In This Article

“UNLESS someone like you cares a whole awful lot, nothing is going to get better. It’s not.” The Lorax by Dr. Seuss

UNLESS

Each year at my children’s school, the older kids participate in a “poetry teahouse” where students choose a poem, commits it to memory and recites it while standing before peers, teachers, and parents alike. While the youngers students choose a single, short form poem, the “older” students choose 2, one long form with the second being short.

This year, my oldest daughter decided on The Lorax, by Dr. Suess, for her longer poem … because every 10-year-old decides to put a 72-page, 8 minute read to memory?! #overachiever … though, I digress…

Our typical 25-minute adventures to school are ritually consumed by Hedgeye’s Macro show, though, most recently, a soft, yet constant reciting of this 50-year-old classic has been set to “repeat” over my shoulders for the past month.

Published by Random Housing in 1971, the message of this “whimsical yet powerful” story should be crystal clear … GREED has devastating, destructive and often cascading consequences … be it the environment (in the case of the Lorax), our health, or what’s important for our purposes in this piece, the economy.

In the face of colossal warnings screaming in our faces, a majority will more frequently react emotionally vs. being data driven; and having a firm understanding of both, the cycle, and dynamics at play.

Through colorful and poetic metaphors, The Lorax walks readers through the knock-on effects of the Once-ler’s greed, as his incessant chopping of the beautiful Truffula trees coupled with an overwhelming amount of pollution created by his ever-growing factories, destroys this once thriving ecosystem.

The Once-ler’s greed of “biggering and Biggering and BIGGERING and BIGGERING!! Turning MORE Truffula Trees into Thneed’s which everyone, EVERYONE, EVERYONE needs!” predictably cascaded, adversely affecting:

- “the Brown Bar-ba-loots, who lived happily eating Truffula Fruits” had no more fruit to eat,” while:

- “the poor Swomee-Swans … could no longer sing a note; with so much smog in their throats” and:

- “the Humming-Fish who could no longer hum, for their gills are all gummed Gluppity-Glupp and Schloppity-Schlopp

Dr. Suess uses his Lorax, to foreshadow what would happen to our natural environment UNLESS something changed.

As an aside, if you’ve never read or researched the waterfall effects of the Gray wolf being re-introduced into Yellowstone’s eco-system, you should. The story provides a real-life example of what’s been described as a “trophic cascade through the entire ecosystem” by initially skeptical “experts and scientists” who have been “surprised” by the transformation (imagine that?!)

Today, the wolves of Yellowstone are a quintessential example of how cycles, in this case, “life cycles” … flow.

Turning to our market newsletters, we’ve done our best over the years to help investors understand both, the complexity and fragility of financial markets, and how structural changes have forever altered the path of investing. Moreso, that markets are now primarily driven by regulatory changes and more importantly, the corresponding business cycles, as measured by the data.

And of course, that “cycles take time”.

This month, we’ll again allow the data to speak, sift through the narratives and empower you to make up your mind as to whether or not this market is an investible “bull” (as those who have been consistently wrong for the last year continue to preach or if prudence & patience remain our best assets, by providing proper context to the data?!

It’s never just one thing!

While risk management has always been a cornerstone for us from the onset of running discretionary money, our process continues to evolve. One notable change over the years is that we’ve adopted the Hedgeye mantra that, “it’s never just one thing”, that Global Macro should be contextualized as a whole. More importantly, that there is nothing linear about markets, they are fractal in nature with the “directionality” and RoC (Rate of Change) in the data being most pertinent.

It’s unnerving to think that those who control the fate of Trillions upon TRILLIONS of dollars base monetary policy off of what amounts to be stale headline data of a limited number of metrics given their mandates of “price stability” and “employment”.

Which is why placing context to and understanding to how these metrics are derived allows us, in many cases, understand what the Fed is believes it’s seeing vs. what it actually means and how markets are likely to interpret it over a Hedgeye trending duration … let’s start by looking at price stability (inflation) via CPI!

Most recently, Headline CPI came in +6.0% YoY, which was in-line with consensus “expectations”, however, given all the “tightening” of monetary policy, CORE CPI actually ACCELERATED +0.5% MoM; +5.5% YoY … driven by Shelter, coming in +8.1% YoY.

As we noted last month, there was a single “drag” in the data: “With the exception of the “used car” component … ALL major sub-categories of the CPI were UP on a Year over Year basis.”

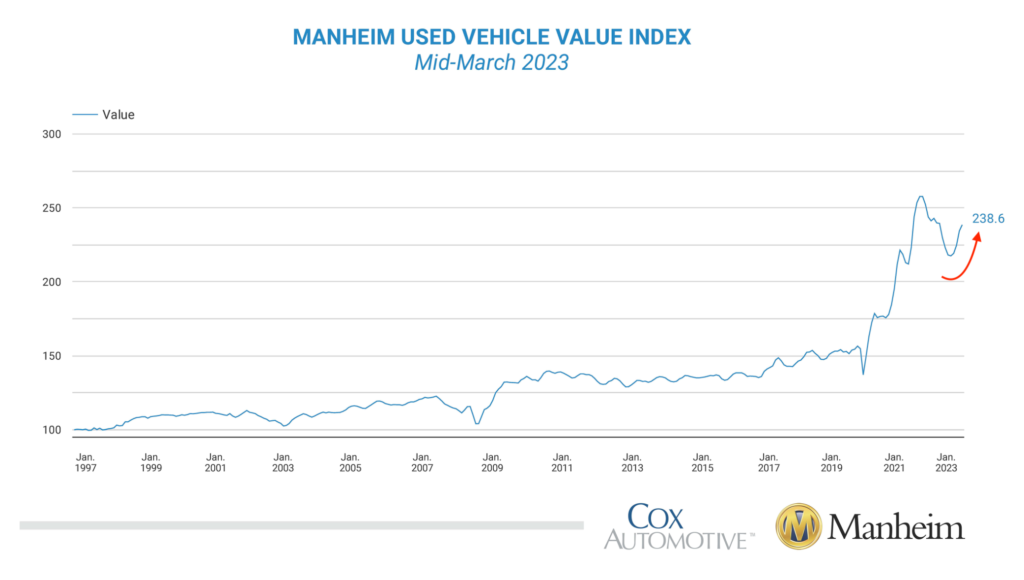

And very little changed in this month’s CPI report. Used Vehicles were the only notable deceleration, decelerating from -11.9% YoY to -13.6% YoY.

