Bed, Bath & Beyond’s ($BBBY) alone will add 360 empty buildings to an already struggling commercial real estate market and over 32,.000 employees to the unemployment line.

Those who look at “levels” (wall street and the Fed) would like you to believe things are contained, but they’re not … just as the Ancient Egyptians understood the concept of non-linearity and cycles in 13 BC … all of the leverage embedded in this everything bubble is all connected.

And while the Fed may ultimately break the inflation cycle, they’re also likely to take many industries whose business models can’t survive in this elevated cost of capital/highly leveraged world down with it!

It’s our opinion the majority of investors as led by traditional wall street models have little idea as to what real pain in their portfolios feels like … only time will tell?!

And if we’re wrong … and the Fed pivots, starts buying assets hand over fist and prints ungodly sums of money, we’ll then pivot accordingly, but this is not our current base case.

In the end, will the ouroboros represent unity?! In our scenario, eternity?! Will it be reborn and if so, in what form?! Again, only time will tell … either way, we’ll remain data dependent and process driven!

Good Investing,

Mitchel C. Krause

Managing Principal & CCO

Please click here for all disclosures.