Ironically, the latest Manheim Used Vehicle index ACCELERATED, up +4.3% MoM in February, its fastest pace in over decade (2009) … which is where context comes into play.

We’ve tried to explain the dynamics of lead/lags in CPI data for nearly a year. For the Fed’s policy is based on headline data, whereas long time readers may recall that an input like Shelter is typically seen in the data on a 12–15-month lead/lag; talk about late to the party!

As we noted in June of 2022, reiterating in out December 2022 note:

“while housing data, as measured by the Case Shiller National Home Price Index peaked last July/August, history suggests a 12/15-month lead lag before that data shows up in the CPI report; meaning there is still a very high likelihood that the “SHELTER” component of the CPI (representing 33% of the overall index) will continue to provide upward pressure on the primary data point the Fed uses to base its interest rate policy off of.”

We continued to discuss this dynamic in our 3Q2022 note:

Having peaked July/August of 2021, and given a 12-to-15-month lead/lag, that would then have the data rolling over around now … Unfortunately, as we’ve also noted in the past, the housing market remained at obnoxiously elevated levels for nearly 9 months before it started to crash; meaning … the shelter component of CPI could/should remain historically elevated for another 5-7 months before it becomes a net negative … the Food component isn’t likely to lighten up much any time soon either.

If you do the math, our 3Q2022 note was published October 28th; making late March 2023 5-months later, while late May/early June of 2023 would be 7-months; so, in the coming months, while the SHELTER component of CPI will finally show a significant deceleration, this will be offset by Used Vehicles via Manheim reporting their fastest acceleration in over a decade.

While a notable deceleration in CPI over the next few months is most probable, it is likely to remain persistently high courtesy of how the data flows through into the numbers, keeping the Federal Reserve engaged in their rate hiking cycle … again, context is critical … the markets aggregate all of the current data, not a stale headline.

It’s important to remember the Fed’s inflation focus, is CORE CPI, which as noted above, “ACCELERATED +0.5% MoM; +5.5% YoY”; CORE CPI excludes both food and energy … which makes it a perfect measure of inflation since no one eats, heats their homes, cooks, or fuels their cars (insert eyeroll here).

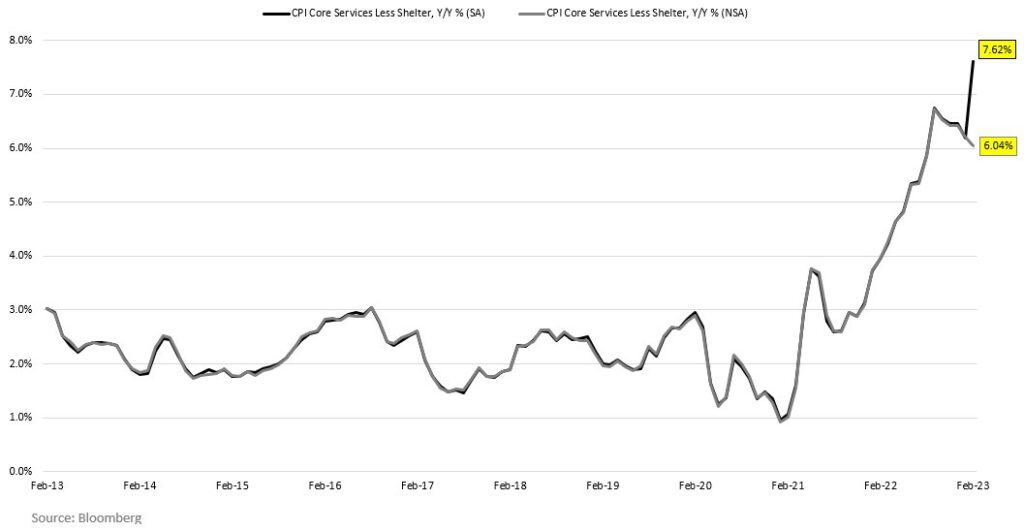

When you actually take a look at how inflation is affecting all Americans, the more pertinent measure of Inflation should be the Consumer Price Basket, which INCLUDES those items the consumer actually needs most; Shelter, Medical Care, Food at Home, Utilities and Wireless Services (representing 53% of the total CPI weighting) … this basket remains elevated at 7.62% YoY growth as recently detailed by Hedgeye’s Christian Drake @HedgeyeUSA

This is NOT good.

Labor

The second focus for the Fed is employment, a dynamic we’ve been discussing for nearly a year now … being very clear from early on:

“They (the FOMC) are backwards looking – they don’t understand labor is as late cycle as it gets… As margins compress – profits fall – layoffs are around the corner – these (expletive deleted) will be tightening into one of the largest slowdowns in history” OSAM 4/1/22

Let’s look at the data:

- Are margins compressing?! →Yes!!…

- Are profits falling?! →Yes!! … with S&P earnings down nearly -15%

- Are we seeing layoffs?! →Virtually daily, so a resounding YES! (highlighted most recently in November and December)

- Is the Fed tightening into one of the largest slowdowns in history?! →Only at its fastest pace ever!

We penned the aforementioned quote roughly one year ago as Powell touted the strength of the Beveridge curve and every major CEO laughing at the thought of layoffs. Are we that much smarter?!

We would not be so arrogant as to believe so … but after doing this for nearly 27 years and utilizing the data as our north star, powered by Hedgeye; we are married to the data, attempt to be hyperaware of cycles and how they flow, and are not driven by misaligned incentives … we cannot say the same for most others in this industry.

While CEO’s, much like the Lorax’s Once-ler, are focused on biggering and Biggering, and BIGGERING, selling nothing but a trajectory for growth, it’s as if they outright refuse to conceive what happens after the last tree has been chopped! They are blind to the cycle and the small, incremental changes in data or the “particulars” as Hedgeye CEO Keith McCollough often says.

With this in mind, let’s look at the high frequency labor data that is coming in:

- U.S Weekly jobless claims oscillated this month. After registering its 7th consecutive week below 200k, coming in at 190k to start the month … claims then jumped 21k WoW to +211k only to fall below 200k again the week thereafter, registering +192k.

- Continuing Claims increased from 1.655MM earlier in the month to 1.718MM, remaining relatively flat at +1.713MM in the back half of the month, while the JOLTs ( Job Openings data) decelerated to 10.8MM.

- February Non-Farm Payrolls came in slightly better than expected up +2.9% YoY, +311k vs. wall street consensus at +244k.

- We ask you consider this data in conjunction with February’s Challenger, Christmas, and Grey Job cuts data up +77.7k, or a +410% YoY acceleration. The last time job cuts were this steep was February of 2009. Per Daryl Jones, Hedgeye’s Director of Research:

“So far in 2023, 186K job cuts were recorded . . . this is up +427% Y/Y and the highest total for January and February since 2009.”

Again, we understand that unemployment data remains at historically low levels, but as we’ve noted for years, what’s most important is a. understanding the “particulars” and nuances of cycles b. getting the directionality of the data right, and c. being aware of the significance of the rate of change in the data.

Bringing us back to the old Avalanche analogy we used in November:

“The best analogy that comes to mind regarding what we’re currently witnessing in labor markets is the sound one hears when ice and snow begins to crack just before they’re about to get crushed by an avalanche … at first things happen slowly, then once in motion, the speed at which snow, and ice falls increasingly accelerates destroying just about anyone or thing that gets in its way!

There is no stepping in front of an avalanche! The cycle is much like gravity, it just is … and there is little to nothing that anyone can do in an effort to stop it; and at this point the carnage will be ugly.”

If you can’t hear the cracking of the ice beneath the surface of the data, I’m not sure what to tell you?!

Per the data, the same holds true today as it did last month:

“while weakening, the labor data remains robust enough, in the face of a 6.0% CPI, to maintain the Federal Reserve’s higher interest rates for longer mentality.”

BUT, But, but … The economy is strong!

Last month we quoted Hedgeye CEO Keith McCullough:

“2 Weeks Ago: Consensus = “Soft-landing”, 1 rate hike left then 2 cuts … Now: Consensus = No-landing, ~4 rate hikes, 0 Cuts, a potential 50bps hike in March and whispers of a 6% Terminal Rate The more you chase consensus/tourist narratives, the faster they run…”

Given the offsides positioning of the masses at the time, we then added, “In roughly a week, consensus (i.e., the crowd) shifted 180° (for now)”

Aaannnnd, just a few short weeks later, consensus has again, completely reversed course!

So, what happened?!

Panic!

In the last week and a half, we’ve just witnessed the 16th and 29th largest banks in the country (by asset size), become the 2nd and 3rd largest bank closures in U.S. history, behind Washington Mutual’s ($WAMU) closure in 2008. At the time $WAMU was $327 billion in size, where Silicon Valley Bank ($SIVB) had $212 billion in assets, while Signature Bank ($SBNY) had $110 billion; both have now been placed into receivership by regulatory agencies.

At one point in time during Monday, March 13th’s trading session, the Regional Bank index was down -16.5%. As it stands in final edits, the $KRE is down roughly 28.1% over the last two weeks … it’s second largest 2 week decline EVER!

A liquidity event like this should come as no surprise to our readers, as we’ve been screaming it from the rooftops. Did we specifically single out $SIVB or $SBNY, no … it’s very difficult to pinpoint exactly where the next shoe will fall during a Hedgeye #Quad4 disinflationary environment.

At the same time, we have been openly discussing what happens to small and mid-cap financial stocks when a liquidity crisis occurs the previous two weeks leading up to these collapses on #Hedgeye’s #WeeklyNoteBookReview, a Twitter spaces hosted by Robert McGroarty held just about every Wednesday at 4:30pm, which are open to anyone willing to listen.

I explained what happened in 2008, while watching from the institutional desk I sat on at the time; my group focused on small and mid-cap stocks at the time! As we stated on the spaces, “THEY GO BID-LESS!” which is exactly what happened … bids disappeared, financial stocks crated.

More importantly, we’re watching in real-time the dangers of “group think”. Make no mistake, what has happened to $SIVB, $SBNY and countless more financial institutions that you have yet to hear from is a combination of many things: poor management, lack of risk controls, and outright bad assumptions … by the masses.

We would argue, and have for years, that something like this should have been expected consequences from historically poor and constantly latent Federal Reserve policy.

In our 4Q2018 note we attempted to walk investors through this dynamic by using very remedial examples that most anyone could relate to and understand. We felt it imperative to educate readers as to the size of the massive powder keg that was being built off of 8+ years of ZIRP (Zero Percent Interest Rate Policy).

“ZIRP has afforded businesses to raise record amounts of debt (due to their ability to afford it – due to this lower cost of carry) … 8-years of Zero Interest Rate Policy (ZIRP) has allowed just about everyone on the planet to max out their credit cards, continually consolidating their debt to that new card with a zero-interest teaser rate; and with every consecutive rollover, they have borrowed exponentially more and more.”

“The reason time (access to this debt for an abnormally long, prolonged period) is such an important factor is it has given everyone (every government, corporation, consumer, student, car buyer, etc.) with a pulse, the opportunity to lower his or her interest rate. After all, with interest rates this low you can afford “more house”, “more car”, “more expensive education”, “bigger boat”, “more cloths”, “name brands”, “flat screen”, “$1k iPhone”, “larger acquisition”, “larger corporate repurchase plan”, you get the point (I hope).

What has happened over an 8-year ZIRP economy is rather than continuing to pay down principal and retire the debt, over time, as interest rates dropped, the majority of this world has decided to borrow more and more and more – many, exponentially more (in some instances, 3-5-plus times more)”

But no one cared, again, the masses kept on biggering and Biggering AND BIGGERING!

We opined:

“If only a small percentage of “borrowers” were accustomed to low rates, their refinancing of debt at higher levels wouldn’t be such a big deal, the world could handle incremental increases, but when it’s the masses, it’s just like yelling fire in a movie theater.”

Silicon Valley bank will merely be the posterchild for the recklessness that the Fed created by ZIRP and irresponsible monetary/fiscal COVID policies … BUT, they are surely not the only ones with this massive problem!

With copious amounts of free money sloshing through the system, $SIVB watched their deposits skyrocket from $61 billion in 4Q2019 to $189 billion in 4Q2021 … imagine … no one panicked when their deposits nearly tripled in roughly 2 years as their share price grew?! That, after all was building shareholder value! But now, panic ensues … BAILOUT cries billionaire Bill Ackman (I wonder how much money he held at that bank?!) … though, I digress… (SIGH)!!

While $SIVB paid virtually nothing on deposits (roughly 25bps on average), their loans to venture firms moon-shotted … but their biggest problems was their biggering too quickly, increasing their HTM (Held to Maturity) securities portfolio by 10’s of billions from $40 billion to $97 billion through 2021 (as can be tracked in their 10-q’s and 10-k).

Now, there shouldn’t be an investor out there who doesn’t understand the inverse correlation of yield and price when speaking to bonds. When yields go down, the value of a bond goes up … when yields go up, the value of a bond goes down … much like gravity, it just is!

So, in spite of the FOMC being dead wrong about inflation being “transitory” from the start, eventually flipping to persistently high $SIVB (and countless other institutions) pushed a sizable amount of their chips to their HTM portfolios, which by regulation, can’t be hedged … per PwC:

The notion of hedging the interest rate risk in a security classified as held to maturity is inconsistent with the held-to-maturity classification under ASC 320, which requires the reporting entity to hold the security until maturity regardless of changes in market interest rates. For this reason, ASC 815-20-25-43(c)(2) indicates that interest rate risk may not be the hedged risk in a fair value hedge of held-to-maturity debt securities.

But, but, but … they bought high-quality government bonds!

And many will argue that in doing so, it was the “responsible thing” to do … buying government bonds and secure mortgage paper with an average duration of roughly 10 years and an average yield of ~ 1.63%, designating these assets HTM (or held to maturity) … after all, they bought high-quality liquid assets … what could possibly go wrong?!

And that, ladies and gentlemen is “group think”, coupled with no macro strategy, poor assumptions and zero forward vision or curiosity to ask questions, like … should we always assume that interest rates will be this low indefinitely, especially in the face of runaway inflation?!

But no one knew inflation was going to ramp as it did?!

Anyone who implements the Hedgeye process knows that their models were screaming inflation from May/June 2020. We were new to them at the time, and they made it impossible not to know. As we also were advised and understood why disinflation/deflation was headed our way in 2Q2022 … armed with the knowledge that markets often discount economic regime shifts in advance.

It’s not as if $SIVB, $SBNY, $FRC and the rest of the world didn’t have an opportunity to follow a macro process and NowCast that front runs the Federal Reserve and most of Wall Street … they chose the wrong advisors, following those who had been constantly wrong, while dismissing the minority voice who had been right.

From late 2020 through 1H2021 we were emphatic that inflation would be persistently high, by September of 2021 we were telling readers that the Fed would not only continue to tighten, but do so aggressively heading into 2Q/3Q2022

“The FOMC, fresh with their newly appointed hawkish voters and relatively new permanent board member/voter in Christopher Waller, feeling behind the curve as core inflation rises (think housing as we’ve discussed), will most likely begin to RAISE INTEREST RATES as they are tapering, which will be considered a “double tightening” creating an exogenous shock”

Remember, $SVIB began increasing the size of their HTM securities through 2021, and cycles take time!

The opinions we had were not shared by elite academics or Wall Street “experts” advising the masses … they didn’t advise against $SIVB from designating such a large amount of their portfolio to HTM … they just gladly sold them product. As deposits exploded, they didn’t pause asking questions like, “what happens on when the rate of change slows and there is a $1.4 TRILLION-dollar black hole in government spending and subsidies?”

Thanks to Hedgeye’s Josh Steiner, we did!

The key was seeing the massive deceleration in spending, which we noted in September 2021 and literally mapped out December 2021; h/t: to Hedgeye’s Josh Steiner who was educating those willing to listen as early as MID 2021. Those who suggest, no one could see it coming were those who willfully refused to do so, have no forward-looking process, or don’t benefit financially from a deceleration in spending.

There will be those who will have you believe that while SVB’s decision to push such a large pool of assets to HTM wasn’t all that poor of a decision because who could have predicted the Federal Reserve to hike rates in such an unprecedented manner?!

Very few things in this business are “obvious”, at the same time, if a $7-trillion dollar monetary and fiscal bailout can increase balance sheets in an “unprecedented manner”, and loans are being issued in an “unprecedented rate” and inflation was skyrocketing at an “unprecedented pace”, might taking a step back to consider what “unprecedented thing” could happen next, on the other side of it all be the prudent thing to do?! Asking questions like:

- What’s caused this massive spike in deposits?

- What could possibly make the music stop?

- When will is stop?

- How will it affect us?

- What can be done if anything to prepare?!

Economic cycles have both ups and downs … Decades of poor Fed policy have led investors to believe the down cycles immediately vanish with even more central planning, but real consequences exist.

As long-time readers know, we pushed back hard against the CEOs of the largest firms in early 2022, $MSFT, $AAPL, $GOOGL and $META to name a few … freely admitting, we’re not “smarter” per say … but we’re not blinded to the realities of economic CYCLES due to misaligned incentives.

Again, the process is data driven and rate of change focused … a: Deceleration in spending → earnings recession → layoffs → credit event … among other things! Just like the wolves of Yellowstone, there is a natural progression to all of these cycles we’ve been discussing.

It was very transparent from earnings calls and “forward looking guidance” that few companies use a disciplined, forward looking macro-economic process … and the same holds true for the CEOs of these financial firms.

Group think is VERY dangerous, making assumption that the Fed hikes wouldn’t be “unprecedented” or that their hikes wouldn’t adversely affect mortgage rates because they didn’t in 2018 was irresponsible … If you’re seeing “unprecedented” on the up, why wouldn’t you consider “unprecedented” on the down.

Just because consensus believes something to be true, it doesn’t mean that they are always correct … in fact, they are more frequently wrong, which is why we’re frequently on the opposite side of consensus. We don’t do it just to be different; we follow the data, not someone else’s narrative!

Remember, it wasn’t more than a few weeks ago, experts were touting the “war-chest” like balance sheets of financials which now appear to have billions of negative equity … where $SIVB’s mark to market losses as of 3Q2022 was roughly $15.9 billion vs. $11.5 billion of tangible common equity.

The Fed

As soon as the Fed enters the picture, bulls start to knee jerk react with cheers, while we read the details.

The Fed and their newly minted BTFP (Bank Term Funding Program) was recently released to stave off more bank runs, and market bulls believe it’s going to save the world. Unfortunately, it didn’t save the equity or bond holders of $SIVB or $SBNY. It, and a $30 billion-dollar revolving credit line from $JPM and 11 other firms is still having enough trouble preventing $FRC (First Republic) from shuttering its doors; First Republic is/was the 14th largest bank in the country.

The Federal Reserve’s new program has currently back-stopped depositors (both insured and “most” of the uninsured) at both $SIVB and $SBNY, It’s also providing one year term funding, allowing these firms to pledge under-water bonds deemed HTM, as collateral on these loans at “face value”, per the Federal Reserve:

The BTFP offers loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging any collateral eligible for purchase by the Federal Reserve Banks in open market operations (see 12 CFR 201.108(b)), such as U.S. Treasuries, U.S. agency securities, and U.S. agency mortgage-backed securities. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

What this means is if these bonds are trading at $0.60 on the $1.00, the Fed is providing these loans as if the asset is worth $1.00 … making the presumption that since they would eventually be worth par upon maturity, then they can take the duration risk.

This new facility brought with it an explosion of financial firms borrowing from the Federal Reserve’s discount window as its hockey sticked to $152 billion dollars in a single week (up $140.5 billion eclipsing the prior record which occurred during the financial crisis in 2008 at $111 billion). Additionally, we witness the BTFP lend another $11.9 billion dollars to unnamed institutions and $142 billion in Fed loans … as noted by Danielle DiMartino Booth:

“…includes loans that were extended to depository institutions established by the FDIC. The Federal Reserve’s loans to these depository institutions are secured by the collateral and the FDIC provides repayment guarantees.”

The Fed’s balance sheet did expand by roughly $300 billion but it’s important to note … these are LOANS to these institutions to sure up liquidity in an effort to prevent bank runs … LOANS need to be paid back! LOANS are ultimately deflationary.

Quick aside: There is no question that the Fed is clearly making things up as they go … we haven’t even touched on the LEGALITY of this program as recently discussed by John Hussman, Ph.D. @hussmanJP:

It’s not QE. Th Fed has not purchased the securities. It has lent against them. BTFP has problems because it’s inconsistent with both Sections 10 and 13 of the Federal Reserve Act, so the legal authority is unclear, particularly valuing collateral at par, but it’s not QE.

Come on John … Details, details … the Fed loves “crossing many red lines” (though, we digress)

With all of this in mind, take a few steps back for a moment and think: has the directionality of the data the Fed bases their policy off of changed?! Nope!

In fact, per the data the Federal Reserve has tied themselves to, as noted above; be it CPI, Core CPI, CPI core services “less shelter”, or headline labor data as we detailed above; coupled with the Fed’s newly created “solution” for these underwater securities on bank’s balance sheets, there is literally zero excuse for the Fed to pause their rate hike path in an effort to return price stability to the American people.

This is what makes the above thought from Keith McCollough so poignant, as yet again; consensus has flipped based upon headlines, chasing market reaction rather than examining the data the Fed focuses on. As we type, markets have all but removed any further rate hikes from the realm of possibility while moving to a 100 basis points of CUTS over the course of the next year…

“We have both the tools we need and the resolve that it will take to restore price stability on behalf of American families and businesses.” Jay Powell, 5 consecutive FOMC Statements May 2022 – November 2022

RESOLVE

/rəˈzôlv,rəˈzälv/

Noun

- firm determination to do something.

“he received information that strengthened his resolve”

If nothing, Federal Reserve Chairman Jerome Powell has been consistent. From May 2022 through November 2022, the opening quote, led each speech — inflation is too high and price stability is essential in order to have “a sustained period of strong labor market conditions that benefit all.”

While the above referenced sentence has since been removed from his most recent opening statements, the word RESOLVE continues to appear throughout his commentary in regards to the Federal Reserve’s efforts to bring inflation down and restore price stability; from February 1, 2023:

“…we have to deliver that, and so we are strongly resolved that we will … you know, complete this task because we think it has benefits that will support economic activity and benefit the public for many, many years.” Federal Reserve Chairman Jerome Powell Feb 1, 2023

“I laughed at the Lorax, You poor stupid guy! You never can tell what some people will buy.”

But, “Strongly Resolved” … that “sounds” serious!

It was no longer than a few weeks ago in his Semiannual Monetary Policy Report to Congress, Powell, insinuated the same:

“The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.”

We openly admit, we don’t know what the Federal Reserve will do this week, but at the same time, with the $MOVE index near 180 and the Hedgeye Risk Range on Treasury yield wider than they’ve EVER been, neither does anyone else (legally).

The Fed will either remain data dependent, standing resolute in their mandate or they will succumb to the tears and panic of Wall Street beggars.

Should the Fed pivot, they are knowingly opening the door for a massive reacceleration in inflation … a mistake they’ve been extremely vocal about not wanting to make, as emphasized in their February 1, 2023, press conference (as well as the prior 6)

- Although inflation has moderated recently, it remains too high. The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.

- Our overarching focus is using our tools to bring inflation back down to our 2 percent goal and to keep longer-term inflation expectations well anchored. Reducing inflation is likely to require a period of below-trend growth and some softening of labor market conditions. Restoring price stability is essential to set the stage for achieving maximum employment and stable prices over the longer run. The historical record cautions strongly against prematurely loosening policy. We will stay the course, until the job is done.

- I continue to think that it’s very difficult to manage the risk of doing too little and finding out in 6 or 12 months that we actually were close but didn’t get the job done. Inflation springs back, and we have to go back in. And now, you really do worry about expectations getting unanchored and that kind of thing. This is a very difficult risk to manage.

Ah, words, words, words … STARTING WITH THE DATA the Fed is anchored to, the new facilities in place for banks to deter bank runs, the Fed’s understanding of what happens if they take their foot off the gas too early, and overall market positioning and volatility, we believe the more highly probable outcome is the one in which the Fed maintains their battle with inflation and continues to hike rates, which places us on the opposite side of consensus, again.

This being said, last Friday we sold all of our treasury holdings and have drastically reduced positioning to interest rate sensitivity. With bond volatility as high as it is and rates probing the low end of Hedgeye’s risk ranges, there is no reason we have to buy … well, anything?! If the Fed does raise short term rates, we’ll gravitate back towards longer duration bonds that is not controlled by the Fed. We would also anticipate the 2/10s curve to re-widen.

The consumer

If only CPI and Labor were where the decelerating data stopped …… but they are not.

The consumer is a disaster and will continue to deteriorate. While many American’s recently received COLA (Cost of Living Adjustments), which arguably skewed data for the month of January, 32 states have recently cut emergency allotment SNAP or (Supplemental Nutrition Assistance Program) benefits which have been in place since the beginning of the pandemic.

Meaning … 42 MILLION Americans have grown accustomed to and built their lifestyles/spending habits around, on average, nearly $82.00 per MONTH more in their pockets; roughly $328.00 per month lost for a family of 4.

While some readers may balk at the significance, we detailed the condition of the American consumer last month; half of ALL Americans having less than $500 or NO emergency money.

Adding insult to injury, it’s been nearly 3 years since a payment has been made on over $1.7 trillion dollars of government sponsored student loans, which is about to change for roughly 40 million Americans. Per Hedgeye’s Financials team sector head, this equates to roughly $5 billion per month in interest accrual. Again, per Steiner:

The average payment for an undergraduate is $235 per month, student loan with a Graduate degree is on average $600 p/month … so net net, on average, we’re looking at roughly a $400 per month, per household payment that’s set to resume.

Do you really think American’s have been budgeting their lives around these payments resuming?! Of course not, which can be seen in the savings rate data, which is DOWN.

While we acknowledge the current administrations student debt forgiveness program is in the hands of the Supreme Court, regardless of the outcome, payments are set to resume.

Payments will resume within 60 days of either the Department of Education being permitted to implement forgiveness on (SOME) of the debt or a resolution of the litigation faced. Should there be no decision made by June 30th, 2023; payments will resume 60 days thereafter.

More spending that will no longer find its way into consumption … would anyone kindly remind us what percentage consumption was of GDP?! We’ll help, it was 68.5% in December of 2022…

Did we mention weak consumer showing up in the data?!

We just saw a new “post pandemic” low in U.S. Redbook Weekly Retail Sales at +2.6% YoY; with U.S. Retail Sales falling -0.4% MoM in February vs. +3.2% MoM in January, while overall, February Retail Sales were up +5.4% YoY, which was another deceleration vs. January which was up +7.7% YoY.

Odds and ends

- U.S. January Factory Orders declined -1.6% MoM, which was a deceleration from December at +1.7%

- U.S. February ISM Services saw a nominal decline coming in down -0.1 MoM at 55.1 vs. 55.2

- At the same time, Prices Paid continue to fall, by 2.2 points MoM from 67.8 to 65.6; down -3.24% MoM and a -21.06% YoY deceleration.

- Import Prices were down -0.1% MoM, now down -1.1% YoY

As Hedgeye’s Director of Research Daryl Jones noted:

“U.S. imports are now deflationary for the first time since December 2020.”

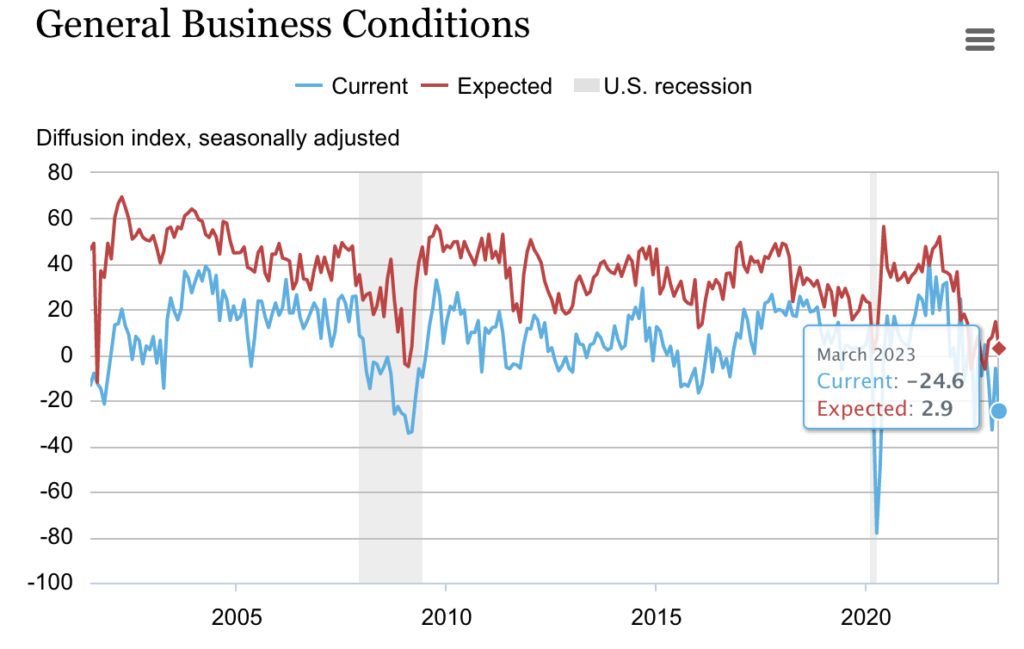

And while everyone was paying attention to the carnage taking place in financials, with markets manic bouncing off every rumored “bail out potential” by the Fed, the March Empire State Manufacturing collapse was lost in the shuffle, falling to -24.6 from -5.8 MoM.

Industrial Production is also rolling, but, no big deal, it’s only the #2 weighting in Hedgeye’s GDP NowCast as we head towards consecutive negative quarters!

Couple this with an already weak consumer and the dynamics discussed above regarding the cancellation of SNAP, resumption of student debt payments, American’s having tapped out their credit cards, a sharp acceleration in delinquencies on both the credit card and auto loan front … while being at the part of the cycle where the employment rate is about to explode and PER THE DATA, things are setting up to get really very dark.

Add in these bank failures … do you believe banks are going to be more or less willing to lend money out?!

Again, it’s the cycle. As people lose their jobs, delinquencies move higher and the largest of banks are being placed into receivership, senior lending officers don’t just open up their purse and throw money at people … they tighten both underwriting and lending standards restricting access to capital … which is THE most important part of the economy. Credit makes the world go round (something we wrote about in June of 2017)

Under a veil of secrecy

If things couldn’t get any worse, there is a very large portion of our financial system that operates under a veil of secrecy. If you think Silvergate $SI, Silicon Valley Bank $SIVB, Signature Bank $SBNY or Credit Suisse $CS is where this ends … we suggest you think again.

$SI, $SIVB, $SBNY, $CS … even the likes of First Republic $FRC whose shares have been collapsing as of late are public companies. For the most part, we have an idea as to what’s on their books. It’s stunning to think that investors are just now waking up to reality, but they are.

For as many bombs that are likely to explode around us, there are countless companies who are hiding being the walls of privacy. How much negative to low yielding debt do pension funds have on their books? What about insurance companies or hedge funds? What story will a private equity firm sell the public until they can no longer hide it?!

We’ve been very vocal about Blackstone’s private BREIT and how they’ve frozen investors out of redemptions, recently noting that their CEO, Stephen Schwarzman was pounding his chest, proud that they have now satisfied roughly 1/3 of the redemption requests in the que ($1.3 billion of the nearly $4.9 billion requested (that we know about))

Given all the recent carnage in the corporate real estate markets, Blackstone just announced that BREIT had recorded its biggest advance in 6 months … while at the very same time … as written by Quill Intelligence CEO, Danielle DiMartino Booth @DiMartinoBooth

“Blackstone Inc. has “substantially” written down the value of a Las Vegas office campus once appraised at ~$500M & allowed mortgage to lapse as CRE prices tumble…$325M CMBS Hughes Center was transferred to a special servicer this month.”

It was also reported late last week that Blackstone is now in talks with Brookfield properties for Blackstone’s stake in One Liberty Plaza office tower; the deal will value the property at $1 billion dollars, down from the $1.5 billion it sold for in 2018. That’s a 33% LOSS from it’s 2018 valuation, do you not think that property was marked up as BREIT announced 15 to 16% annual rises in NAV?! What’s the markdown from it’s most recent mark?! (Shhh … it’s a secret)

And while you can’t compare the size of the two companies, Managing Director of Armada ETF Advisors David Auerbach @DailyREITbeat flagged this one for me, Cottonwood communities NAV just declined by 3% in February.

Which nails my point, so please, think long and hard on this. Just about every publicly traded REIT out there is watching their NAV decline as are many private non-traded REITS … but in the face of all this carnage, including publicly noted significant marks taken to their own portfolio, BREIT somehow has a record an advance … as redemptions that they can’t satisfy continue to build.

It’s impossible … the world can’t be crumbling around them, with companies literally handing the keys back on multi-billion-dollar buildings (as we noted last month), as they publicly take significant marks on prime real estate with the cost of capital exploding, and yet their portfolio saw an increase?! They’re full of sh*t!

The current corporate real estate markets have virtually ZERO liquidity … if they did, BREIT redemption requests would have been satisfied already. As Armada ETFs founder and CEO Phil Bak recently wrote:

“Look: liquidity ain’t an appraisal based NAV, and liquidity ain’t a mark-to-market price against a sparsely traded asset. Liquidity is a bid. An actual cash bid. And public market funds of a modest size have that, every weekday from open to close. Oversized funds of illiquid assets don’t. That right there is how you define liquidity risk.”

Blackstone, Starwood and KKR are hiding behind covenants which allow them to freeze redemptions … and just like $SIVB, $SBNY & $FRC aren’t alone with their balance sheet woes … until private equity, pension funds and other investment firms are forced to take their marks (SEE: Carlyle Group 2008); the charade lives another day … but when they do, don’t be surprised to see a cascading effect of blowups, as all of these markets are interconnected. We’re in the midst of a massive liquidity crisis and the credit crisis has barely begun. When these funds are forced to take their marks, it will more than likely be a day of reckoning for the masses.

“The more things change, the more they stay the same.”

Final thoughts

After 27 years in this business, the above quote resonates with me almost daily. Be it, human behavior, the Fed, talking heads on TV, often times it feels as if we’re living a real-life version of the movie Ground Hogs Day. For those who have never seen it, actor Bill Murray plays the role of a cynical TV weatherman that finds himself reliving the same day over and over again.

- Inflation is transitory … until it’s not … but nobody could see it coming … except those of us who did?!

- The bear market is over … until it’s not … but stocks are up, buy them … until they get crushed again!

- The economy is strong … until banks start blowing up … but nobody could see it coming … damn short sellers … we need an immediate bail out now (cue Bill Ackman crying)!

I recently had lunch with an old friend and client who asked me a question … I’m paraphrasing slightly, but it’s pretty close to exact:

“How do you stay grounded with all the craziness going on around us … banks closing, bankruptcies, layoffs, these are all things you’ve been saying would happen for over a year, how do you stay grounded?!”

My response was simple and quick … “by following the data, utilizing Hedgeye as our guide, and sticking with our process.”

As we’ve noted before, the process and Hedgeye models go both ways, as much as I’d like to be bullish, the data tells a much different, much darker story. We’ll get bullish when the data suggests doing so.

The longer we do this, the more we learn that most people don’t follow a process, they follow their emotions and incentives … from CEOs to Wall Street to Financial Media.

“And at that very moment, we heard a loud whack! From outside in the fields came a sickening smack of an axe on a tree. Then we heard the tree fall. The very last Truffula Tree of them all! No more trees. No more Thneed’s. No more work to be done.” The Lorax

Virtually no one asks what happens when the music stops, because a CEO gets paid to grow and wall street gets paid to sell and financial media gets paid more in advertising revenues when the money is flowing. It’s the very reason why earnings estimates remain robust in the face of them clearly rolling over and GDP decelerating.

“As we’ve stated for nearly a year, GDP will first crater from 7 to 2, then to zero and eventually it will trough in outright negative territory. This, as we head deeper into a U.S. corporate profit recession. This will force even more U.S. based businesses to expand their cost cutting efforts (layoffs) even more than they originally believed they’d have to, creating a self-feeding downward spiral.

However, even with GDP and inflation falling, and layoffs rising … there will still be no data points directly tied to the Fed’s mandates that will be anywhere near a level which would trigger any meaningful bailout large enough to thwart off this U.S. corporate earnings recession.”

$META laid off another 10,000 employees last week, $AMZN announced another 9,000 cuts earlier this week.

Again, in APRIL 2022 we said:

“They (the FOMC) are backwards looking – they don’t understand labor is as late cycle as it gets… As margins compress – profits fall – layoffs are around the corner – these (expletive deleted) will be tightening into one of the largest slowdowns in history.”

By 2Q22, the deceleration in growth via GDP, earnings, etc. should be very noticeable. The second quarter is also when we should begin to see a real deceleration in inflationary pressures as well. As previously discussed, a Rate of Change deceleration in both Growth and Inflation would place us squarely into a #Deflationary economic investing regime; the same environment that brought us the 4Q2018 decline and 1Q2020 crash (among other larger deflationary market crashes).

Why are there so few people asking these questions BEFORE things blow up?! We’re a one man shop in Raleigh, NC …

Where were the CEO’s … where was Wall Street or the financial media?! I’ll tell you where … they were doing the same thing then as they’re doing today, only then they were pushing you to buy the falling knife in profitless tech companies, while today, as I write, they’re doing the same in financials.

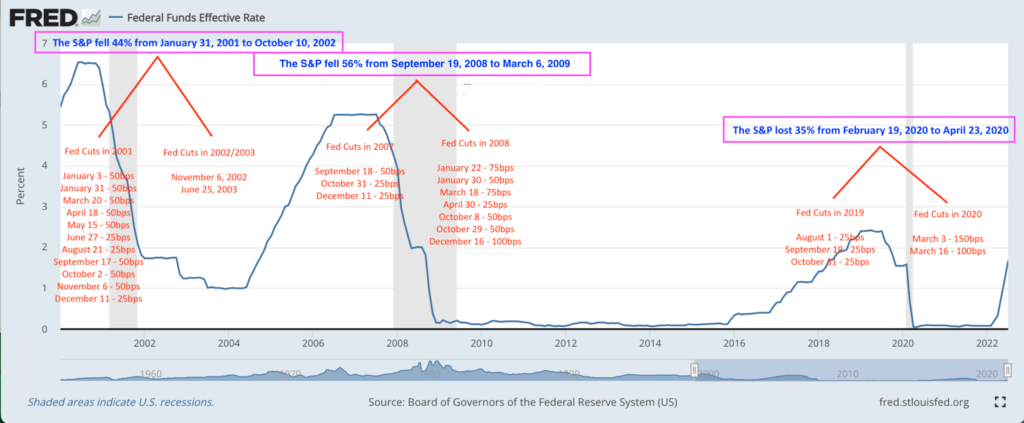

These blow ups have just begun. As the Fed panics to handle liquidity issues, the come the credit blow-ups, then the layoffs … THEN the rate cuts, but once we’re there, we’re already buried by the crashing avalanche … as we noted in August of 2022, the largest market declines take place as the Fed is cutting rates.

As I sat pondering how to close this note, Keith McCullough used one of the best analogies I’ve ever heard to describe the part of the cycle that we’re in right now. So, while paraphrasing, ALL credit on this thought goes to him.

Picture you’re on the Titanic, which has just hit the iceberg. The ship is taking on massive amounts of water. Do you hang out and watch? Sit down and play another hand of cards? Go back to your room to pack?! Do you head to the back of the ship to hide as it’ll be the last to breech the water?!

Or do you frantically search for the first available life raft?!

In 2008, when Bear Sterns collapsed, other financial firms attempted to collectively “save them”, too … a week later Bear was gone. Warren Buffet bought banks in October of 2008; markets subsequently collapsed another 35/40% before troughing.

You don’t run to hide out in large cap tech stocks because the world is collapsing around you … you seek safety and protection … you find the life raft!

At the end of the day, every investor needs to care more about their financial future than anyone else. Investors need to be advocates; they need to call BS on those who continue to be wrong as they sell you a story.

We’d argue that you take a chance, align yourselves with someone who has been much more accurate in the face of being vilified by a majority that’s been flat out wrong.

While none of us are perfect, there are advisors out there who refuse to accept the traditional Wall Street narrative; those of us who put the work in and ask difficult questions in the face of those who operate under the guise of a moral and intellectual superiority as they peddle narratives over facts and data.

Seek out those who understand the peaks and troughs of cycles, while dedicating themselves to the data and does their best to see the rate of change slowdown before the last tree falls. They won’t always be right … they’ll make mistakes (we sure do). But over the course of TIME, we should protect, preserve, and grow your hard-earned wealth better than most.

The Lorax said nothing. Just gave me a glance… just gave me a very sad, sad backward glance … And I’ll never forget the grim look on his face when he hoisted himself and took leave of this place … And all that the Lorax left here in this mess was a small pile of rocks, with one word… UNLESS …

But now, says the Once-ler, now that you’re here, the word of the Lorax seems perfectly clear. UNLESS someone like you cares a whole awful lot, nothing is going to get better. It’s not” ~ The Lorax By Dr. Seuss

Changing your mindset and approach to how you invest is not easy … though, if life teaches us one thing, it’s that nothing stays the same forever; change is inevitable … you date different people, eat different meals, friends and relatives pass on, you have children … CHANGE is one of the very few constants; so embrace it!

Unless you take a chance on doing something different, nothing is going to change. Deflationary investing regimes are very destructive. The question is, can you spot them. Most of wall street can’t, it’s evident … they tell you no one can (because they can’t and don’t want to lose your business).

Hedgeye has … as have many of their disciples (with varying degrees of success based upon investment restrictions). At the same time … UNLESS you take that first step, unless you take a chance, in the words of the Once-ler, “nothing is going to get better, it’s not!”

Good Investing,

Mitchel C. Krause

Managing Principal & CCO

4141 Banks Stone Dr.

Raleigh, NC. 27603

phone: 919-249-9650

toll free: 844-300-7344

mitchel.krause@othersideam.com

Please click here for all disclosures.